Chiến lược theo dõi xu hướng đảo chiều dựa trên giao nhau của chỉ báo động lượng

Tổng quan

Chiến lược này kết hợp nhiều chỉ báo động lượng như MACD, RSI, ADX để nhận diện tín hiệu đảo chiều giá, áp dụng chiến lược ngược xu hướng, vào lệnh khi xu hướng mạnh đảo ngược. Chiến lược đồng thời đặt cắt lỗ và chốt lời để khóa lợi nhuận và kiểm soát rủi ro.

Nguyên lý chiến lược

Chiến lược này trước hết kết hợp so sánh sự giao nhau của đường MACD nhanh và chậm để xác định xu hướng giá; sau đó kết hợp chỉ báo RSI để lọc tín hiệu phá vỡ giả, chỉ khi sự đảo chiều giá thực sự xảy ra mới phát sinh tín hiệu giao dịch; cuối cùng sử dụng chỉ báo ADX để xác nhận lại xem giá đã bước vào trạng thái xu hướng hay chưa. Chỉ khi tất cả các điều kiện trên đồng thời thỏa mãn, tín hiệu mua hoặc bán mới được phát ra.

Cụ thể, khi đường MACD nhanh cắt lên trên đường chậm, RSI trên 50 và hồi phục, ADX trên 20 thì là tín hiệu mua; khi đường MACD nhanh cắt xuống dưới đường chậm, RSI dưới 50 và giảm xuống, ADX trên 20 thì là tín hiệu bán.

Phân tích ưu điểm

Ưu điểm lớn nhất của chiến lược này là sử dụng sự kết hợp của nhiều chỉ báo, có thể lọc hiệu quả thị trường đi ngang và tín hiệu sai, thực sự xác định được điểm đảo chiều xu hướng, từ đó đạt tỷ lệ thắng cao. Ngoài ra, việc đặt cắt lỗ và chốt lời giúp khóa lợi nhuận và kiểm soát rủi ro, có thể chống lại hiệu quả tác động của các sự kiện bất ngờ.

Phân tích rủi ro

Rủi ro lớn nhất của chiến lược này nằm ở việc xác định sai sự đảo chiều xu hướng, chẳng hạn như giá điều chỉnh sâu gây nhầm lẫn. Ngoài ra, xu hướng mới sau khi đảo chiều có thể không đủ bền vững để thu được lợi nhuận đủ lớn.

Giải pháp là tối ưu thêm tham số, điều chỉnh mức cắt lỗ, hoặc kết hợp thêm nhiều chỉ báo phụ trợ để lọc tín hiệu.

Hướng tối ưu hóa

Chiến lược này có thể được tối ưu hóa thêm theo các hướng sau:

- Tối ưu tổ hợp tham số MACD, RSI, nâng cao độ chính xác khi xác định đảo chiều giá.

- Thêm nhiều chỉ báo lọc hơn như KD, BOLL, tạo hiệu ứng vòng quanh chỉ báo.

- Điều chỉnh linh hoạt mức cắt lỗ, điều chỉnh theo các tình huống thị trường khác nhau.

- Dựa trên diễn biến thực tế sau khi đảo chiều, sửa đổi vị trí chốt lời theo thời gian thực.

Tổng kết

Chiến lược này tổng hợp sử dụng nhiều chỉ báo động lượng để nhận diện các cơ hội đảo chiều giá tiềm năng. Thông qua tối ưu hóa tham số, kết hợp thêm các chỉ báo phụ trợ, điều chỉnh linh hoạt chiến lược cắt lỗ và chốt lời, có thể nâng cao hơn nữa tính ổn định và độ tin cậy của chiến lược, khóa các cơ hội giao dịch đa dạng mà thị trường cung cấp.

