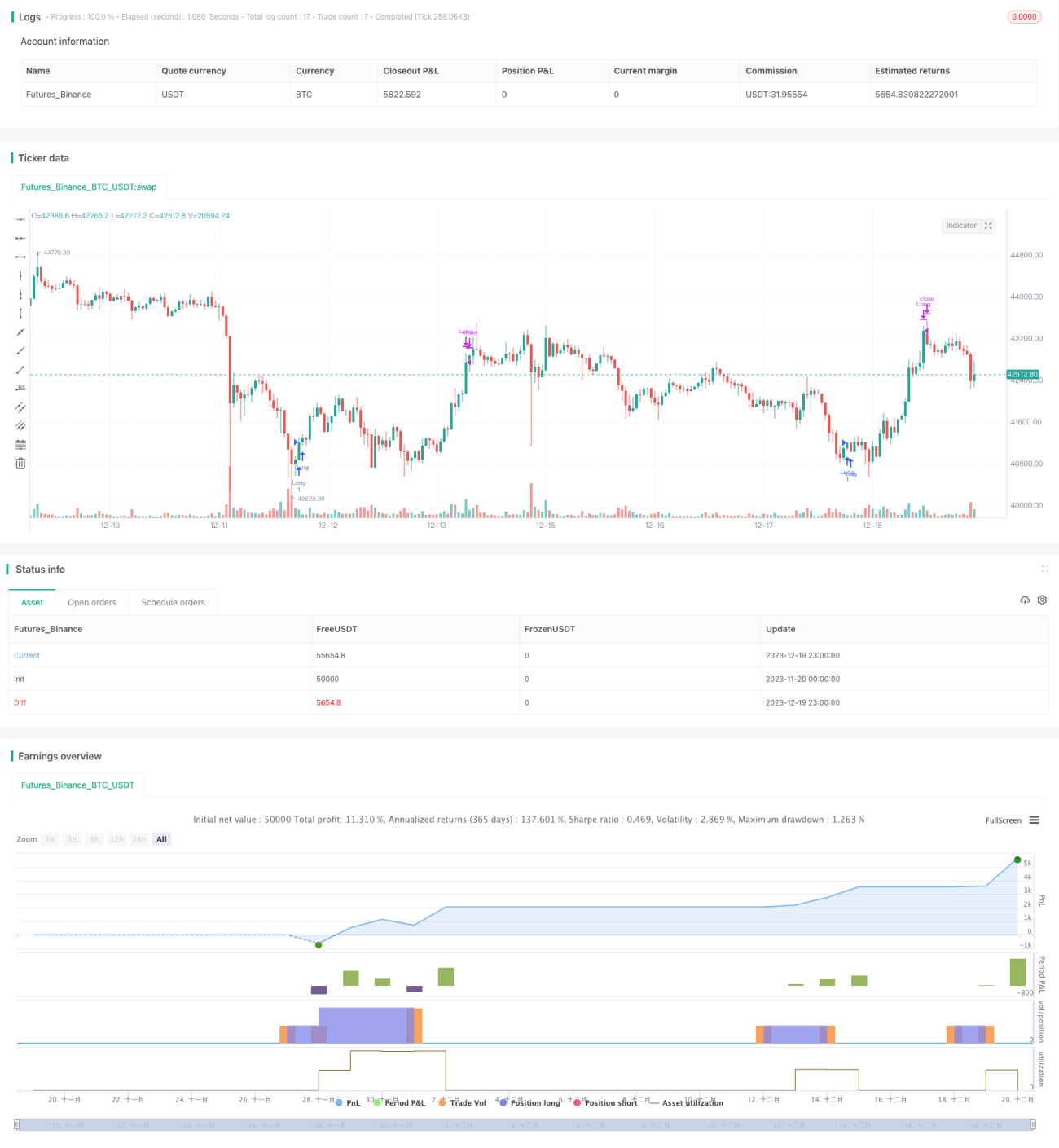

Chiến lược giao dịch đa khung thời gian dựa trên chỉ báo biến động và chỉ báo stochastic

Tổng quan

Chiến lược này kết hợp chỉ số biến động VIX và chỉ số ngẫu nhiên RSI, thông qua sự kết hợp của các chỉ báo với khung thời gian khác nhau, nhằm thực hiện hiệu quả các lệnh mua phá vỡ và đóng vị thế cắt lỗ khi quá mua/quá bán. Chiến lược có không gian tối ưu hóa lớn, có thể thích ứng với các điều kiện thị trường khác nhau.

Nguyên lý chiến lược

-

Tính chỉ số biến động VIX: lấy giá cao nhất và giá thấp nhất trong 20 ngày gần nhất để tính biến động. Khi biến động cao hơn dải trên, thị trường đang hoảng loạn; khi thấp hơn dải dưới, thị trường đang tự mãn.

-

Tính chỉ số RSI: lấy mức tăng giảm trong 14 ngày gần nhất, khi RSI trên 70 là vùng quá mua, dưới 30 là vùng quá bán.

-

Kết hợp hai chỉ báo: mua khi biến động cao hơn dải trên hoặc phân vị cao nhất; đóng vị thế khi RSI trên 70.

Ưu điểm chiến lược

- Kết hợp nhiều chỉ báo, đánh giá tổng hợp thời điểm thị trường.

- Các chỉ báo với khung thời gian khác nhau kiểm chứng lẫn nhau, nâng cao độ chính xác của quyết định.

- Có thể tối ưu và điều chỉnh thông số để thích ứng với các công cụ giao dịch khác nhau.

Phân tích rủi ro

- Thiết lập thông số không phù hợp có thể dẫn đến nhiều tín hiệu giả.

- Chỉ dùng một chỉ báo đóng vị thế dễ bỏ lỡ sự đảo chiều giá.

Đề xuất tối ưu hóa

- Bổ sung thêm các chỉ báo xác nhận như đường trung bình, dải Bollinger để xác định thời điểm vào lệnh.

- Bổ sung thêm các chỉ báo đóng vị thế như mô hình nến đảo chiều.

Tổng kết

Chiến lược này sử dụng chỉ số VIX để đánh giá thời điểm và mức độ rủi ro của thị trường, kết hợp với chỉ số RSI để lọc bỏ các điểm giao dịch bất lợi do quá mua/quá bán, từ đó mua vào tại thời điểm hiệu quả và cắt lỗ kịp thời. Chiến lược có không gian tối ưu hóa lớn, có thể thích ứng với môi trường thị trường rộng hơn.

- 1