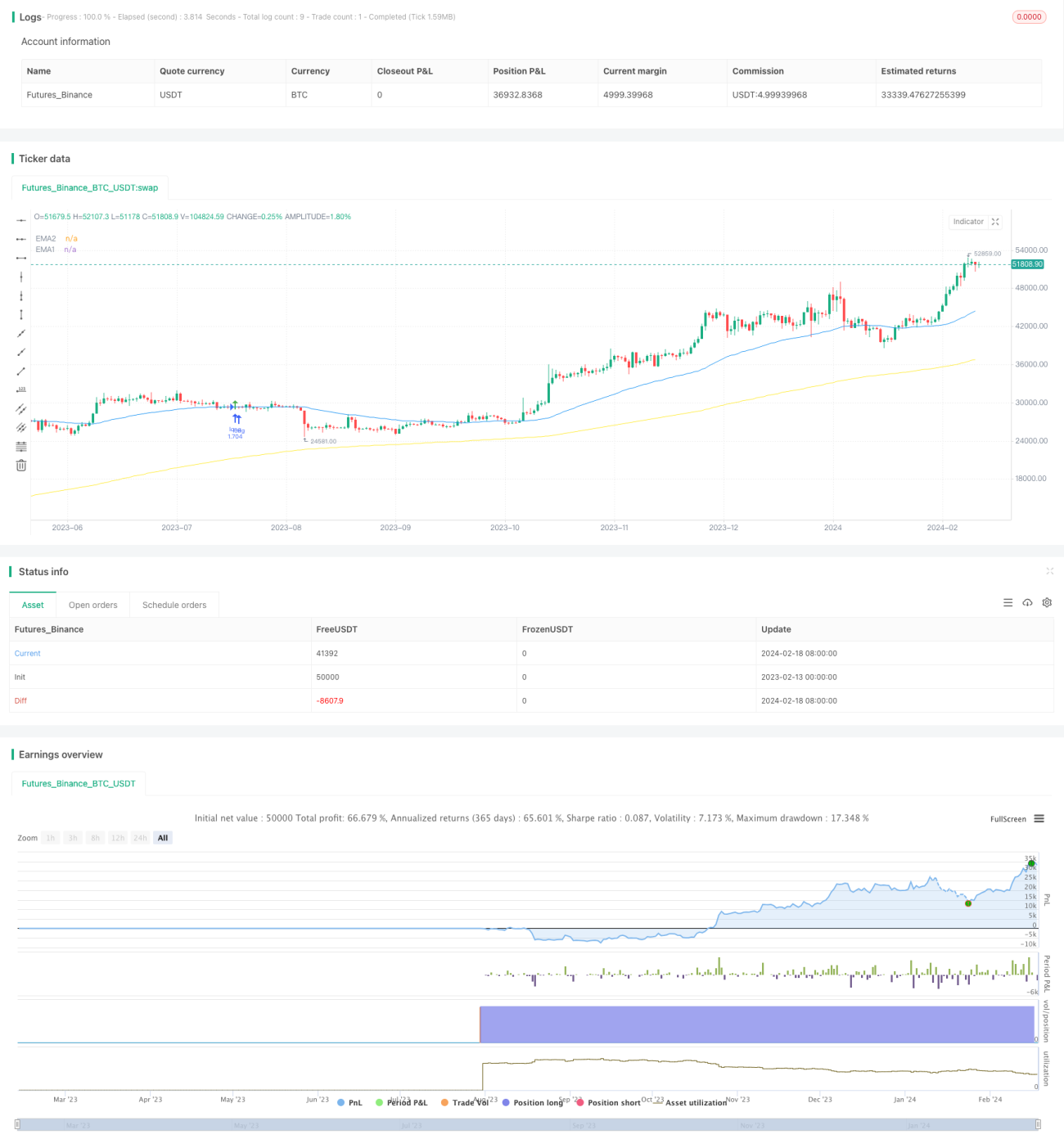

Chiến lược kết hợp chỉ báo đột phá theo dõi xu hướng

Tổng quan

Tên chiến lược này là "Chiến lược giao dịch theo xu hướng kết hợp các chỉ báo đột phá". Chiến lược này kết hợp sử dụng nhiều chỉ báo để nhận diện hướng xu hướng thị trường và thực hiện các giao dịch theo xu hướng. Bao gồm các phần chính sau:

