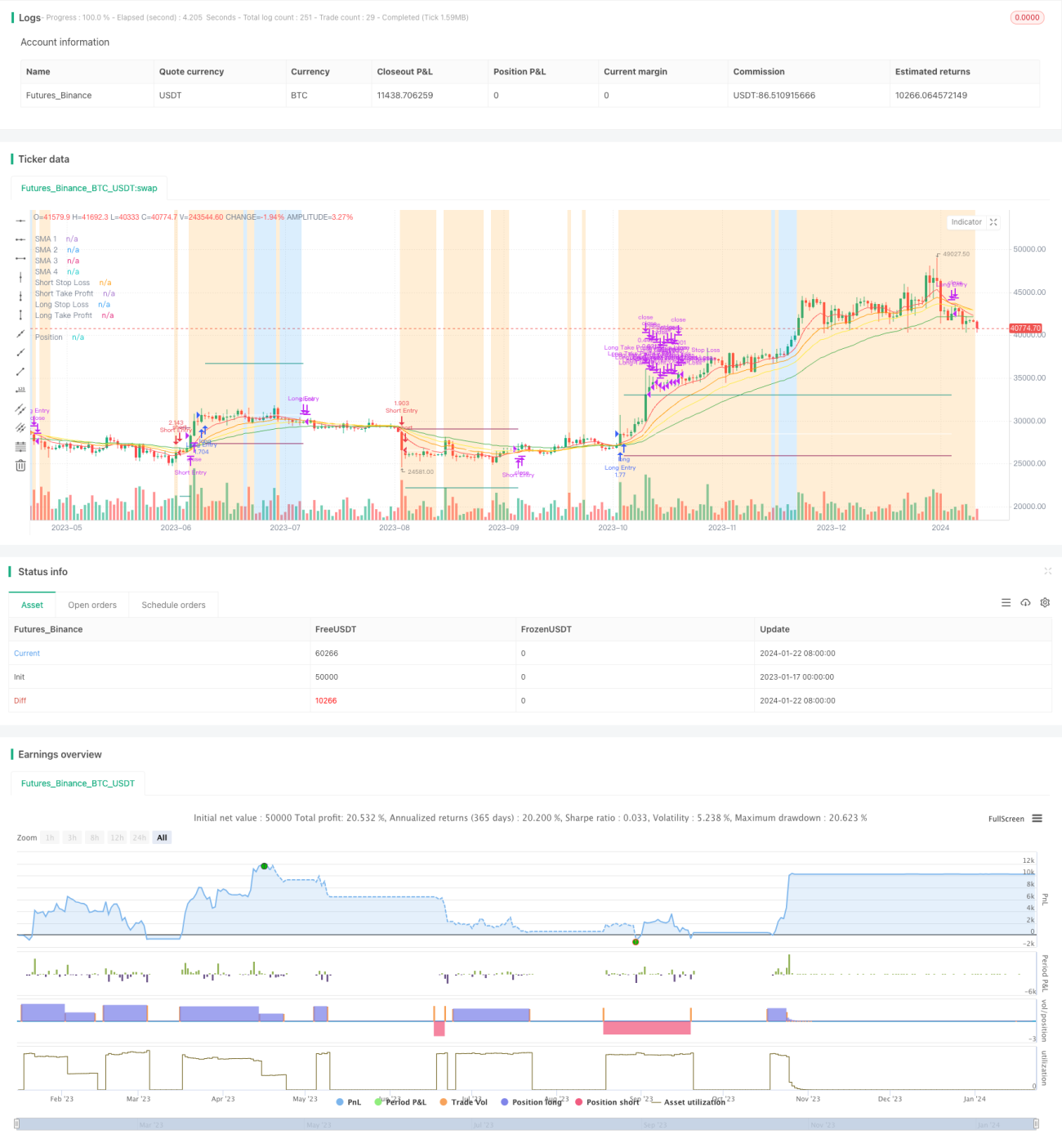

Chiến lược theo xu hướng dựa trên đường trung bình động

Tổng quan

Chiến lược này là một chiến lược theo xu hướng đơn giản dựa trên đường trung bình động. Nó xác định hướng xu hướng hiện tại và thời gian kéo dài của xu hướng bằng cách so sánh mối quan hệ kích thước giữa các đường trung bình động với các chu kỳ khác nhau. Khi đường trung bình động ngắn hạn cắt lên trên đường trung bình động dài hạn, mua vào; khi đường trung bình động ngắn hạn cắt xuống dưới đường trung bình động dài hạn, bán khống. Đồng thời, chiến lược cũng đặt điểm dừng lỗ và điểm chốt lời để kiểm soát rủi ro.

Nguyên lý chiến lược

Chiến lược sử dụng 4 đường trung bình động với các chu kỳ khác nhau: đường 5 ngày, 10 ngày, 15 ngày và 25 ngày. Bốn đường trung bình này được gọi là MA1, MA2, MA3 và MA4. Trong đó, MA1 là ngắn nhất, MA4 là dài nhất.

Khi MA1 > MA2 > MA3 > MA4, điều đó cho thấy giá đang trong xu hướng tăng, lúc này mua vào; khi MA1 < MA2 < MA3 < MA4, giá đang trong xu hướng giảm, lúc này bán khống.

Điều kiện mở lệnh mua và bán khống cũng cần đồng thời đáp ứng bộ lọc dừng lỗ ATR, tức là giá trị ATR phải lớn hơn đường trung bình động đơn giản 40 chu kỳ của ATR, điều này có thể tránh phát tín hiệu sai khi biến động giá quá nhỏ.

Lợi thế của chiến lược

Chiến lược này có những lợi thế sau:

- Ý tưởng đơn giản, dễ hiểu, dễ thực hiện.

- Sử dụng nhiều nhóm đường trung bình động để xác định xu hướng là đáng tin cậy.

