দ্বৈত চলমান গড় ক্রসওভার তীর কৌশল

সারসংক্ষেপ

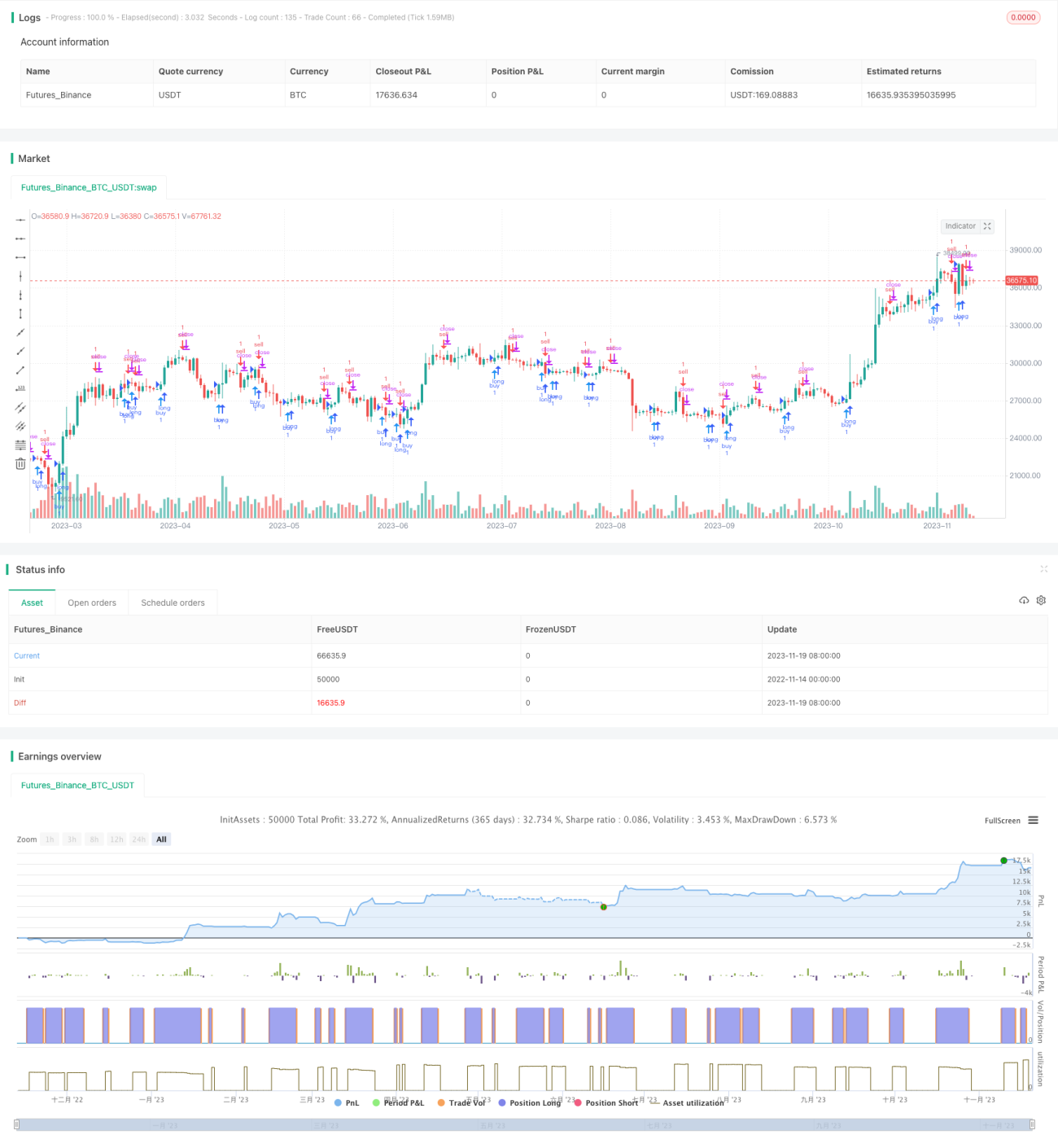

এই কৌশলটি MACD সূচকের দ্বৈত মুভিং এভারেজ ক্রসওভার গণনা করে ক্রয় ও বিক্রয়ের সময় নির্ধারণ করে। এটি চার্টে তীর চিহ্ন এঁকে ট্রেডিং সিগন্যাল প্রদর্শন করে।

নীতি

কৌশলটি প্রথমে ফাস্ট লাইন (EMA 12 পিরিয়ড), স্লো লাইন (EMA 26 পিরিয়ড) এবং MACD পার্থক্য গণনা করে। তারপর ফাস্ট ও স্লো লাইনের গোল্ডেন ক্রস ও ডেথ ক্রস এবং MACD পার্থক্যের ধনাত্মক/ঋণাত্মক মানের ভিত্তিতে ক্রয় ও বিক্রয়ের সময় নির্ধারণ করে:

- যখন ফাস্ট লাইন স্লো লাইনকে উপরে অতিক্রম করে (গোল্ডেন ক্রস) এবং MACD পার্থক্য ০-কে উপরে অতিক্রম করে, তখন এটি ক্রয় সংকেত।

