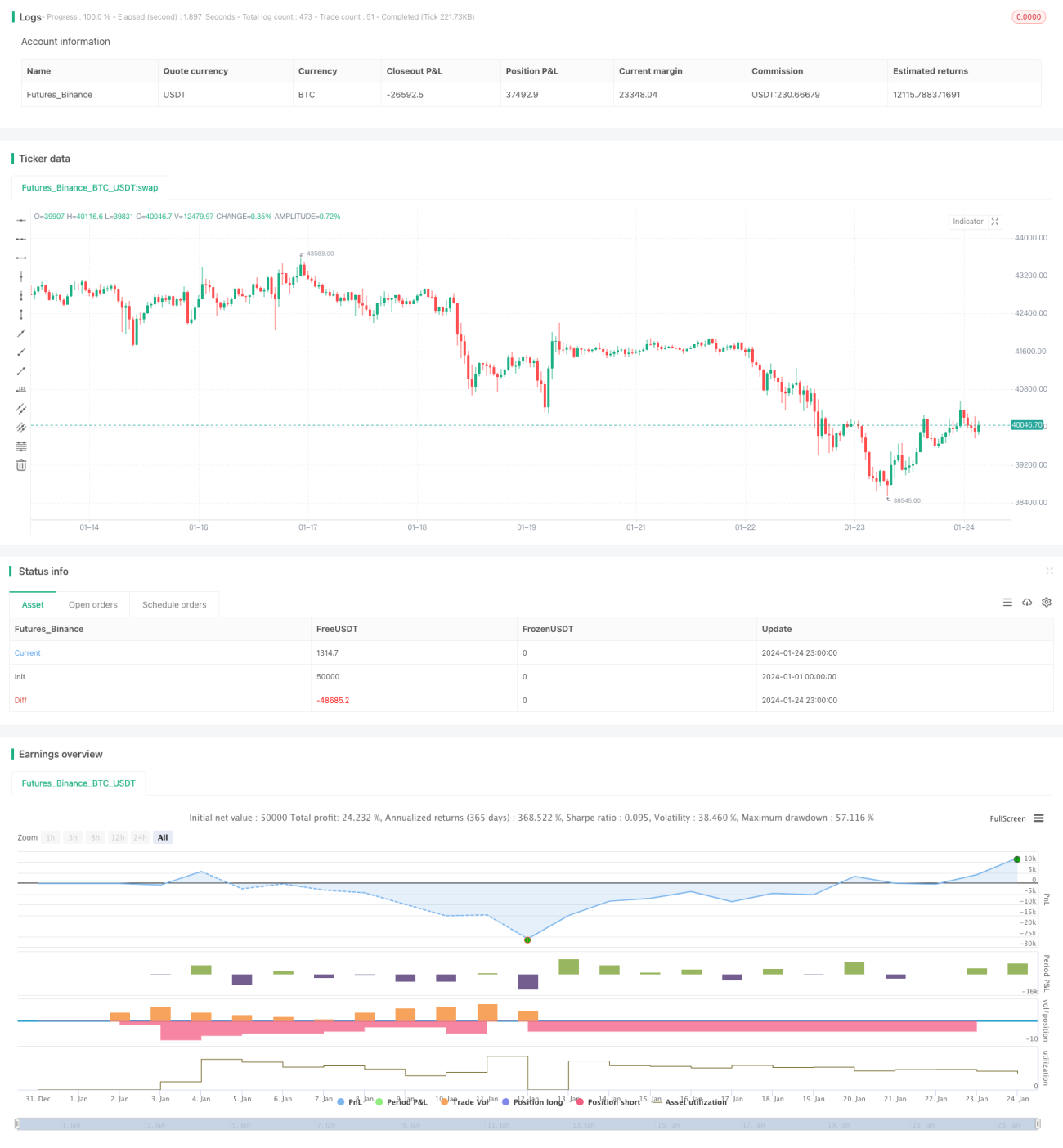

Chiến lược giao dịch lưới thích ứng dựa trên nền tảng giao dịch định lượng

Tổng quan

Chiến lược này là một chiến lược giao dịch lưới thích ứng dựa trên nền tảng giao dịch định lượng. Bằng cách thiết lập phạm vi giao dịch lưới tự động hoặc thủ công, chiến lược đặt các lệnh mua và bán cách đều nhau trong phạm vi đó để thực hiện giao dịch lưới. Khi giá vượt qua giới hạn trên hoặc dưới của lưới, chiến lược sẽ tự động điều chỉnh phạm vi lưới.

