Chiến lược tạo lập thị trường dải Bollinger với lệnh giới hạn

Tổng quan

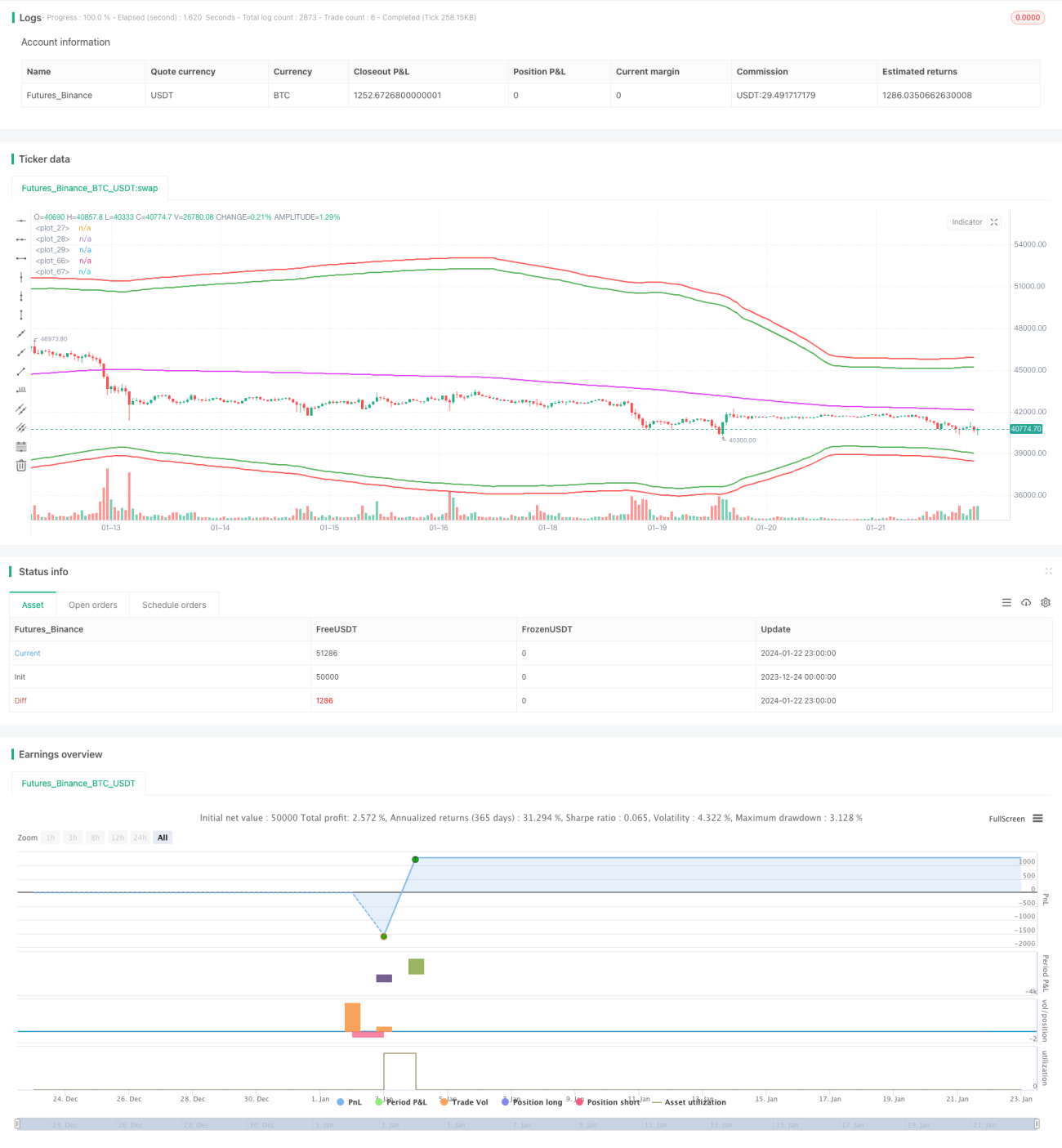

Chiến lược này là một chiến lược market-making sử dụng Bollinger Bands để vào lệnh, đường trung bình động (MA) để thoát lệnh và tỷ lệ dừng lỗ phần trăm đơn giản để quản lý rủi ro. Nó đã đạt được lợi nhuận cực cao trên hợp đồng XTBUSD vào tháng 6 năm 2022.

