## Chiến lược giao dịch định lượng hoàn toàn mới dựa trên mô hình ABCD kết hợp dừng lỗ theo dõi và chốt lời theo dõi

1. Tổng quan chiến lược

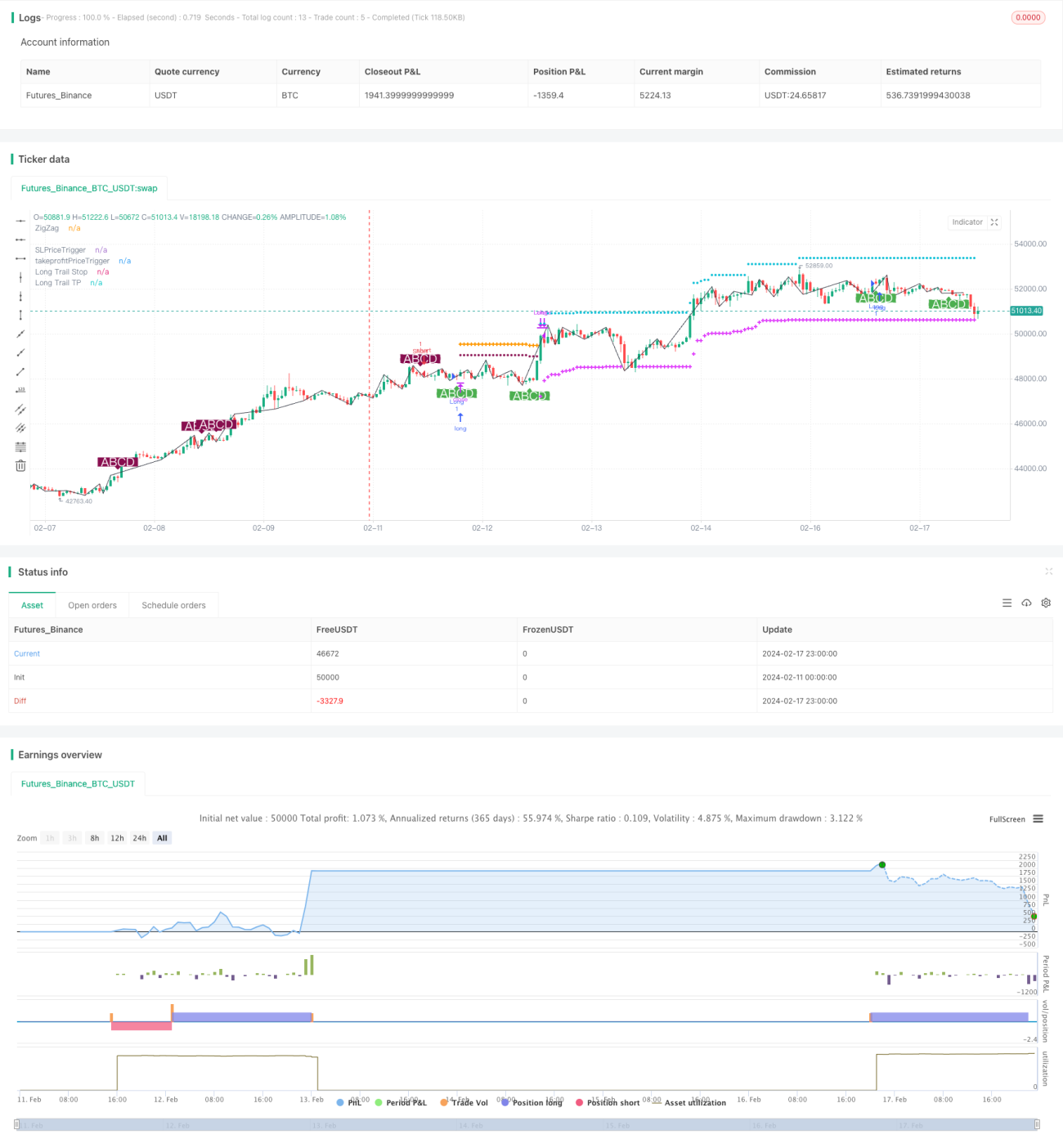

Chiến lược này có tên là "Chiến lược giao dịch mô hình ABCD tối ưu (Có trailing stop loss và trailing take profit)". Đây là một chiến lược định lượng dựa trên mô hình giá ABCD rõ ràng để thực hiện các giao dịch. Ý tưởng chính là sau khi nhận diện được mô hình ABCD hoàn chỉnh, sẽ mua hoặc bán theo hướng của mô hình, đồng thời thiết lập trailing stop loss và trailing take profit để quản lý vị thế.

2. Nguyên lý chiến lược

-

Sử dụng phương pháp hỗ trợ của Bollinger Bands để nhận diện các điểm đỉnh đáy của giá, từ đó có được đường ZigZag.

-

Trên đường ZigZag, nhận diện mô hình ABCD hoàn chỉnh. Bốn điểm A, B, C, D cần thỏa mãn một tỷ lệ nhất định. Sau khi nhận diện được mô hình ABCD phù hợp, sẽ mua hoặc bán.