Nguyên lý chiến lược

-

Thiết lập giá giới hạn trên và dưới của lưới. Có thể tự động tính toán mức giá cao nhất và thấp nhất trong một khoảng thời gian nhất định của lịch sử làm giới hạn trên và dưới, hoặc thiết lập cố định thủ công.

-

Dựa trên giá giới hạn trên và dưới cùng số lượng ô lưới, tính toán khoảng cách giá giữa các ô lưới.

-

Giữa giá giới hạn trên và dưới, sắp xếp nhiều điểm mua và bán cách đều nhau làm lưới.

-

Khi giá thị trường phá vỡ giới hạn dưới của lưới, đặt lệnh mua tại ô lưới tiếp theo sau ô lưới có lệnh chưa đóng gần nhất; khi giá thị trường phá vỡ giới hạn trên của lưới, đặt lệnh bán tại ô lưới trước đó của ô lưới có lệnh chưa đóng gần nhất.

-

Như vậy, liên tục thực hiện các hoạt động mua bán trong phạm vi giới hạn trên và dưới của lưới. Khi xu hướng giá đảo chiều, các lệnh trước đó sẽ dần chốt lời hoặc cắt lỗ.

Ưu điểm của chiến lược

-

Giao dịch lưới có thể kiếm lợi nhuận trong thị trường đi ngang và dao động.

-

Tự động điều chỉnh phạm vi lưới, có thể tự động điều chỉnh theo biến động thị trường mà không cần can thiệp thủ công.

-

Có thể định trước số vốn đầu tư, phân bổ theo tỷ lệ trên các ô lưới, kiểm soát rủi ro cho mỗi lệnh.

-

Logic đơn giản, dễ hiểu, linh hoạt điều chỉnh tham số.

Rủi ro và biện pháp đối phó

-

Tổn thất do vượt quá giới hạn trên/dưới

- Giải pháp: Thiết lập vị trí dừng lỗ hợp lý.

-

Thua lỗ lặp lại trong thị trường xu hướng

- Giải pháp: Nhận diện xu hướng, tạm dừng giao dịch kịp thời.

-

Thiết lập tham số không phù hợp

- Giải pháp: Điều chỉnh số lượng ô lưới và khoảng cách giá.

Hướng tối ưu hóa

-

Sử dụng học máy để dự đoán phạm vi biến động giá và xu hướng, điều chỉnh tham số lưới một cách linh hoạt.

-

Trong thị trường xu hướng, chuyển sang giao dịch theo xu hướng để tránh thua lỗ từ giao dịch lưới.

-

Kết hợp các chỉ số như tỷ lệ sử dụng vốn, tỷ suất lợi nhuận để kiểm soát rủi ro.

-

Mở rộng sang nhiều loại sản phẩm, tăng phạm vi sử dụng vốn.

Tổng kết

Chiến lược này là một chiến lược lưới thích ứng có thể tự động điều chỉnh tham số, phù hợp với các loại cổ phiếu, tiền điện tử và ngoại hối dao động đi ngang. Với sự điều chỉnh của tham số Parameter, nó có thể thích ứng với các điều kiện thị trường khác nhau, mang lại giá trị thực tiễn nhất định.

/*backtest

start: 2024-01-01 00:00:00

end: 2024-01-24 23:59:59

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

//hk4jerry

strategy("Grid Bot Backtesting", overlay=false, pyramiding=3000, close_entries_rule="ANY", default_qty_type=strategy.cash, initial_capital=100.0, currency="USD", commission_type=strategy.commission.percent, commission_value=0.025)- 1