Chiến lược nâng cao siêu xu hướng

Tổng quan

Chiến lược Siêu Xu Hướng Nâng Cao (Ultra Trend Advanced) là chiến lược được tối ưu hóa và nâng cấp dựa trên chỉ báo Siêu Xu Hướng cổ điển. Nó kết hợp hành động giá, độ biến động và nhiều chỉ báo kỹ thuật khác, nhằm nâng cao chất lượng tín hiệu, giảm nhiễu và bắt chính xác hơn các biến động của xu hướng thị trường.

Nguyên lý chiến lược

Cốt lõi của Chiến lược Siêu Xu Hướng Nâng Cao là đường Siêu Xu Hướng. Nó được tính toán dựa trên biên độ dao động thực và động lượng giá, dùng để đánh giá xu hướng giá tiềm năng và các điểm đảo chiều. Khi giá nằm trên đường Siêu Xu Hướng, điều đó biểu thị xu hướng tăng; ngược lại, biểu thị xu hướng giảm.

Khác với chỉ báo Siêu Xu Hướng truyền thống chỉ xem xét giá đóng cửa và biên độ dao động thực, chiến lược nâng cao còn tích hợp nhiều chiều như khối lượng giao dịch, bộ dao động động lượng và dữ liệu cơ bản để xác minh độ tin cậy của tín hiệu. Phương pháp đa biến này đảm bảo các tín hiệu giao dịch được tạo ra chính xác và đáng tin cậy hơn, ít bị ảnh hưởng bởi nhiễu thị trường.

Phân tích ưu điểm

Ưu điểm chính của Chiến lược Siêu Xu Hướng Nâng Cao là:

-

Đánh giá chính xác hơn diễn biến thị trường, lọc bỏ các phá vỡ giả. Chiến lược này chờ đợi nhiều yếu tố chỉ báo đồng nhất mới phát sinh tín hiệu giao dịch, giúp nâng cao đáng kể tỷ lệ chính xác.

-

Giảm thiểu nhiễu loạn thị trường. Bằng cách sử dụng kết hợp các bộ lọc, có thể loại bỏ một lượng lớn dữ liệu thị trường không quan trọng, giúp nhận định rõ ràng hơn.

-

Tối ưu hóa quản lý rủi ro. Tín hiệu giao dịch rõ ràng giúp nhà giao dịch lên kế hoạch cắt lỗ và chốt lời tốt hơn, từ đó có khả năng kiểm soát rủi ro tốt hơn.

-

Khả năng thích ứng cao. Ngoài việc nhận diện xu hướng, chiến lược này còn có thể kết hợp với các công cụ kỹ thuật khác để xây dựng một hệ thống giao dịch toàn diện và hiệu quả.

Phân tích rủi ro

Chiến lược Siêu Xu Hướng Nâng Cao cũng tồn tại các rủi ro chính sau:

-

Rủi ro cài đặt tham số. Kết hợp tham số chỉ báo không đúng có thể khiến chiến lược mất hiệu quả hoặc sinh ra quá nhiều tín hiệu sai.

-

Rủi ro nhận định xu hướng sai. Bất kỳ chiến lược nào cũng không thể hoàn toàn tránh khỏi rủi ro nhận định sai, khi xu hướng thay đổi bất ngờ có thể dẫn đến thua lỗ.

-

Rủi ro tối ưu quá mức. Khi tham số được điều chỉnh đến mức quá chính xác, sẽ quá phụ thuộc vào dữ liệu lịch sử, không thích ứng được với biến động thị trường.

-

Rủi ro chi phí giao dịch. Khi số lần giao dịch tăng lên, chi phí giao dịch như phí hoa hồng và trượt giá cũng tăng đáng kể.

Giải pháp tương ứng:

-

Tối ưu hóa cài đặt tham số, kiểm tra độ vững chắc của tham số thông qua backtest định kỳ.

-

Đặt cắt lỗ và chốt lời, kiểm soát mức lỗ cho mỗi giao dịch.

-

Tránh tối ưu quá mức, duy trì khả năng khái quát hóa của tham số.

-

Tính toán tỷ lệ rủi ro/lợi nhuận của tín hiệu, kiểm soát chi phí giao dịch.

Hướng tối ưu

Chiến lược Siêu Xu Hướng Nâng Cao có thể được tối ưu theo các hướng sau:

-

Điều chỉnh tham số theo từng thị trường khác nhau để phù hợp hơn với đặc điểm của thị trường đó. Ví dụ, trong thị trường biến động có thể rút ngắn chu kỳ tính toán.

-

Thêm cơ chế lọc thích ứng. Khi thị trường bước vào trạng thái đặc biệt, tự động điều chỉnh tham số chỉ báo hoặc vô hiệu hóa một số bộ lọc.

-

Khám phá phương pháp học máy, sử dụng các mô hình huấn luyện như mạng nơ-ron để tối ưu tham số động.

-

Kết hợp chỉ báo tâm lý và tin tức tình báo, sử dụng dữ liệu phi cấu trúc để nâng cao hiệu quả.

