Chiến lược đột phá vị thế mua dựa trên nến K

Tổng quan

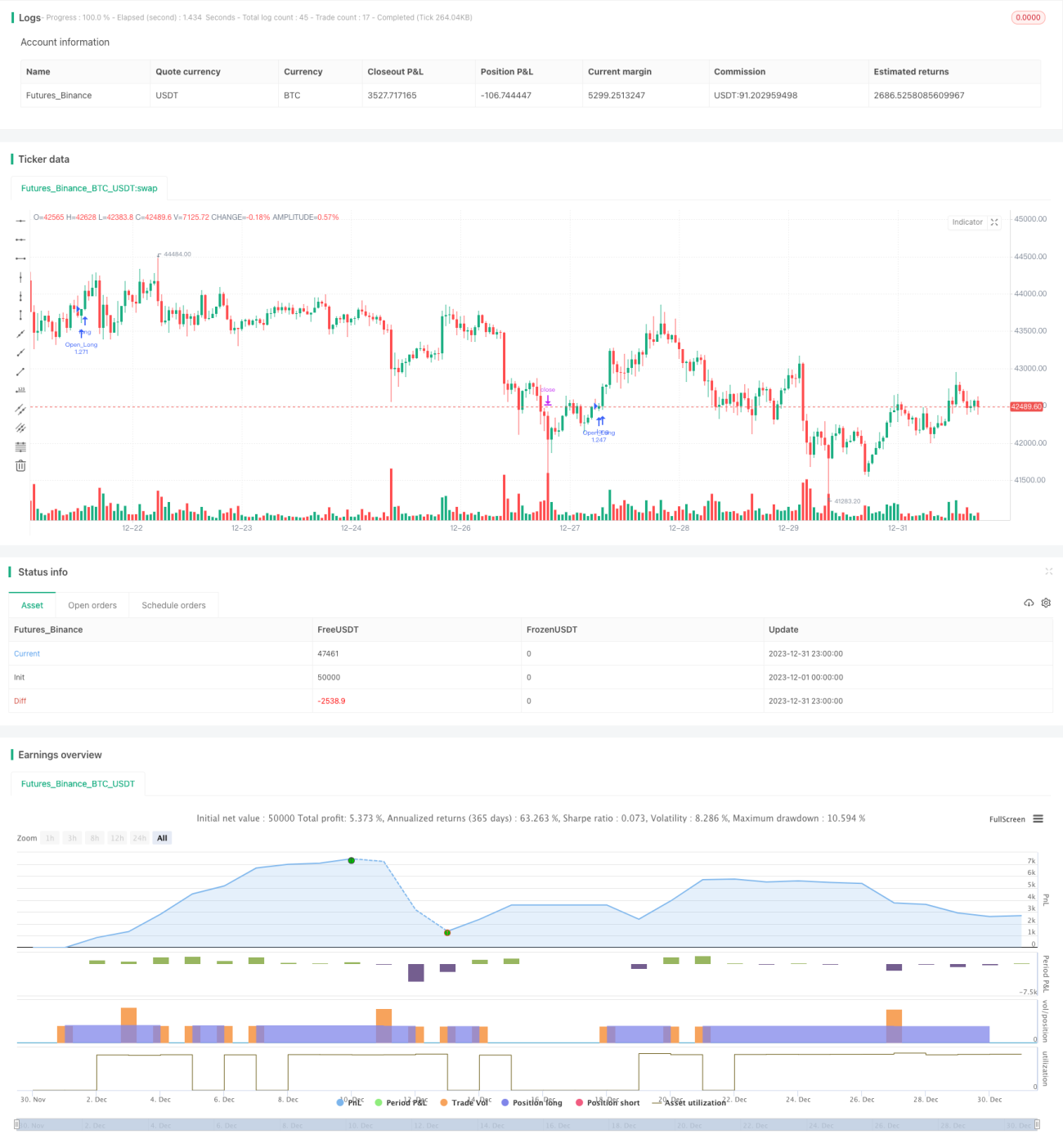

Chiến lược này thiết lập các quy tắc nhận dạng mô hình nến đơn giản để thực hiện giao dịch đột phá vị thế mua trên khung 4 giờ của Tesla. Chiến lược có ưu điểm là triển khai đơn giản, logic rõ ràng, dễ hiểu.

