Hệ thống theo dõi thị trường tăng giá

Tổng quan

Hệ thống Bull Tracking là một hệ thống giao dịch cơ học dựa trên xu hướng. Nó sử dụng các chỉ báo xu hướng trên khung thời gian 4 giờ để lọc tín hiệu giao dịch, trong khi vào lệnh được xác định dựa trên các chỉ báo trên khung thời gian 15 phút. Các chỉ báo chính bao gồm RSI, Stochastic và MACD. Ưu điểm của hệ thống này là sự kết hợp đa khung thời gian có thể lọc hiệu quả các tín hiệu giả, đồng thời sử dụng các chỉ báo trên khung thời gian thấp hơn để xác định thời điểm vào lệnh chính xác hơn. Tuy nhiên, hệ thống này cũng có một số rủi ro, chẳng hạn như dễ xảy ra giao dịch quá mức và các vấn đề về phá vỡ giả.

Nguyên lý

Logic cốt lõi của hệ thống này là kết hợp các chỉ báo trên các khung thời gian khác nhau để xác định hướng xu hướng và thời điểm vào lệnh. Cụ thể, RSI, Stochastic và EMA trên khung thời gian 4 giờ đều phải đáp ứng các điều kiện để xác định hướng xu hướng tổng thể. Điều này có thể lọc hiệu quả hầu hết các nhiễu. Đồng thời, RSI, Stochastic, MACD và EMA trên khung thời gian 15 phút cũng phải cùng chiều tăng hoặc giảm để xác định thời điểm vào lệnh cụ thể. Nhờ đó, có thể tìm được các điểm mua bán tốt. Khi cả hai khung thời gian 4 giờ và 15 phút đều phù hợp, hệ thống mới phát ra tín hiệu giao dịch.

Ưu điểm

- Kết hợp đa khung thời gian, có thể lọc hiệu quả các tín hiệu giả và xác định xu hướng chính

- Chỉ báo chi tiết trên khung 15 phút cho phép xác định thời điểm vào lệnh khá chính xác

- Sử dụng kết hợp các chỉ báo phổ biến như RSI, Stochastic, MACD, dễ hiểu và dễ tối ưu hóa

- Áp dụng các biện pháp quản lý rủi ro nghiêm ngặt như chốt lời, cắt lỗ và trailing stop, giúp kiểm soát hiệu quả rủi ro cho mỗi giao dịch

Rủi ro

- Rủi ro giao dịch quá mức. Hệ thống này nhạy cảm với khung thời gian ngắn, có thể tạo ra nhiều tín hiệu giao dịch, dẫn đến giao dịch quá mức

- Rủi ro phá vỡ giả. Chỉ báo trên khung thời gian ngắn có thể đánh giá sai, tạo ra tín hiệu phá vỡ giả

- Rủi ro chỉ báo mất hiệu lực. Bản thân các chỉ báo kỹ thuật có một số hạn chế nhất định, có thể mất hiệu lực trong các điều kiện thị trường cực đoan

Tương ứng, có thể tối ưu hóa hệ thống từ các khía cạnh sau:

- Điều chỉnh tham số chỉ báo để phù hợp hơn với các môi trường thị trường khác nhau

- Thêm các điều kiện lọc để giảm tần suất giao dịch, ngăn ngừa giao dịch quá mức

- Tối ưu hóa chiến lược chốt lời/cắt lỗ để phù hợp hơn với biên độ dao động của thị trường

- Thử nghiệm các tổ hợp chỉ báo khác nhau để tìm ra giải pháp tối ưu

Kết luận

Nhìn chung, hệ thống Bull Tracking là một hệ thống giao dịch cơ học theo xu hướng rất thực tế. Nó sử dụng các chỉ báo kết hợp đa khung thời gian để xác định xu hướng thị trường và thời điểm vào lệnh quan trọng. Với việc thiết lập tham số hợp lý và kiểm tra tối ưu liên tục, hệ thống này có thể thích ứng với hầu hết các điều kiện thị trường, đạt được hiệu quả lợi nhuận ổn định. Tuy nhiên, chúng ta cũng cần nhận thức được một số rủi ro tiềm ẩn và thực hiện các biện pháp tích cực để phòng ngừa và giải quyết các rủi ro này.