- Sử dụng chỉ báo xu hướng sóng để xác định xu hướng chính của thị trường

- Kết hợp chỉ báo RSI và chỉ báo dòng tiền để loại bỏ một số tín hiệu giả

- Chỉ báo EMA xác định hướng giao dịch cụ thể

- Vào lệnh sử dụng phương pháp đột phá theo xu hướng để đảm bảo đi theo xu hướng

Nguyên lý chiến lược

Chiến lược này chủ yếu xác định hướng và sức mạnh của xu hướng lớn, đồng thời thiết lập giao dịch hai chiều mua và bán. Nguyên lý hoạt động cụ thể như sau:

Tín hiệu vào lệnh mua:

- Giá cao hơn EMA 200 ngày, cho thấy thị trường đang trong xu hướng tăng

- Giá điều chỉnh về gần EMA 50 ngày tạo thành hỗ trợ

- Chỉ báo sóng đảo chiều thành xu hướng tăng và xuất hiện tín hiệu mua

- RSI và MFI đều hiển thị quá mua

- 3 nến liên tiếp lần lượt phá vỡ EMA 50 ngày, cho thấy đột phá lên trên

Tín hiệu vào lệnh bán:

Ngược lại với tín hiệu vào lệnh mua

Phương thức chốt lời cắt lỗ:

Cung cấp hai tùy chọn: cắt lỗ giá thấp nhất/cao nhất, cắt lỗ ATR

Phân tích ưu điểm chiến lược

Chiến lược này có những ưu điểm sau:

- Kết hợp nhiều chỉ báo để xác định xu hướng lớn, tránh đột phá giả

- Sử dụng EMA để xác định hướng giao dịch, dễ dàng theo dõi xu hướng

- Phương pháp cắt lỗ bám sát xu hướng giúp đạt lợi nhuận liên tục

- Có thể đồng thời mua và bán để đi theo bất kỳ hướng nào của thị trường

Phân tích rủi ro chiến lược

Chiến lược này cũng tồn tại một số rủi ro:

- Xác suất chỉ báo phát ra tín hiệu sai

- Điểm cắt lỗ đặt quá nhỏ, làm tăng rủi ro cắt lỗ

- Số lần giao dịch nhiều, phí giao dịch là một khoản tổn thất ẩn

Để giảm thiểu các rủi ro trên, có thể tối ưu hóa từ các khía cạnh sau:

- Điều chỉnh tham số chỉ báo để lọc tín hiệu sai

- Nới rộng điểm cắt lỗ phù hợp

- Tối ưu hóa tham số chỉ báo, giảm số lần giao dịch

Hướng tối ưu hóa chiến lược

Từ góc độ mã code, các hướng tối ưu hóa chính của chiến lược này bao gồm:

- Điều chỉnh tham số của chỉ báo sóng, RSI và MFI để chọn ra tổ hợp tham số tốt nhất

- Kiểm tra hiệu suất của các chu kỳ EMA khác nhau

- Điều chỉnh hệ số tỷ lệ rủi ro/lợi nhuận của chốt lời cắt lỗ để có cấu hình tốt nhất

Thông qua điều chỉnh tham số và kiểm tra, chiến lược có thể tối đa hóa lợi nhuận đồng thời giảm rủi ro sụt giảm.

Tổng kết

Chiến lược này kết hợp nhiều chỉ báo để xác định hướng xu hướng lớn, sử dụng chỉ báo EMA làm tín hiệu giao dịch cụ thể và sử dụng phương pháp cắt lỗ bám sát xu hướng để khóa lợi nhuận. Thông qua tối ưu hóa tham số, có thể đạt được lợi nhuận ổn định tốt. Tuy nhiên, cũng cần lưu ý một số rủi ro hệ thống nhất định, cần liên tục theo dõi hiệu quả của các chỉ báo và sự thay đổi của môi trường thị trường.

- 1