- যখন ফাস্ট লাইন স্লো লাইনকে নিচে অতিক্রম করে (ডেথ ক্রস) এবং MACD পার্থক্য ০-কে নিচে অতিক্রম করে, তখন এটি বিক্রয় সংকেত।

মিথ্যা সংকেত ফিল্টার করতে, কোডে পূর্ববর্তী K-লাইনের সংকেত অবস্থাও বিবেচনা করা হয়। শুধুমাত্র যখন পূর্ববর্তী K-লাইনটি বিপরীত সংকেত দেখায় (ক্রয় থেকে বিক্রয় বা বিক্রয় থেকে ক্রয়), তখন বর্তমান সংকেতটি সক্রিয় হয়।

এছাড়াও, কোডে K-লাইনের উপর তীর চিহ্ন এঁকে ক্রয় ও বিক্রয়ের সময় নির্দেশ করা হয়।

সুবিধা

এই কৌশলটির নিম্নলিখিত সুবিধা রয়েছে:

- দ্বৈত মুভিং এভারেজ ক্রসওভার ব্যবহার করে বাজারের শব্দ ফিল্টার করে এবং প্রবণতা চিহ্নিত করতে সহায়তা করে।

- MACD পার্থক্য যুক্ত করে ভুল অর্ডার ও ভুল সিদ্ধান্ত এড়ানো যায়।

- তীর চিহ্নের মাধ্যমে ক্রয়-বিক্রয়ের সময় নির্দেশ করে, যা কার্যক্রমকে আরও স্পষ্ট করে।

- নিয়মগুলি সহজ ও পরিষ্কার, বোঝা ও কপি করা সহজ।

ঝুঁকি ও সমাধান

এই কৌশলটির কিছু ঝুঁকিও রয়েছে:

- দ্বৈত মুভিং এভারেজ ক্রসওভার মিথ্যা সংকেত তৈরি করতে পারে, যা অতিরিক্ত ট্রেডিংয়ের কারণ হতে পারে। প্যারামিটারগুলি যথাযথভাবে সামঞ্জস্য করে বা অতিরিক্ত ফিল্টার যুক্ত করে মিথ্যা সংকেত কমানো যেতে পারে।

- প্রবণতার মধ্যে ওঠানামা সনাক্ত করতে অক্ষমতা থাকায় লোকসান হতে পারে। ADX-এর মতো প্রবণতা সূচক যুক্ত করে এই পরিস্থিতি এড়ানো যেতে পারে।

- স্থির ক্রয়-বিক্রয় শর্ত কৌশলটিকে যান্ত্রিক করে তোলে এবং বাজার পরিবর্তনের সাথে খাপ খাওয়াতে পারে না। মেশিন লার্নিংয়ের মতো অভিযোজিত পদ্ধতি ব্যবহার করে অপ্টিমাইজ করা যেতে পারে।

অপ্টিমাইজেশনের দিকনির্দেশনা

এই কৌশলটি নিম্নলিখিত দিক থেকে অপ্টিমাইজ করা যেতে পারে:

- বিভিন্ন প্যারামিটার কম্বিনেশন পরীক্ষা করে সর্বোত্তম ফাস্ট লাইন, স্লো লাইন এবং MACD প্যারামিটার খুঁজে বের করা।

- ভলিউম ব্রেকআউটের মতো অতিরিক্ত এন্ট্রি শর্ত যুক্ত করে সংকেত ফিল্টার করা।

- স্টপ-লস ব্যবস্থা যুক্ত করে পৃথক লেনদেনের লোকসান নিয়ন্ত্রণ করা।

- VIX-এর মতো অস্থিরতা সূচক যুক্ত করে ঝুঁকি পছন্দ নির্ধারণ করা।

- স্থির নিয়মের পরিবর্তে মেশিন লার্নিং মডেল ব্যবহার করে কৌশলটির অভিযোজিত অপ্টিমাইজেশন প্রয়োগ করা।

উপসংহার

এই দ্বৈত মুভিং এভারেজ ক্রসওভার তীর কৌশলটি সামগ্রিকভাবে সহজ ও কার্যকর। দ্বৈত মুভিং এভারেজ ক্রসওভার ও MACD পার্থক্য ফিল্টার ব্যবহার করে মাঝারি থেকে দীর্ঘমেয়াদী প্রবণতায় ক্রয়-বিক্রয় পয়েন্ট সনাক্ত করা যায় এবং দামের মোড় এড়িয়ে চলা যায়। তীর চিহ্নের মাধ্যমে ইঙ্গিত দেওয়াও কার্যক্রমকে আরও স্পষ্ট করে। পরবর্তীতে প্যারামিটার অপ্টিমাইজেশন, অতিরিক্ত ফিল্টার যুক্ত করার মাধ্যমে কৌশলটির স্থায়িত্ব ও লাভজনকতা আরও বাড়ানো যেতে পারে।

/*backtest

start: 2022-11-14 00:00:00

end: 2023-11-20 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=3

//Daniels stolen code

strategy(shorttitle="Daniels Stolen Code", title="Daniels Stolen Code", overlay=true, calc_on_order_fills=true, pyramiding=0)

- 1