Chiến lược bắt biên độ động thái RSI - Dải Bollinger

Tổng quan

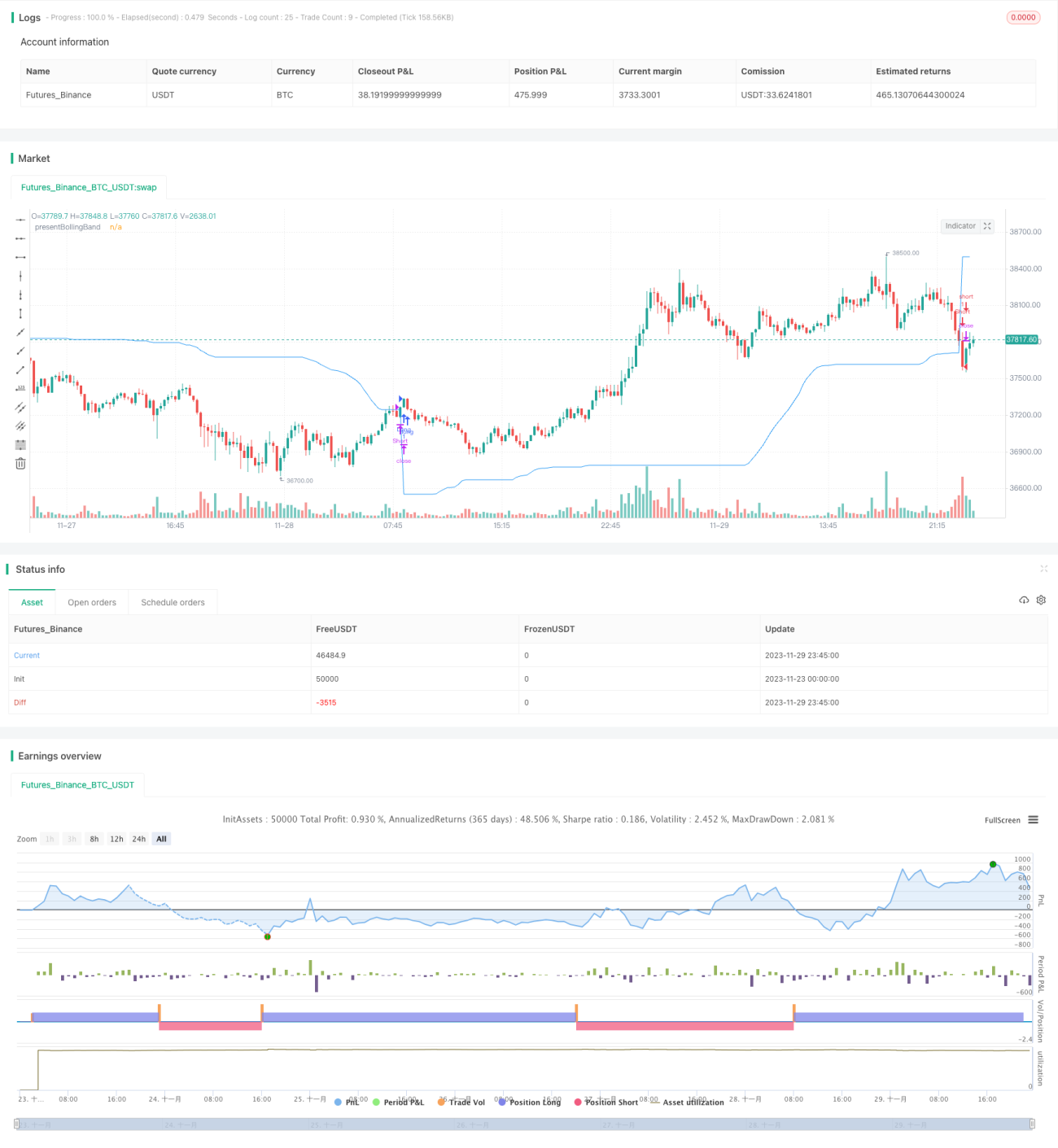

Chiến lược RSI-Bollinger Bands bắt sóng biên độ động là một chiến lược giao dịch tích hợp các khái niệm về Bollinger Bands (BB), Chỉ số Sức mạnh Tương đối (RSI) và Đường trung bình động đơn giản (SMA). Điểm độc đáo của chiến lược này nằm ở việc nó tính toán một mức động dựa trên giá đóng cửa giữa dải trên và dải dưới. Tính năng đặc biệt này cho phép chiến lược thích ứng với biến động thị trường và biến động giá.