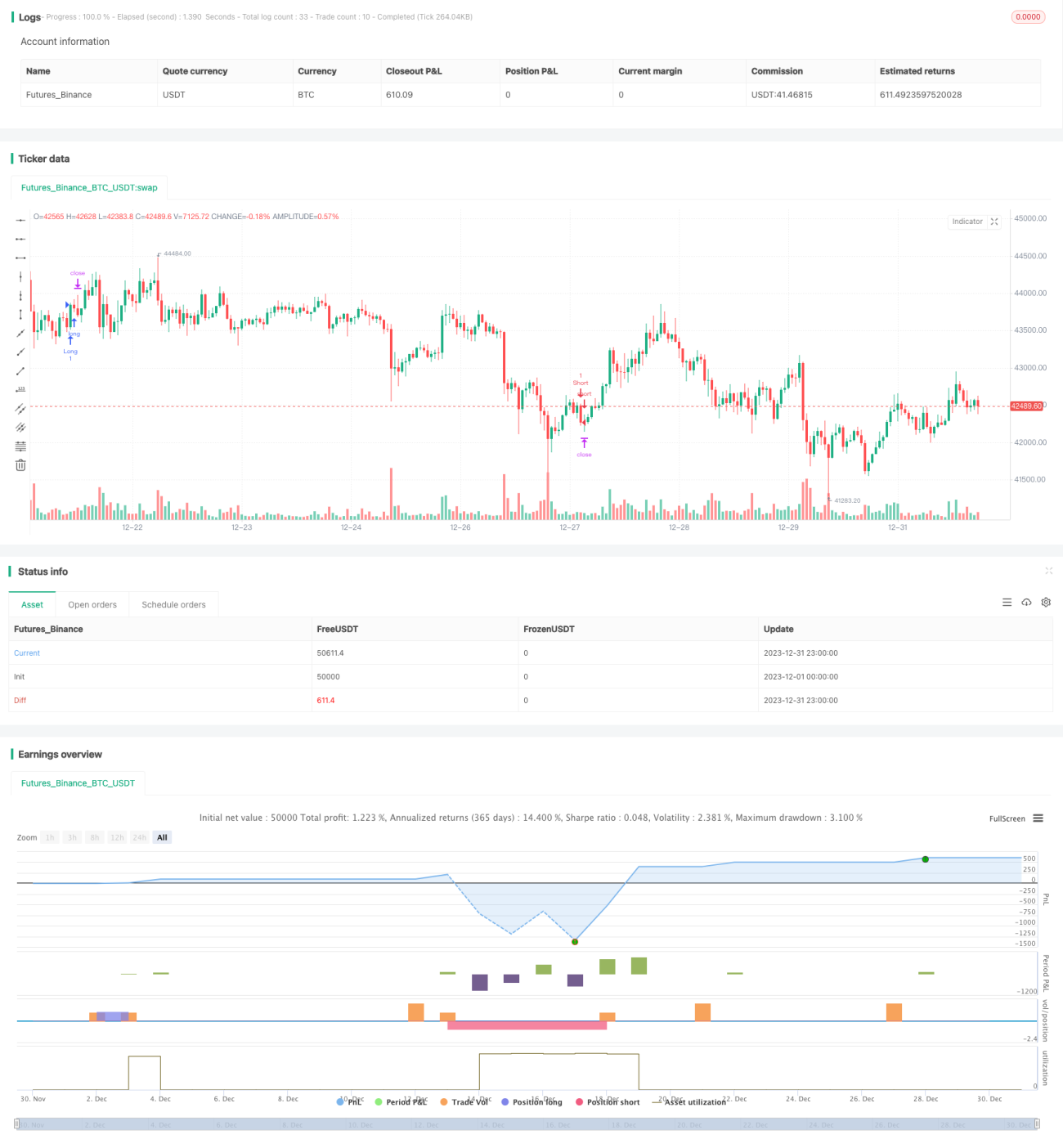

/*backtest

start: 2023-12-01 00:00:00

end: 2023-12-31 23:59:59

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

strategy("Cowabunga System from babypips.com", overlay=true)

// 4 Hour Stochastics

length4 = input(162, minval=1, title="4h StochLength"), smoothK4 = input(48, minval=1, title="4h StochK"), smoothD4 = input(48, minval=1, title="4h StochD")- 1