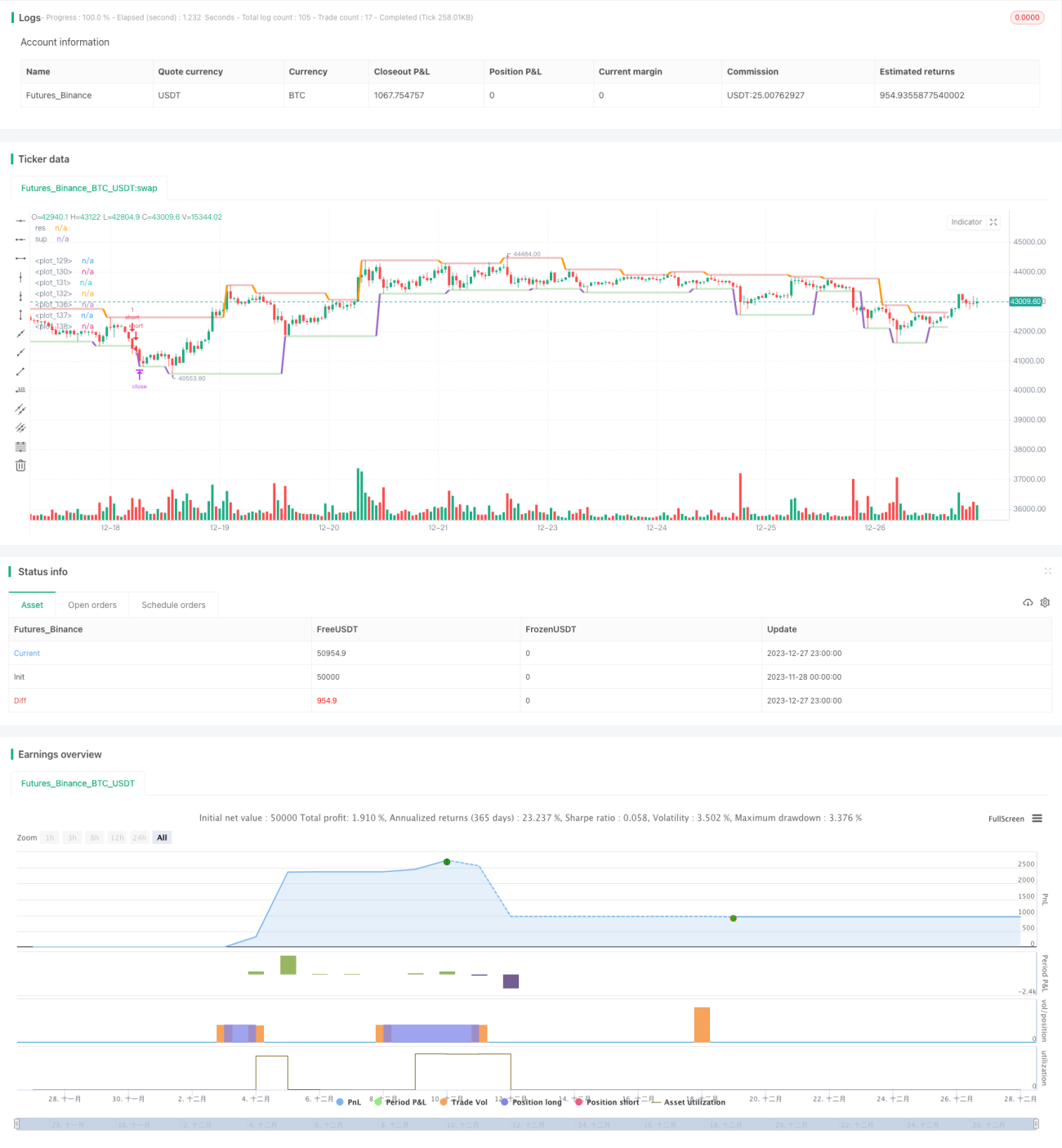

/*backtest

start: 2023-11-28 00:00:00

end: 2023-12-28 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © AHMEDABDELAZIZZIZO

//@version=5- 1