Thị trường tiền điện tử và chứng khoán có biến động cao, do đó rất phù hợp để áp dụng chiến lược Bollinger Bands. RSI giúp xác định các tình trạng quá mua/quá bán trên thị trường vốn thường mang tính đầu cơ này.

Nguyên lý chiến lược

Bollinger Bands động: Chiến lược trước tiên tính toán dải trên và dải dưới của Bollinger Bands dựa trên độ dài và hệ số nhân do người dùng xác định. Sau đó, kết hợp giữa Bollinger Bands và giá đóng cửa để điều chỉnh động giá trị presentBollingBand. Cuối cùng, khi giá vượt qua present BollingBand, tín hiệu long được tạo ra; khi giá vượt qua present BollingBand, tín hiệu short được tạo ra.

RSI: Nếu người dùng chọn sử dụng RSI để tạo tín hiệu, chiến lược còn tính toán RSI và SMA của nó, đồng thời sử dụng chúng để tạo ra các tín hiệu long và short bổ sung. Chỉ khi tùy chọn "Sử dụng RSI tạo tín hiệu" được đặt thành true thì các tín hiệu dựa trên RSI mới được sử dụng.

Sau đó, chiến lược kiểm tra hướng giao dịch đã chọn và vào lệnh long hoặc short tương ứng. Nếu hướng giao dịch được đặt thành "Hai chiều", chiến lược có thể đồng thời vào lệnh long và short.

Cuối cùng, khi giá đóng cửa vượt qua present BollingBand, vị thế long được đóng lại; khi giá đóng cửa vượt qua present BollingBand, vị thế short được đóng lại.

Phân tích ưu điểm

Chiến lược kết hợp ưu điểm của các chỉ báo Bollinger Bands, RSI và SMA, có khả năng thích ứng với biến động của thị trường, bắt sóng biên độ một cách linh hoạt và tạo ra tín hiệu giao dịch trong các tình huống quá mua/quá bán.

Chỉ báo RSI bổ sung tín hiệu giao dịch từ Bollinger Bands, tránh vào lệnh sai trong thị trường dao động. Cho phép lựa chọn chỉ long, chỉ short hoặc giao dịch hai chiều, thích ứng với các điều kiện thị trường khác nhau.

Các tham số có thể tùy chỉnh, cho phép điều chỉnh theo mức độ chấp nhận rủi ro cá nhân.

Phân tích rủi ro

Chiến lược phụ thuộc vào các chỉ báo kỹ thuật, không thể đối phó với các biến động lớn do yếu tố cơ bản gây ra.

Việc thiết lập tham số Bollinger Bands không phù hợp có thể dẫn đến tín hiệu giao dịch quá thường xuyên hoặc quá thưa thớt.

Rủi ro khi giao dịch hai chiều tăng cao, cần cảnh giác với khoản lỗ từ vị thế short ngược chiều.

Khuyến nghị kết hợp cắt lỗ để kiểm soát rủi ro.

Hướng tối ưu hóa

-

Kết hợp các chỉ báo khác để lọc tín hiệu, ví dụ MACD.

-

Thêm chiến lược cắt lỗ.

-

Tối ưu hóa tham số của Bollinger Bands và RSI.

-

Điều chỉnh tham số theo từng sản phẩm giao dịch và khung thời gian khác nhau.

-

Xem xét tối ưu hóa trên thực tế, điều chỉnh tham số để phù hợp với tình hình thực tế.

Tổng kết

Chiến lược RSI-Bollinger Bands bắt sóng biên độ động là một chiến lược dựa trên các chỉ báo kỹ thuật, kết hợp ưu điểm của Bollinger Bands, RSI và SMA. Thông qua việc điều chỉnh động Bollinger Bands để bắt sóng thị trường. Chiến lược có khả năng tùy chỉnh và tối ưu hóa rộng rãi, nhưng không thể dự đoán các thay đổi cơ bản. Khuyến nghị kiểm chứng hiệu quả trên thực tế, nếu cần thì điều chỉnh tham số hoặc bổ sung các chỉ báo khác kết hợp sử dụng để giảm rủi ro.

- 1