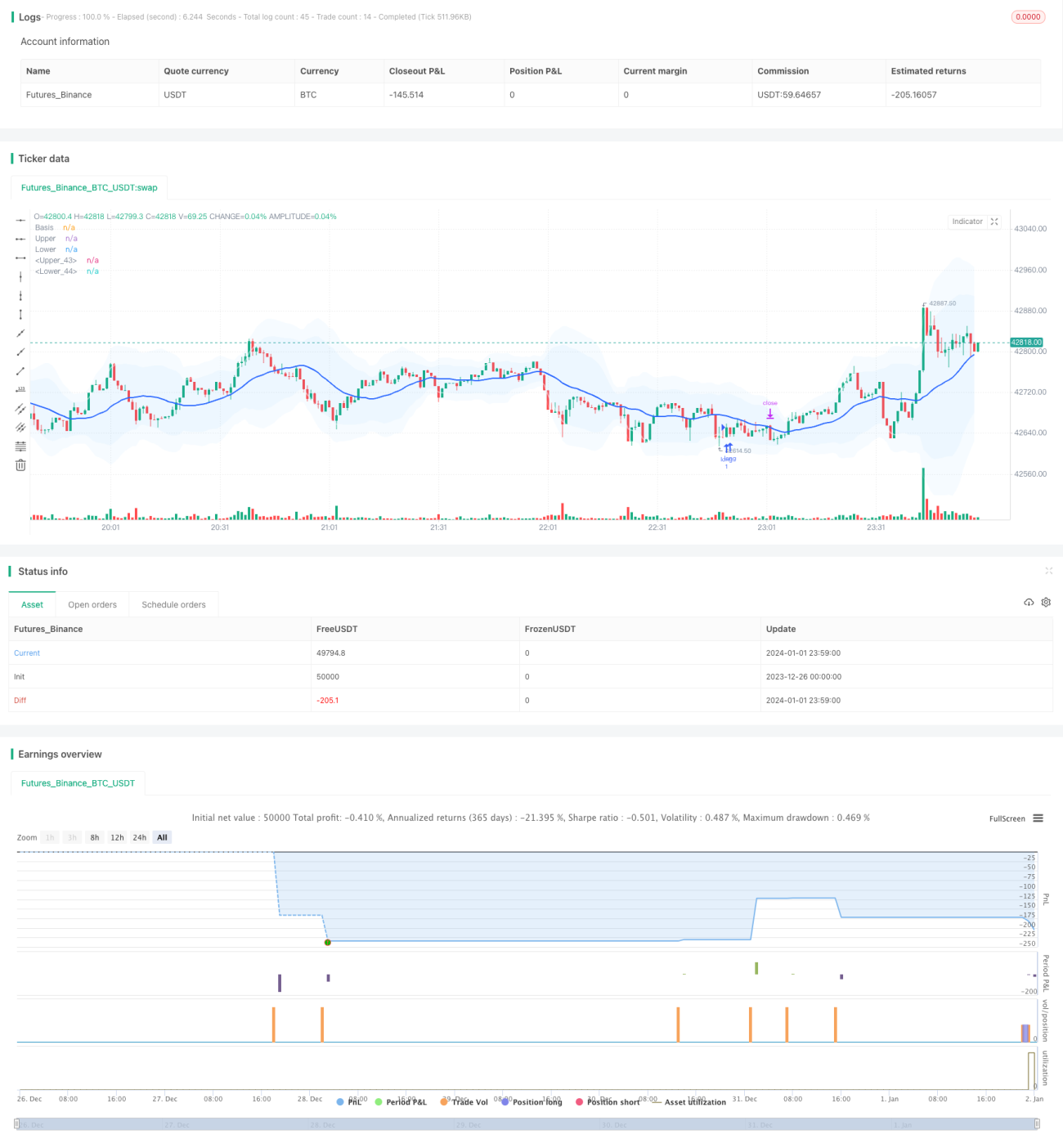

Chiến lược trailing stop ATR kết hợp dải Bollinger

Tổng quan

Chiến lược này kết hợp sử dụng chỉ báo Bollinger Bands và chỉ báo ATR (Average True Range) để tạo thành chiến lược giao dịch đột phá có trailing stop. Khi giá vượt qua dải trên hoặc dải dưới của Bollinger Bands với độ lệch chuẩn được chỉ định, tín hiệu giao dịch được phát ra. Đồng thời, sử dụng chỉ báo ATR để tính toán mức stop loss và take profit, kiểm soát tỷ lệ lời/lỗ. Ngoài ra, chiến lược còn có các chức năng như bộ lọc thời gian và tối ưu hóa tham số.

Nguyên lý chiến lược

Bước đầu tiên, tính toán đường trung bình, dải trên và dải dưới. Đường trung bình là đường trung bình động đơn giản SMA của giá, dải trên và dưới là bội số nguyên của độ lệch chuẩn giá. Khi giá phá vỡ từ dải dưới đi lên, vào lệnh mua; khi giá phá vỡ từ dải trên đi xuống, vào lệnh bán.

Bước thứ hai, tính toán chỉ báo ATR. Chỉ báo ATR phản ánh mức độ biến động giá trung bình. Thiết lập mức stop loss cho lệnh mua và lệnh bán dựa trên giá trị ATR. Đồng thời, thiết lập vị trí chốt lời dựa trên giá trị ATR để kiểm soát tỷ lệ lời/lỗ.

Bước thứ ba, sử dụng bộ lọc thời gian, chỉ giao dịch trong khung thời gian chỉ định, tránh biến động mạnh do các sự kiện tin tức lớn.

Bước thứ tư, cơ chế trailing stop. Dựa vào vị trí ATR mới nhất, điều chỉnh mức stop loss theo thời gian thực, khóa thêm lợi nhuận.