- Thiết lập điểm chốt lời và dừng lỗ, có thể kiểm soát hiệu quả mức thua lỗ tối đa cho mỗi giao dịch.

- Bộ lọc dừng lỗ ATR có thể tránh phát tín hiệu sai khi biến động giá quá nhỏ.

Phân tích rủi ro

Chiến lược này cũng có những rủi ro sau:

- Trong thị trường biến động mạnh, dễ phát sinh tín hiệu sai.

- Cài đặt tham số (chu kỳ đường trung bình, v.v.) không phù hợp có thể dẫn đến hiệu quả chiến lược kém.

- Không xem xét ảnh hưởng của các yếu tố cơ bản và tin tức quan trọng lên giá.

Để giảm thiểu những rủi ro này, có thể tối ưu hóa tham số một cách thích hợp hoặc thêm các điều kiện bộ lọc khác để nâng cao độ ổn định của chiến lược.

Hướng tối ưu hóa

Hướng tối ưu hóa của chiến lược này bao gồm:

- Kiểm tra các tổ hợp tham số chu kỳ đường trung bình động khác nhau để tìm ra tham số tối ưu.

- Thêm các bộ lọc chỉ báo kỹ thuật khác, như MACD, KDJ, v.v. để đánh giá độ tin cậy của tín hiệu.

- Thêm bộ lọc khối lượng giao dịch, chỉ giao dịch khi khối lượng giao dịch gia tăng.

- Tối ưu hóa chi tiết tham số theo từng loại sản phẩm dựa trên sự khác biệt về tham số giữa các sản phẩm.

- Thêm thuật toán học máy để đánh giá tín hiệu.

Tổng kết

Nhìn chung, chiến lược này là một chiến lược theo xu hướng khá đơn giản, xác định hướng xu hướng thông qua đường trung bình động, và đặt điểm chốt lời/dừng lỗ hợp lý để kiểm soát mức rủi ro. Chiến lược còn nhiều dư địa để tối ưu hóa, có thể cải thiện hơn nữa độ ổn định và khả năng sinh lời của chiến lược thông qua điều chỉnh tham số, thêm bộ lọc, v.v.

- 1