Chiến lược theo dõi xu hướng cân bằng sử dụng Đường trung bình động Hull

Tổng quan

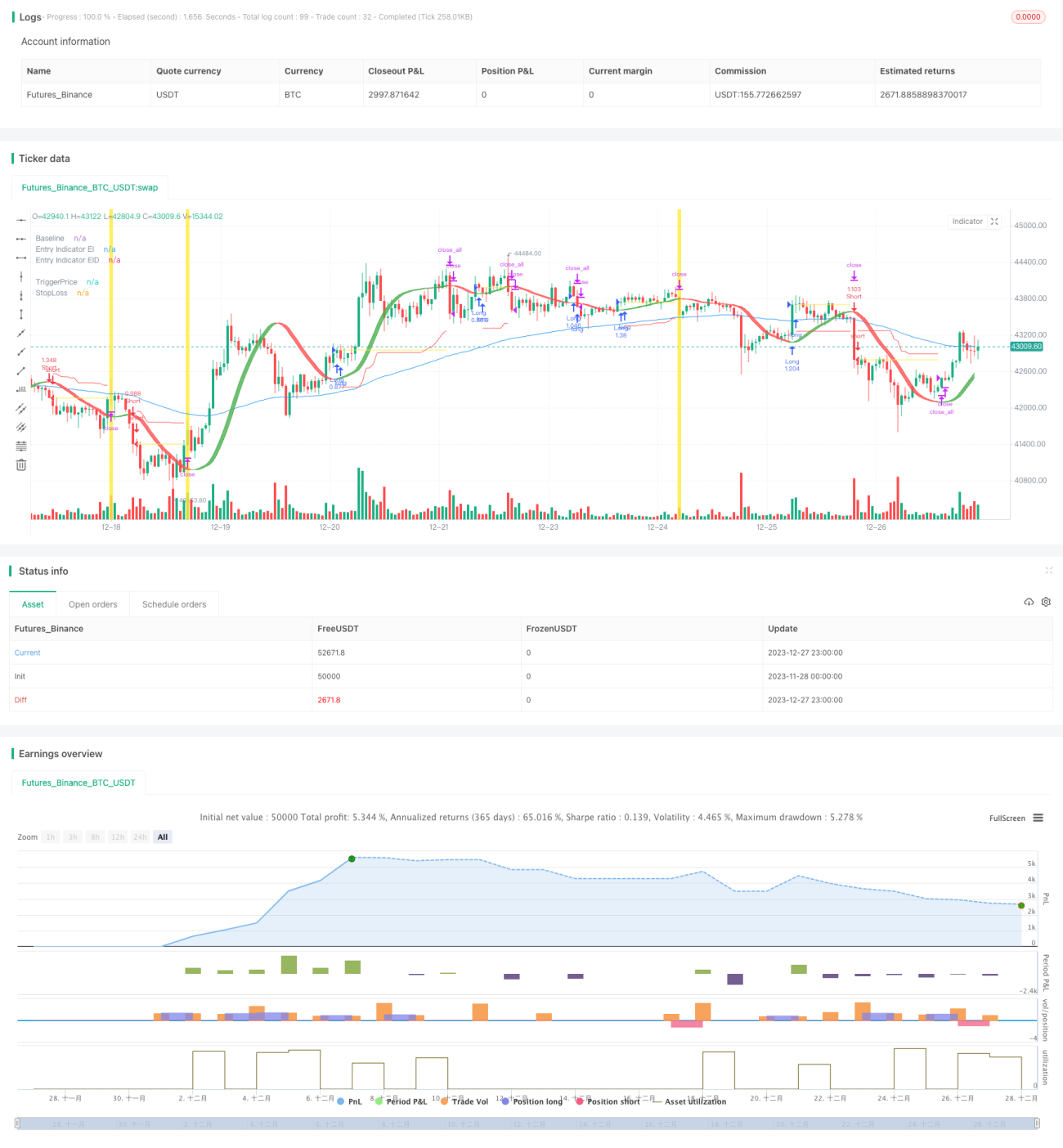

Chiến lược theo dõi cân bằng sử dụng đường trung bình động Hull làm chỉ báo tham gia thị trường chính để xác định hướng xu hướng giá. Đồng thời, chiến lược này kết hợp với nhiều chỉ báo khác như đường cơ sở, chỉ báo xác nhận, v.v., để xác thực xu hướng giá và lọc các tín hiệu giả. Sau khi tham gia thị trường, chiến lược sử dụng Average True Range để tính toán mức dừng lỗ động, nhằm theo dõi xu hướng và thu lợi nhuận.