-

Sau khi mua/bán, thiết lập trailing stop loss để kiểm soát rủi ro. Stop loss ban đầu sử dụng stop loss cố định, khi lợi nhuận đạt đến một tỷ lệ nhất định sẽ chuyển sang trailing stop để khóa một phần lợi nhuận.

-

Tương tự, take profit cũng được thiết lập trailing để kịp thời chốt lời sau khi đạt đủ lợi nhuận, tránh lợi nhuận bị thoái lui. Trailing take profit cũng chia làm hai giai đoạn: đầu tiên sử dụng take profit cố định để thu một phần lợi nhuận, sau đó chuyển sang trailing take profit để tiếp tục theo dõi giá.

-

Khi giá chạm trailing stop loss hoặc trailing take profit, sẽ đóng vị thế, kết thúc một chu kỳ giao dịch.

3. Phân tích ưu điểm chiến lược

-

Sử dụng phương pháp hỗ trợ của Bollinger Bands để nhận diện đường ZigZag, tránh vấn đề retroactive của đường ZigZag truyền thống, làm cho tín hiệu giao dịch đáng tin cậy hơn.

-

Mô hình giao dịch ABCD đã trưởng thành và ổn định, cơ hội giao dịch tương đối dồi dào. Hơn nữa, hướng của mô hình ABCD rõ ràng, dễ dàng xác định hướng vào lệnh.

-

Thiết lập trailing stop loss và take profit hai giai đoạn giúp kiểm soát rủi ro tốt hơn và thu được lợi nhuận. Trailing stop loss và take profit giúp chiến lược linh hoạt hơn.

-

Các tham số chiến lược được thiết kế hợp lý, tỷ lệ stop loss/take profit, tỷ lệ kích hoạt trailing đều có thể tùy chỉnh, rất linh hoạt khi sử dụng.

-

Chiến lược này có thể áp dụng cho bất kỳ sản phẩm nào, bao gồm ngoại hối, tiền điện tử và chỉ số chứng khoán.

4. Phân tích rủi ro chiến lược

-

Mặc dù mô hình ABCD khá rõ ràng, nhưng cơ hội giao dịch tương đối hạn chế, không đảm bảo tần suất giao dịch đủ.

-

Trong thị trường đi ngang (sideways), stop loss và take profit có thể bị kích hoạt thường xuyên. Khi đó cần điều chỉnh tham số phù hợp, mở rộng phạm vi stop loss/take profit.

-

Cần quan tâm đến tính thanh khoản của sản phẩm giao dịch. Với các sản phẩm có thanh khoản thấp, stop loss và take profit khó thực hiện chính xác.

-

Chiến lược khá nhạy cảm với chi phí giao dịch, cần chọn sàn môi giới và tài khoản có phí thấp.

-

Một số tham số có thể tiếp tục tối ưu, chẳng hạn như điều kiện kích hoạt trailing stop loss và take profit có thể thử nghiệm nhiều giá trị khác nhau để tìm ra điểm tối ưu.

5. Hướng tối ưu hóa chiến lược

-

Có thể kết hợp với các chỉ báo khác, thiết lập thêm bộ lọc để tránh một số mô hình giả (HW). Điều này có thể giảm các giao dịch không hiệu quả.

-

Thêm nhận định về cấu trúc ba đoạn của thị trường, chỉ tìm kiếm cơ hội giao dịch trong đoạn thứ ba. Điều này có thể nâng cao tỷ lệ thắng.

-

Thử nghiệm tối ưu quy mô vốn ban đầu, tìm mức vốn ban đầu tốt nhất. Quá lớn hoặc quá nhỏ đều không có lợi cho tỷ suất lợi nhuận tối ưu.

-

Có thể thử nghiệm trên dữ liệu ngoài mẫu (out-of-sample) để xác nhận độ mạnh của tham số. Điều này rất cần thiết để nắm bắt độ ổn định trung và dài hạn của chiến lược.

-

Tiếp tục tối ưu điều kiện kích hoạt trailing stop loss/take profit và kích thước slippage, nâng cao hiệu quả thực thi chiến lược. Tối ưu hóa cài đặt SETTINGS không bao giờ kết thúc.

6. Tổng kết chiến lược

Chiến lược này chủ yếu dựa vào mô hình giá ABCD để nhận diện và vào lệnh. Thiết lập trailing stop loss và take profit hai giai đoạn để quản lý rủi ro và lợi nhuận. Chiến lược khá trưởng thành và ổn định, nhưng tần suất giao dịch có thể thấp. Chúng ta có thể tăng cường bộ lọc để có được cơ hội giao dịch hiệu quả hơn. Ngoài ra, tiếp tục tối ưu tham số và quy mô vốn cũng có thể nâng cao khả năng sinh lời ổn định của chiến lược. Nhìn chung, chiến lược này có tư duy rõ ràng, dễ hiểu và dễ triển khai, là một chiến lược giao dịch định lượng đáng để nghiên cứu và ứng dụng sâu.

- 1