Chiến lược đảo chiều xu hướng ba cây nến

Tổng quan

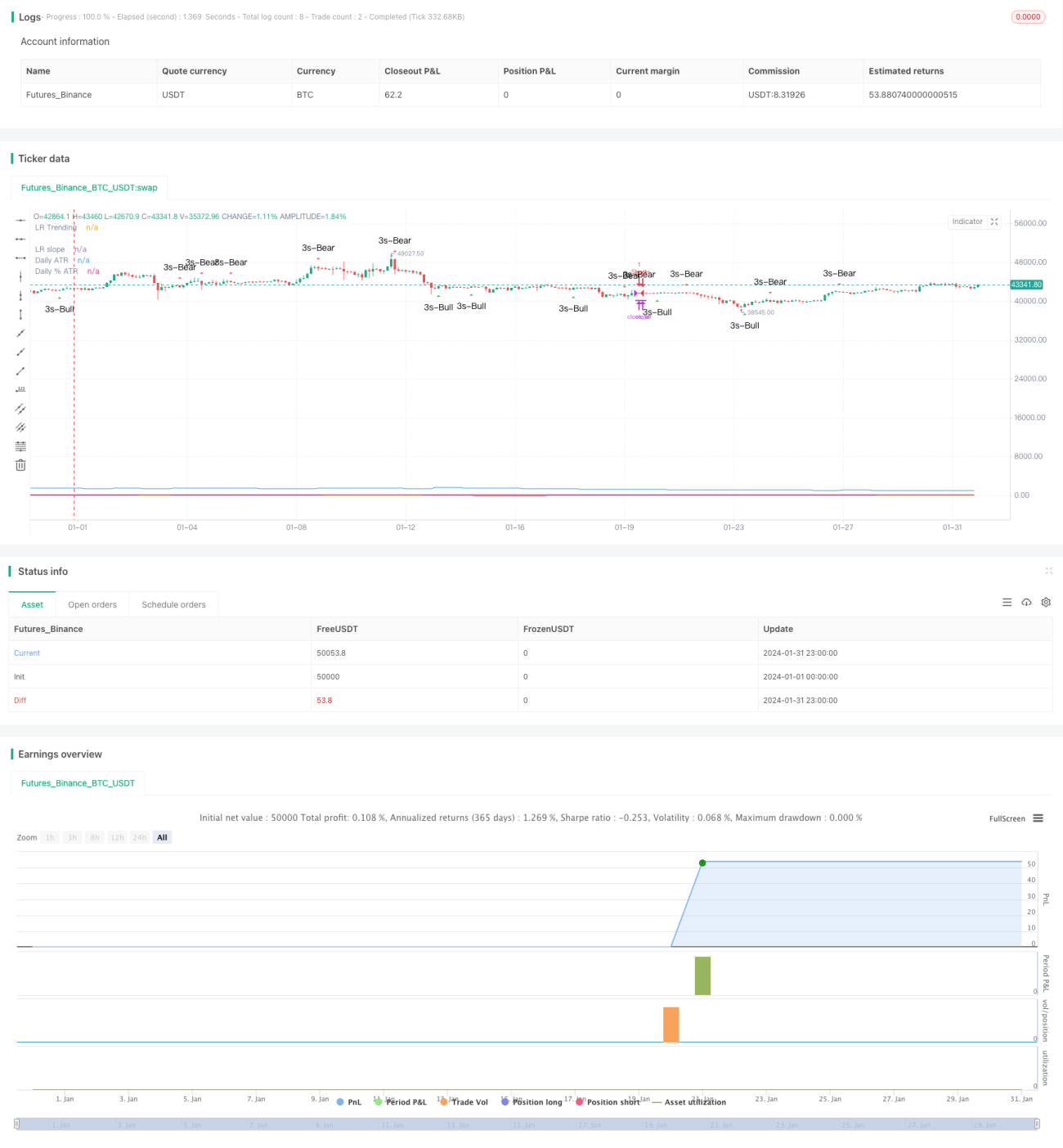

Chiến lược đảo chiều xu hướng ba nến (Three Candle Reversal Trend Strategy) là một chiến lược giao dịch ngắn hạn. Nó xác định sự đảo chiều xu hướng ngắn hạn bằng cách nhận diện ba cây nến tăng hoặc giảm liên tiếp, sau đó là một cây nến nhấn chìm (engulfing) theo hướng ngược lại. Kết hợp với nhiều chỉ báo kỹ thuật để lọc điểm vào lệnh. Chiến lược này giao dịch với tỷ lệ dừng lỗ/chốt lời 1:3, giúp thu được lợi nhuận vượt trội.