Nguyên lý chiến lược

Cốt lõi của chiến lược theo dõi cân bằng là đường trung bình động Hull. Đường trung bình động Hull nhạy cảm hơn với sự thay đổi giá, có thể xác định hướng xu hướng một cách hiệu quả. Khi giá phá vỡ lên trên đường Hull, xác nhận xu hướng tăng hình thành, vào lệnh mua; khi giá phá vỡ xuống dưới đường Hull, xác nhận xu hướng giảm hình thành, vào lệnh bán.

Ngoài ra, chiến lược còn đưa vào chỉ báo đường cơ sở để xác định xu hướng dài/ngắn hạn; chỉ báo xác nhận để lọc các phá vỡ giả. Chỉ khi cả đường cơ sở và chỉ báo xác nhận đều xác nhận hướng xu hướng, tín hiệu giao dịch mới được kích hoạt.

Sau khi tham gia thị trường, chiến lược sử dụng ATR và Hull EMA để tính toán mức dừng lỗ dựa trên biên độ dao động thực trung bình. Khi xu hướng tiếp diễn, đường dừng lỗ cũng liên tục dịch chuyển lên/xuống để khóa lợi nhuận từ xu hướng.

Phân tích ưu điểm

Chiến lược theo dõi cân bằng kết hợp ưu điểm của việc xác định xu hướng và quản lý rủi ro, có thể đạt được lợi nhuận tốt trong thị trường xu hướng. So với chiến lược dừng lỗ cố định, nó có thể theo dõi xu hướng bằng dừng lỗ di động, tránh bị dừng lỗ do biến động thị trường bình thường.

Sự kết hợp của nhiều chỉ báo cũng giúp chiến lược nhạy cảm hơn với thay đổi thị trường, đồng thời có thể lọc hiệu quả các tín hiệu giả. Ngoài ra, chiến lược cũng cung cấp nhiều tham số để điều chỉnh, người dùng có thể tối ưu hóa dựa trên đánh giá thị trường của mình.

Phân tích rủi ro

Chiến lược này chủ yếu phụ thuộc vào các chỉ báo xu hướng, dễ phát sinh tín hiệu sai và dừng lỗ trong thị trường đi ngang. Ngoài ra, sự kết hợp nhiều chỉ báo cũng có thể dẫn đến xung đột tín hiệu. Việc thiết lập tham số không phù hợp cũng có thể khiến chiến lược hoạt động kém.

Có thể xem xét thêm module đánh giá bổ sung vào chiến lược, tạm dừng giao dịch khi các chỉ báo phân kỳ; hoặc áp dụng cơ chế biểu quyết, tổng hợp kết quả từ nhiều chỉ báo. Về thiết lập tham số, có thể tìm tham số tối ưu thông qua phương pháp tối ưu hóa backtest.

Hướng tối ưu hóa

Chiến lược theo dõi cân bằng có thể được tối ưu hóa theo các hướng sau:

- Thêm module đánh giá, ví dụ module biến động, tạm dừng giao dịch khi biến động cao;

- Thêm module học máy, sử dụng thuật toán học máy để xác định trọng số chỉ báo;

- Tối ưu hóa tham số chỉ báo, tìm tổ hợp tham số tốt nhất;

- Tối ưu hóa thuật toán dừng lỗ di động, giúp dừng lỗ theo dõi xu hướng tốt hơn;

- Thêm module quản lý rủi ro, như vi phạm dừng lỗ, điều chỉnh vị thế động, v.v.

Kết luận

Chiến lược theo dõi cân bằng nhìn chung là một chiến lược theo dõi xu hướng xuất sắc. Nó kết hợp thành công việc xác định xu hướng và dừng lỗ động, có thể theo dõi xu hướng hiệu quả để thu lợi nhuận. Thông qua tối ưu hóa thêm, có thể đạt được hiệu suất chiến lược tốt hơn. Chiến lược này cung cấp một tham khảo tốt cho việc xây dựng các chiến lược giao dịch định lượng.

/*backtest

start: 2023-11-28 00:00:00

end: 2023-12-28 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// © Milleman

//@version=4

strategy("MilleMachine", overlay=true, default_qty_type = strategy.percent_of_equity, default_qty_value = 100, initial_capital=10000, commission_type=strategy.commission.percent, commission_value=0.06)

- 1