-

Thêm chức năng quy mô vị thế mục tiêu. Khi tỷ lệ thắng cao, có thể tăng lợi nhuận bằng cách gia tăng vị thế.

Tổng kết

Chiến lược Siêu Xu Hướng Nâng Cao thông qua việc đưa vào nhiều bộ lọc và chỉ báo xác nhận, đã tối ưu và cải tiến chỉ báo Siêu Xu Hướng cổ điển, giúp đánh giá chính xác hơn diễn biến thị trường và nâng cao chất lượng tín hiệu. So với chỉ báo đơn lẻ, chiến lược này cung cấp một giải pháp giao dịch ổn định, toàn diện và hiệu quả hơn. Tuy nhiên, cũng cần cảnh giác với rủi ro do điều chỉnh tham số không đúng và nhận định sai, đồng thời áp dụng các biện pháp kiểm soát rủi ro thích hợp. Thông qua việc tiếp tục tối ưu và kết hợp sử dụng với các công cụ khác, Chiến lược Siêu Xu Hướng Nâng Cao có tiềm năng ứng dụng rất lớn.

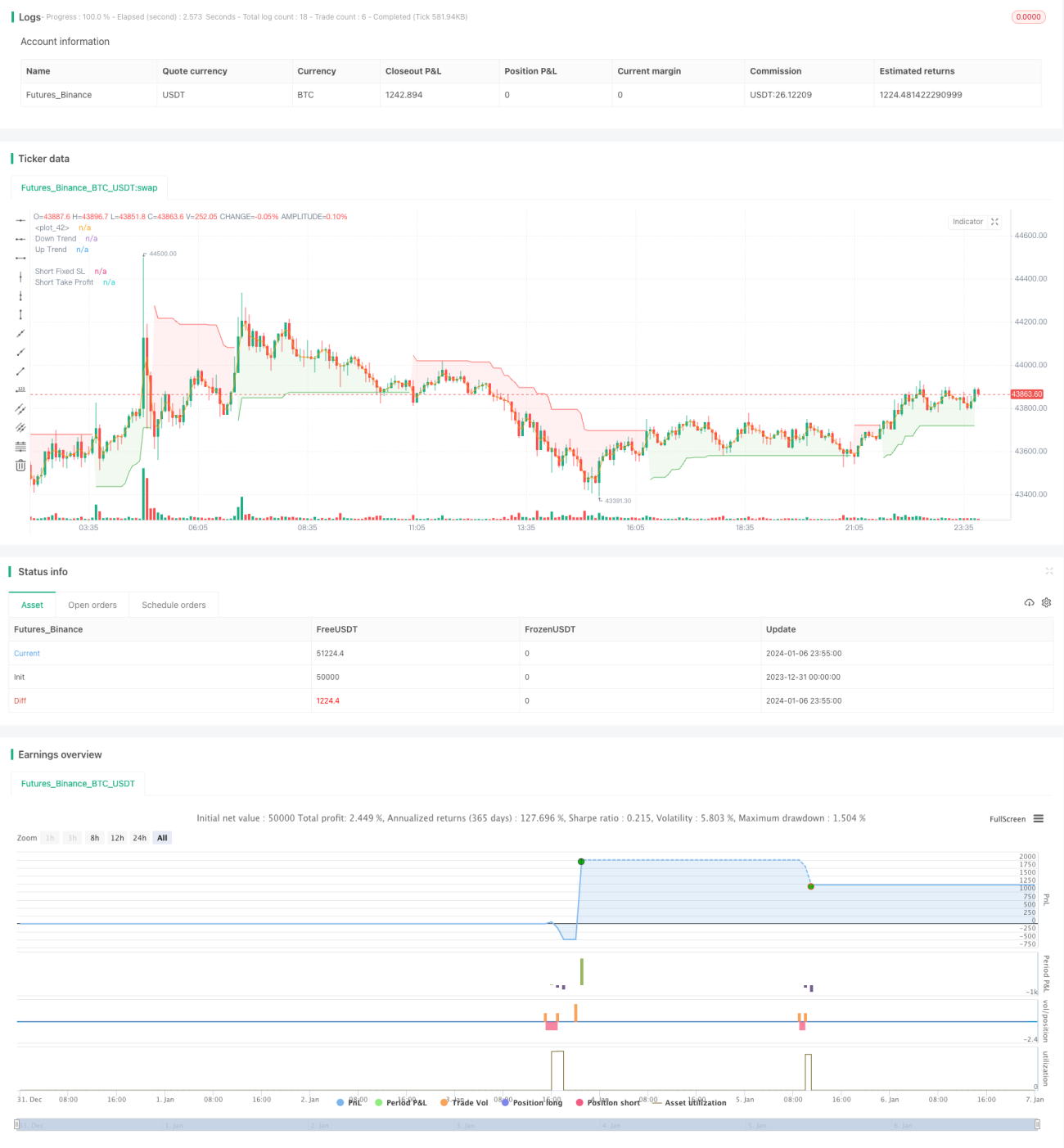

/*backtest

start: 2023-12-31 00:00:00

end: 2024-01-07 00:00:00

period: 5m

basePeriod: 1m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This Pine Script™ code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © JS_TechTrading

//@version=5- 1