Nguyên lý chiến lược

Logic cốt lõi của chiến lược là nhận diện mô hình nến ba cây tăng hoặc giảm liên tiếp, mô hình này thường báo hiệu sự đảo chiều xu hướng ngắn hạn. Khi phát hiện ba cây nến giảm liên tiếp, chờ đến khi xuất hiện cây nến tăng nhấn chìm tiếp theo, thì vào lệnh mua (long). Ngược lại, khi phát hiện ba cây nến tăng liên tiếp, chờ đến khi xuất hiện cây nến giảm nhấn chìm tiếp theo, thì vào lệnh bán (short). Điều này giúp nắm bắt kịp thời cơ hội đảo chiều xu hướng ngắn hạn.

Ngoài ra, chiến lược còn đưa vào nhiều chỉ báo kỹ thuật để lọc điểm vào lệnh. Sử dụng hai đường SMA với tham số khác nhau, chỉ xem xét vào lệnh khi đường nhanh cắt lên đường chậm. Đồng thời, sử dụng chỉ báo hồi quy tuyến tính (linear regression) để đánh giá trạng thái dao động (range-bound) hay xu hướng của thị trường, chỉ giao dịch khi đang trong trạng thái xu hướng. Chiến lược cũng cung cấp một công tắc (switch) cho phép lựa chọn có kết hợp mô hình nến với điểm giao cắt vàng (golden cross) của đường trung bình hay không. Thông qua sự kết hợp toàn diện của các chỉ báo này, có thể lọc bỏ phần lớn nhiễu và nâng cao độ chính xác khi vào lệnh.

Về cài đặt dừng lỗ và chốt lời, chiến lược yêu cầu tỷ lệ rủi ro/lợi nhuận không thấp hơn 1:3. Bằng cách tính toán chỉ báo ATR dựa trên biên độ dao động của N cây nến gần nhất, kết hợp với phần trăm biên độ để đặt mức dừng lỗ, từ đó tính toán mức chốt lời. Điều này cho phép đạt được lợi nhuận vượt trội hợp lý trong khi chấp nhận một mức rủi ro nhất định.

Lợi thế của chiến lược

Chiến lược đảo chiều xu hướng ba nến có những lợi thế sau:

- Xác định điểm đảo chiều xu hướng ngắn hạn, nắm bắt cơ hội kịp thời.

- Nhiều chỉ báo lọc giúp tăng độ chính xác khi vào lệnh.

- Cơ chế dừng lỗ/chốt lời hợp lý, tỷ lệ rủi ro/lợi nhuận vừa phải.

- Tham số đơn giản, dễ hiểu và dễ thao tác.

Rủi ro của chiến lược

Chiến lược này cũng tồn tại một số rủi ro cần lưu ý:

- Đảo chiều ngắn hạn không nhất thiết đại diện cho đảo chiều xu hướng dài hạn, cần chú ý đến xu hướng khung thời gian cao hơn. Có thể thiết lập đường trung bình dài hạn hơn làm bộ lọc.

- Tín hiệu từ mô hình nến đơn lẻ có thể bị nhầm lẫn, có thể cân nhắc thêm các tín hiệu hỗ trợ khác.

- Cài đặt điểm dừng lỗ có thể quá lạc quan, có thể thu hẹp phạm vi dừng lỗ phù hợp.

- Dữ liệu backtest chưa đầy đủ, hiệu suất giao dịch thực tế có thể có độ bất định nhất định.

Hướng tối ưu hóa chiến lược

Chiến lược có thể được tối ưu hóa theo các hướng sau:

- Điều chỉnh tham số đường trung bình và hồi quy tuyến tính để cải thiện hiệu quả đánh giá trạng thái xu hướng.

- Thêm các chỉ báo hỗ trợ khác như Stochastics để tối ưu độ chính xác của tín hiệu.

- Tối ưu cài đặt tham số ATR và biên độ dừng lỗ để cân bằng rủi ro và lợi nhuận.

- Bổ sung cơ chế theo dõi điểm phá vỡ xu hướng để tăng khả năng sinh lời.

- Xây dựng chiến lược quản lý vốn chặt chẽ hơn để kiểm soát rủi ro giao dịch.

Tổng kết

Nhìn chung, chiến lược đảo chiều xu hướng ba nến là một chiến lược giao dịch ngắn hạn sử dụng mô hình giá đơn giản kết hợp với nhiều chỉ báo hỗ trợ, dựa trên nền tảng cân bằng rủi ro/lợi nhuận hợp lý. Với độ phức tạp thấp, nó mang lại hiệu suất khả quan, đáng để các nhà đầu tư quan tâm và thử nghiệm, đồng thời có nhiều không gian để cải tiến. Thông qua tối ưu tham số và bổ sung quy tắc, nó có tiềm năng phát triển thành một chiến lược giao dịch định lượng ổn định và hiệu quả.

/*backtest

start: 2024-01-01 00:00:00

end: 2024-01-31 23:59:59

period: 3h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © platsn

//

// Mainly developed for SPY trading on 1 min chart. But feel free to try on other tickers.- 1