Chiến lược cắt lỗ và chốt lời theo xu hướng

Tổng quan

Đây là một chiến lược giao dịch theo xu hướng dựa trên chỉ báo Bollinger Bands để xác định xu hướng và sử dụng chỉ báo ATR để thiết lập điểm dừng lỗ/chốt lời. Chiến lược này trước tiên xác định xu hướng thị trường, vẽ đường ENVIRONMENT, và thiết lập các điểm dừng lỗ/chốt lời khi đóng vị thế.

Nguyên lý chiến lược

- Tính toán dải trên và dải dưới của Bollinger Bands.

- Xác định xem giá đóng cửa có cao hơn dải trên hoặc thấp hơn dải dưới hay không. Nếu có, xem đó là thị trường có xu hướng, lần lượt là thị trường tăng và thị trường giảm.

- Nếu là thị trường có xu hướng, tính đường môi trường (Environmental line). Đường môi trường được tính dựa trên giá thấp nhất trừ đi giá trị ATR (đối với thị trường tăng) hoặc giá cao nhất cộng với giá trị ATR (đối với thị trường giảm).

- Nếu không phải thị trường có xu hướng, đường môi trường giữ nguyên giá trị của nến trước đó.

- So sánh với đường ENVIRONMENT để xác định hướng xu hướng. Nếu tăng là tăng, giảm là giảm.

- Khi hướng của đường ENVIRONMENT thay đổi, phát sinh tín hiệu mua/bán.

- Thiết lập điểm dừng lỗ/chốt lời: Khoảng cách dừng lỗ cố định là 100 lần giá vào lệnh; khoảng cách chốt lời động là 1,1 lần giá vào lệnh (đối với vị thế tăng) hoặc 0,9 lần giá vào lệnh (đối với vị thế giảm).

Phân tích ưu điểm

- Có khả năng xác định xu hướng thị trường, giảm các giao dịch phá vỡ giả.

- Thiết lập đường ENVIRONMENT, tránh bị mắc kẹt.

- Cài đặt điểm dừng lỗ/chốt lời hợp lý, vừa đảm bảo lợi nhuận vừa kiểm soát rủi ro.

Phân tích rủi ro

- Thiết lập tham số không phù hợp có thể dẫn đến bỏ lỡ cơ hội giao dịch.

- Chỉ báo Bollinger Bands có xác suất sai lệch cao trong thị trường đi ngang.

- Điểm dừng lỗ quá gần có thể khiến lệnh bị thoát ngay lập tức.

Hướng tối ưu hóa

- Tối ưu hóa các tham số của Bollinger Bands để phù hợp hơn với từng loại tài sản.

- Tối ưu hóa cách tính đường ENVIRONMENT, ví dụ như đưa vào các chỉ báo khác.

- Kiểm tra và tối ưu hóa cài đặt điểm dừng lỗ/chốt lời.

Kết luận

Đây là chiến lược sử dụng Bollinger Bands để xác định xu hướng và tận dụng đường ENVIRONMENT để thiết lập điểm dừng lỗ/chốt lời. Ưu điểm cốt lõi là xác định xu hướng rõ ràng, cài đặt điểm dừng lỗ/chốt lời hợp lý, có thể kiểm soát rủi ro hiệu quả. Rủi ro chính nằm ở việc Bollinger Bands xác định sai xu hướng và điểm dừng lỗ quá gần. Hướng tối ưu hóa trong tương lai bao gồm tối ưu hóa tham số, tối ưu hóa cách tính đường ENVIRONMENT và tối ưu hóa điểm dừng lỗ/chốt lời.

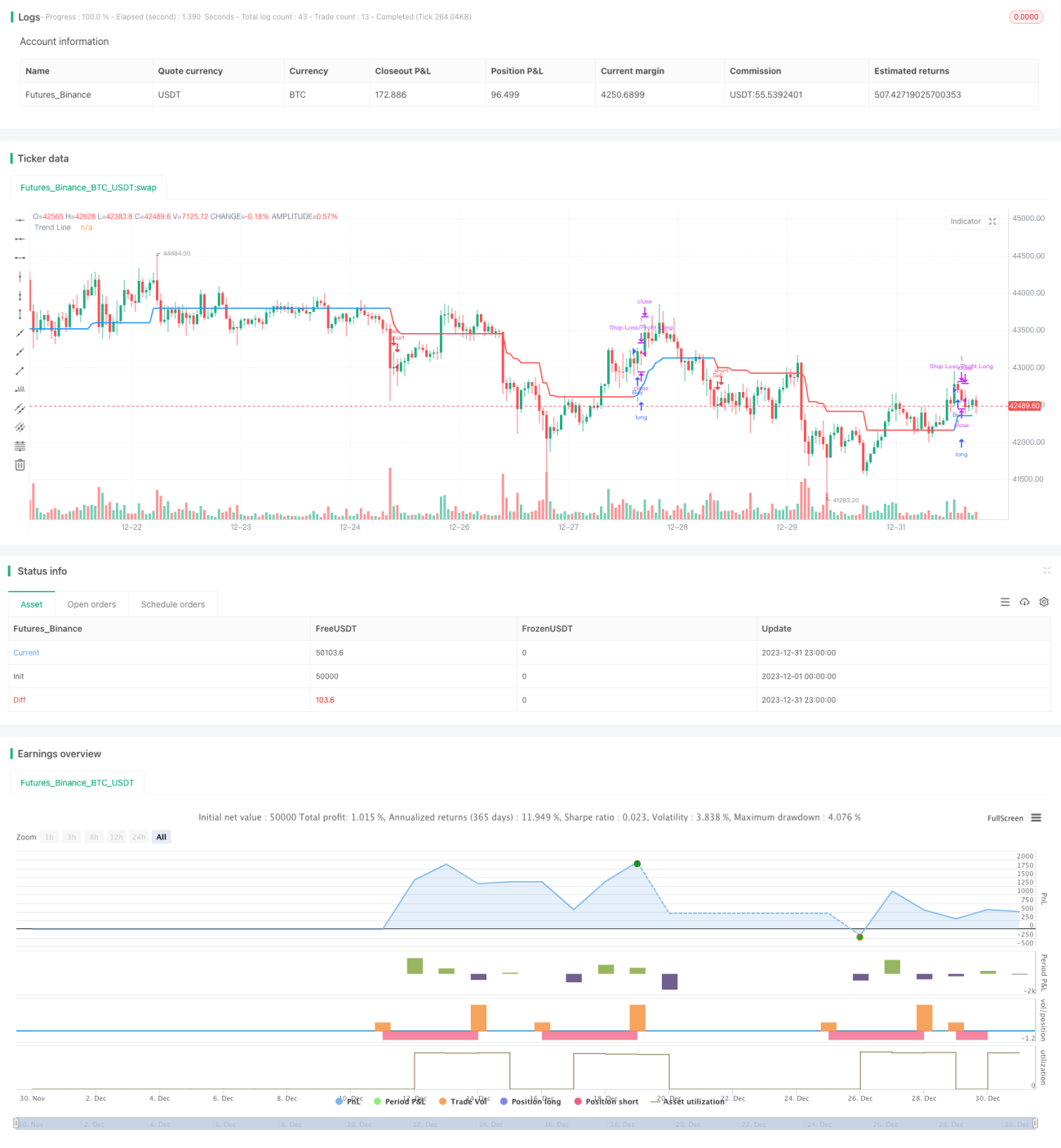

/*backtest

start: 2023-12-01 00:00:00

end: 2023-12-31 23:59:59

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This Pine Script™ code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © zhuenrong

// © Dreadblitz- 1