Nguyên lý chiến lược

Chiến lược này sử dụng các dải trên và dưới của Bollinger Bands làm vùng cơ hội để mở vị thế. Cụ thể, khi giá thấp hơn dải dưới, sẽ mở vị thế mua (long); khi giá cao hơn dải trên, sẽ mở vị thế bán (short).

Ngoài ra, chiến lược cũng sử dụng đường trung bình động làm cơ sở để đóng vị thế. Khi đang nắm giữ vị thế mua, nếu giá cao hơn đường trung bình động, sẽ chọn đóng vị thế; tương tự, khi đang nắm giữ vị thế bán, nếu giá thấp hơn đường trung bình động, cũng sẽ chọn đóng vị thế.

Đối với dừng lỗ, chiến lược này sử dụng cách dừng lỗ cuốn chiếu đơn giản dựa trên giá vào lệnh nhân với một tỷ lệ phần trăm nhất định. Điều này có thể tránh hiệu quả các khoản lỗ lớn trong trường hợp thị trường một chiều.

Phân tích ưu điểm

Các ưu điểm chính của chiến lược này như sau:

- Sử dụng Bollinger Bands có thể nắm bắt hiệu quả sự biến động của giá, thu được nhiều cơ hội giao dịch hơn khi biến động gia tăng.

- Chiến lược market-making có thể thu được phí giao dịch từ cả hai phía mua và bán thông qua giao dịch hai chiều.

- Áp dụng dừng lỗ theo tỷ lệ phần trăm có thể chủ động kiểm soát rủi ro, tránh hiệu quả các khoản lỗ cực lớn trong thị trường một chiều.

Phân tích rủi ro

Chiến lược này cũng tồn tại một số rủi ro:

- Bollinger Bands không phải lúc nào cũng là một chỉ báo vào lệnh đáng tin cậy, đôi khi có thể phát ra tín hiệu sai.

- Chiến lược market-making dễ bị mắc kẹt trong thị trường đi ngang (dao động).

- Dừng lỗ theo tỷ lệ phần trăm có thể quá độc đoán, không thể linh hoạt ứng phó với các diễn biến phức tạp của thị trường.

Để giảm thiểu những rủi ro này, chúng ta có thể cân nhắc kết hợp các chỉ báo khác để lọc, tối ưu hóa cài đặt chiến lược dừng lỗ, hoặc hạn chế quy mô vị thế một cách phù hợp.

Hướng tối ưu hóa

Chiến lược này còn có không gian tối ưu hóa thêm:

- Có thể kiểm tra các tổ hợp tham số khác nhau để tìm ra tham số tối ưu.

- Có thể thêm nhiều chỉ báo lọc hơn để xác nhận đa yếu tố.

- Có thể sử dụng phương pháp học máy để tự động tối ưu hóa tham số.

- Có thể cân nhắc sử dụng phương pháp dừng lỗ tinh vi hơn, chẳng hạn như dừng lỗ parabol (Parabolic SAR).

Tổng kết

Nhìn chung, chiến lược này là một chiến lược market-making tần suất cao rất có lợi nhuận. Nó tận dụng Bollinger Bands để cung cấp cơ hội giao dịch, đồng thời kiểm soát rủi ro. Nhưng chúng ta cũng cần nhận thức được các vấn đề và hạn chế của nó, và cẩn thận kiểm chứng trong giao dịch thực tế. Thông qua tối ưu hóa thêm, chiến lược này có tiềm năng tạo ra lợi nhuận siêu cao ổn định hơn.

- 1