Chiến lược phá vỡ mô hình cờ

Tổng quan

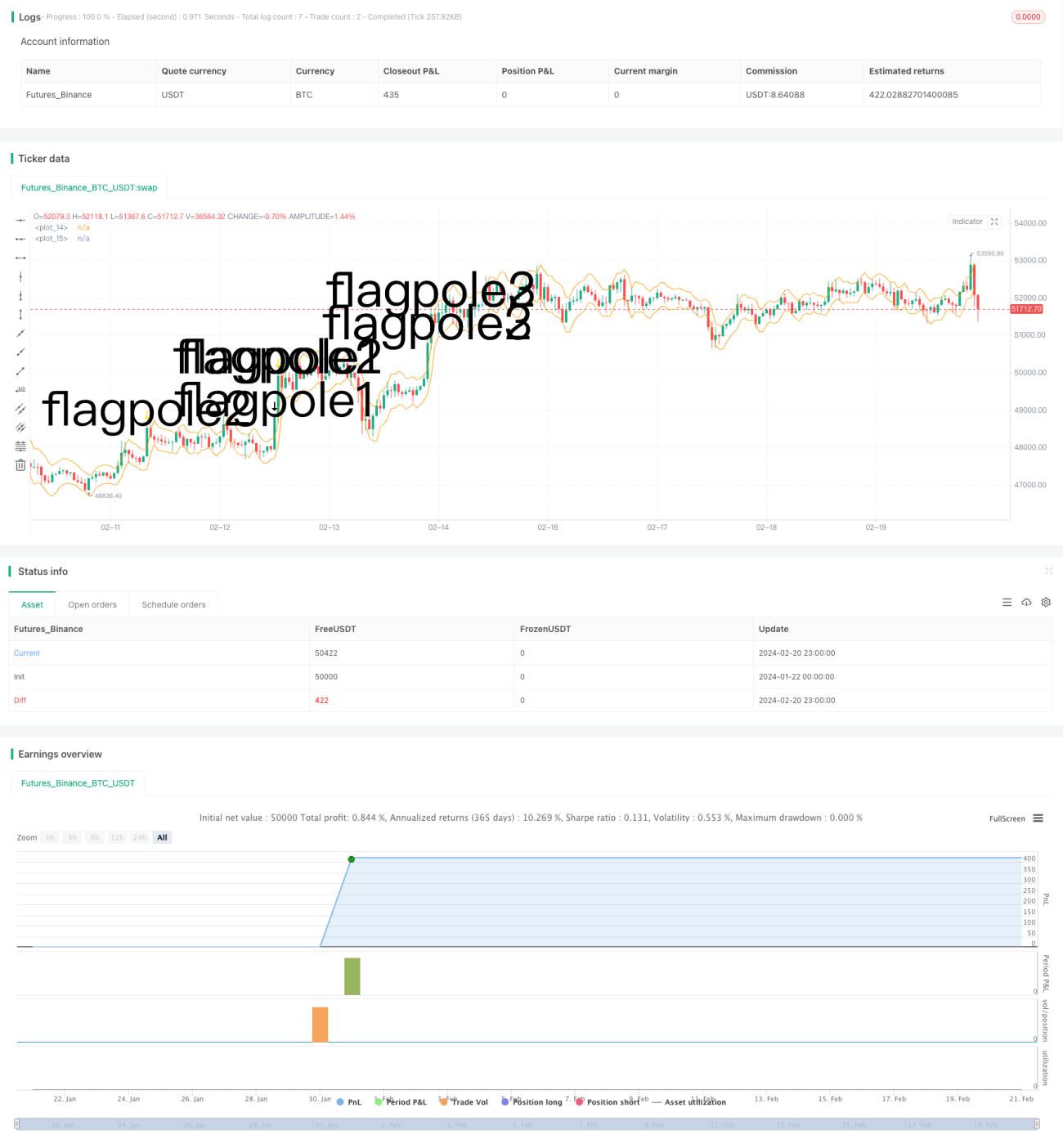

Chiến lược đột phá mô hình cờ là một chiến lược phân tích kỹ thuật, nó nhận diện mô hình hình cờ và vào lệnh tại điểm đột phá, mục tiêu là bắt đầu xu hướng. Chiến lược này sử dụng chỉ báo Dải biến động trung bình thực (ATR) để hỗ trợ phán đoán, sau khi xác định rõ cột cờ sẽ xác định phạm vi cờ, từ đó sàng lọc cơ hội vào lệnh.

Nguyên lý chiến lược

Chiến lược này chủ yếu được chia thành các bước sau:

- Xác định cột cờ: Cần thỏa mãn giá tạo đỉnh mới và phá vỡ kênh ATR.

- Xác định chiều cao cột cờ: Đo khoảng cách từ đỉnh cột cờ đến SMA trước đó.