Phân tích ưu điểm

-

Chỉ báo Bollinger Bands phản ánh tâm giá, hiệu quả hơn so với đường trung bình động đơn thuần;

-

Stop loss dựa trên ATR giúp kiểm soát tỷ lệ lời/lỗ mỗi lệnh, quản lý rủi ro hiệu quả;

-

Trailing stop có thể tự động điều chỉnh theo biến động thị trường, khóa thêm lợi nhuận;

-

Chiến lược có nhiều tham số, có thể tùy chỉnh kết hợp cá nhân hóa.

Phân tích rủi ro

-

Khi thị trường dao động điều chỉnh, dễ xảy ra nhiều lỗ nhỏ;

-

Đột phá Bollinger Bands làm đảo chiều có thể thất bại;

-

Giao dịch vào ban đêm và trong thời gian tin tức lớn có rủi ro cao, cần tránh.

Biện pháp đối phó:

- Tuân thủ nghiêm ngặt nguyên tắc quản lý rủi ro, kiểm soát lỗ đơn lệnh;

- Tối ưu hóa tham số, tăng tỷ lệ thắng;

- Sử dụng bộ lọc thời gian để né tránh các khung giờ rủi ro cao.

Hướng tối ưu hóa

- Kiểm tra các tổ hợp tham số khác nhau để tối ưu cấu hình

- Thêm chỉ báo động lượng như OBV để chọn thời điểm

- Thêm mô-đun học máy để tối ưu hóa

Tổng kết

Chiến lược này kết hợp sử dụng Bollinger Bands để đánh giá xu hướng trung tâm và hướng đột phá, chỉ báo ATR để tính toán chốt lời và cắt lỗ nhằm đảm bảo tỷ lệ lời/lỗ, cùng với trailing stop để khóa lợi nhuận. Ưu điểm của chiến lược là khả năng tùy chỉnh cao, rủi ro được kiểm soát, phù hợp cho giao dịch trong ngày (Intraday Trading). Tối ưu hóa tham số và học máy có thể nâng cao tỷ lệ thắng và khả năng sinh lời của chiến lược.

- 1