Nguyên lý chiến lược

Logic phán đoán cốt lõi của chiến lược dựa trên 4 quy tắc mô hình nến sau:

- Giá thấp nhất của nến hiện tại thấp hơn giá mở cửa

- Giá thấp nhất của nến hiện tại thấp hơn giá thấp nhất của nến trước đó

- Giá đóng cửa của nến hiện tại cao hơn giá mở cửa

- Giá đóng cửa của nến hiện tại cao hơn cả giá mở cửa và giá đóng cửa của nến trước đó

Khi đồng thời thỏa mãn cả 4 quy tắc trên, sẽ thực hiện thao tác mở vị thế mua.

Ngoài ra, chiến lược còn thiết lập mức cắt lỗ và chốt lời, khi giá chạm điều kiện chốt lời hoặc cắt lỗ sẽ thực hiện đóng vị thế.

Phân tích ưu điểm

Chiến lược này có những ưu điểm sau:

- Quy tắc nhận dạng nến sử dụng rất đơn giản và trực tiếp, dễ hiểu và dễ thực hành.

- Hoàn toàn dựa trên phán đoán giá thực tế, không sử dụng các chỉ báo kỹ thuật quá phức tạp, kết quả backtest trực quan.

- Khối lượng mã nguồn triển khai nhỏ, hiệu suất chạy cao, dễ dàng tối ưu hóa và cải tiến.

- Có thể điều chỉnh thông số, tự do thiết lập điều kiện cắt lỗ chốt lời, kiểm soát rủi ro.

Phân tích rủi ro

Các rủi ro cần lưu ý chủ yếu:

- Sử dụng khối lượng mở vị thế cố định, không xem xét quản lý vị thế, có thể có rủi ro giao dịch vượt quá mức.

- Không thiết lập bộ lọc, trong thị trường dao động có thể phát sinh quá nhiều giao dịch không hiệu quả.

- Dữ liệu backtest không đủ, có thể gây sai lệch trong đánh giá hiệu quả chiến lược.

Có thể giảm thiểu rủi ro bằng các phương pháp sau:

- Thêm mô-đun quản lý vị thế, điều chỉnh khối lượng giao dịch linh hoạt theo quy mô vốn.

- Tăng điều kiện lọc giao dịch, tránh mở vị thế bừa bãi trong thị trường dao động.

- Thu thập thêm dữ liệu lịch sử, mở rộng độ dài backtest, nâng cao độ tin cậy của kết quả.

Hướng tối ưu hóa

Các hướng có thể tối ưu hóa cho chiến lược này bao gồm:

- Thêm mô-đun quản lý vị thế, xác định quy mô giao dịch theo tỷ lệ sử dụng vốn.

- Thiết kế cơ chế theo dõi cắt lỗ chốt lời, thực hiện thoát linh hoạt.

- Thêm mô-đun lọc giao dịch, tránh giao dịch không hiệu quả.

- Sử dụng phương pháp học máy để tự động tối ưu hóa tham số.

- Hỗ trợ giao dịch chênh lệch giá đa sản phẩm.

Tổng kết

Chiến lược này thực hiện giao dịch đột phá vị thế mua thông qua các quy tắc nhận dạng mô hình nến đơn giản. Mặc dù còn một số không gian cải tiến, nhưng xét về tính đơn giản và trực tiếp, chiến lược này là một chiến lược vị thế mua rất phù hợp cho người mới bắt đầu hiểu và sử dụng. Thông qua tối ưu hóa liên tục, hiệu quả của chiến lược có thể trở nên xuất sắc hơn.

- 1