- Xác định phạm vi cờ: Đáy cờ là 33% chiều cao cột cờ, làm phạm vi tối thiểu của cờ.

- Xác định mô hình cờ: Kiểm tra xem 3 nến trước đó có nằm hoàn toàn trong phạm vi cờ hay không.

- Vào lệnh: Khi xuất hiện mô hình cờ, mua lên.

- Thoát lệnh: Nắm giữ cố định 6 nến rồi thanh lý toàn bộ.

Khi xác định cột cờ và cờ, chiến lược khéo léo sử dụng chỉ báo ATR để phán đoán sự đột phá rõ ràng, đồng thời giới hạn nghiêm ngặt chiều cao cờ trong vòng 33% chiều cao cột cờ, tránh quá nhiều tín hiệu giả. Ngoài ra, việc xác định 3 nến liên tiếp tạo thành cờ có độ tin cậy cao hơn. Nhìn chung, chiến lược này có quy tắc thiết kế chặt chẽ, có lợi thế nhất định trong việc bắt các đột phá giai đoạn đầu của xu hướng.

Phân tích ưu điểm

Chiến lược này có những ưu điểm chính sau:

- Sử dụng cấu trúc mô hình cờ để xác định bắt đầu xu hướng, đây là phương pháp kinh điển trong phân tích kỹ thuật, tỷ lệ thành công cao.

- Chỉ báo ATR và giới hạn phạm vi nghiêm ngặt có thể tránh được nhiều tín hiệu giả, tăng độ chính xác khi vào lệnh.

- Thoát lệnh cố định sau 6 nến có thể khóa một phần lợi nhuận, tránh rủi ro đảo chiều xu hướng.

- Các quy tắc chiến lược rõ ràng, dễ thực hiện, dễ nắm bắt và tuân thủ.

- Có thể tìm kiếm cơ hội trong nhiều loại thị trường, tính linh hoạt tốt.

Phân tích rủi ro

Các rủi ro chính của chiến lược này bao gồm:

- Mô hình cờ không thể phán đoán hoàn toàn xu hướng, cũng có trường hợp thất bại.

- Thoát lệnh sau 6 nến quá cứng nhắc, có thể rời khỏi thị trường quá sớm.

- Khi thị trường biến động quá mức, dễ tạo ra mô hình cờ giả.

- Không thể kiểm soát hiệu quả khoản lỗ trên mỗi giao dịch.

Đối với các rủi ro trên, chúng ta có thể thiết lập chiến lược cắt lỗ, hoặc tối ưu hóa cơ chế thoát lệnh, chốt lời kịp thời khi lợi nhuận đạt đến một tỷ lệ nhất định. Ngoài ra, chúng ta cũng có thể kết hợp với các chỉ báo khác để lọc, tránh tín hiệu giả khi thị trường biến động quá mức.

Hướng tối ưu hóa

Chiến lược này có thể được tối ưu hóa theo các hướng sau:

- Kết hợp với các chỉ báo như MACD, KD, v.v., để tránh tín hiệu giả trong thị trường biến động.

- Tham số hóa bội số ATR, chu kỳ thoát lệnh, v.v., theo loại thị trường, giúp chiến lược thích ứng hơn.

- Thiết lập cắt lỗ di động hoặc xem xét tỷ lệ lợi nhuận/rủi ro để thoát lệnh linh hoạt.

- Thử nghiệm phương pháp học máy để tìm đặc điểm chính xác hơn trong việc xác định chiều cao cờ.

- Đánh giá tỷ lệ thắng thực tế và tỷ lệ lợi nhuận/rủi ro, điều chỉnh quy mô vị thế một cách linh hoạt.

Tổng kết

Nhìn chung, chiến lược đột phá mô hình cờ sử dụng mô hình kỹ thuật để phán đoán bắt đầu xu hướng, đây là một phương pháp kinh điển, chiến lược này có thiết kế quy tắc vào lệnh chặt chẽ, có thể lọc nhiều tín hiệu giả. Tuy nhiên, kiểm soát rủi ro và cơ chế thoát lệnh vẫn còn dư địa để tối ưu, chúng ta có thể xem xét từ góc độ tổng thể, giúp chiến lược hoạt động ổn định trên nhiều thị trường khác nhau. Nếu được xác nhận và tối ưu hóa đầy đủ, chiến lược này có thể trở thành một thành phần có giá trị trong hệ thống giao dịch định lượng.

/*backtest

start: 2024-01-22 00:00:00

end: 2024-02-21 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// © smith26

//This strategy enters on a bull flag and closes position 6 bars later. Average true range is used instead of a moving average.

//The reason for ATR instead of MA is because with volatile securities, the flagpole must stand up a noticable "distance" above the trading range---which you can't determine with a MA alone.

//This is broken up into multiple parts: Defining a flagpole, defining the pole height, and defining the flag, which will be constrained to the top third (33%) of the pole height to be considered a flag.- 1