Bidirektionale Handelsstrategie mit multiplen gleitenden Durchschnittslücken

Überblick

Diese Strategie nutzt den Williams High/Low-Indikator, um Long/Short-Umkehrsignale zu identifizieren, kombiniert mit mehreren gleitenden Durchschnitten für Gap-Trading und filtert mit dem RSI-Indikator falsche Signale, um effizienten bidirektionalen Handel zu ermöglichen.

Strategieprinzip

-

Der Williams High/Low-Indikator nutzt die Höchst- und Tiefstkurse innerhalb eines bestimmten Zeitraums, um Wendepunkte zu erkennen und Kauf- und Verkaufssignale zu generieren.

-

Die gleitenden Durchschnitte von 20, 50 und 100 Tagen bilden mehrere gleitende Durchschnitte. Wenn der Preis zwei dieser Durchschnitte durchbricht, wird ein Handelssignal ausgelöst.

-

Der RSI-Indikator identifiziert überkaufte und überverkaufte Zonen, um unsichere Signale zu filtern.

-

Die Strategie erzeugt stabile Kauf- und Verkaufssignale, indem sie bestimmt, welche zwei gleitenden Durchschnitte der Preis durchbricht, kombiniert mit dem Williams-Indikator-Signal und der RSI-Filterung.

-

Einstiegsentscheidung: Wenn der kurzfristige gleitende Durchschnitt von unten nach oben den mittel- und langfristigen gleitenden Durchschnitt durchbricht und gleichzeitig ein Williams-Tief und ein RSI-Tiefsignal auftreten, wird long gegangen; wenn der kurzfristige gleitende Durchschnitt von oben nach unten den mittel- und langfristigen gleitenden Durchschnitt durchbricht und gleichzeitig ein Williams-Hoch und ein RSI-Hochsignal auftreten, wird short gegangen.

-

Stop-Loss und Take-Profit: Es werden feste prozentuale Stop-Loss und Take-Profit gesetzt.

Strategievorteile

-

Der Williams-Indikator kann wichtige Unterstützungs- und Widerstandsniveaus genau bestimmen und Umkehrsignale erkennen.

-

Die Beurteilung des Durchbruchs mehrerer gleitender Durchschnitte vermeidet Fehlsignale durch Oszillationen eines einzelnen gleitenden Durchschnitts.

-

Der RSI-Indikator hilft, falsche Signale zu filtern, was den Einstiegszeitpunkt präziser und zuverlässiger macht.

-

Das feste Stop-Loss/Take-Profit-System kontrolliert das Risiko und macht Gewinne und Verluste klarer.

-

Die Kombination aus Umkehrindikator und Trendindikator mit doppelter Bestätigung macht die Handelssignale genauer und zuverlässiger.

Strategierisiken

-

Ungeeignete Auswahl der Handelsinstrumente, Parameter müssen für verschiedene Instrumente angepasst werden.

-

Unangemessene Zeitrahmenwahl, Parameter müssen an verschiedene Zeitrahmen angepasst werden.

-

Feste Stop-Loss/Take-Profit können nicht an Marktveränderungen angepasst werden, was zu vorzeitigen Stopps oder unzureichendem Gewinnmitnahmen führen kann.

-

Bei Oszillationen der gleitenden Durchschnitte können leicht Fehlsignale entstehen.

-

Bei Divergenz der Indikatoren kommt es zu Verzögerungen bei den Signalen.

Optimierungsrichtungen der Strategie

-

Dynamische Optimierung der Parameter entsprechend verschiedenen Handelsinstrumenten.

-

Einbindung eines automatisch anpassenden Stop-Loss/Take-Profit-Systems, um Gewinne/Verluste angemessener zu gestalten.

-

Hinzufügen weiterer Indikatorfilter wie MACD, Stochastic usw., um Fehlsignale zu reduzieren.

-

Hinzufügen von Machine-Learning-Algorithmen zur automatischen Erkennung optimaler Handelszeitpunkte.

-

Kombination mit weiteren Trendindikatoren zur Erkennung von Trendmärkten.

Zusammenfassung

Diese Strategie nutzt umfassend mehrere technische Analysetools wie den Williams-Indikator, gleitende Durchschnitte und den RSI-Indikator. Durch doppelte Bestätigung werden Fehlsignale reduziert, Umkehrmöglichkeiten effektiv erfasst und mit festen Stop-Loss/Take-Profit das Risiko kontrolliert. Insgesamt handelt es sich um eine zuverlässige und praktische bidirektionale Handelsstrategie. Im nächsten Schritt wird die Strategie durch Parameteroptimierung, Optimierung von Take-Profit/Stop-Loss und Modellintegration weiter verbessert.

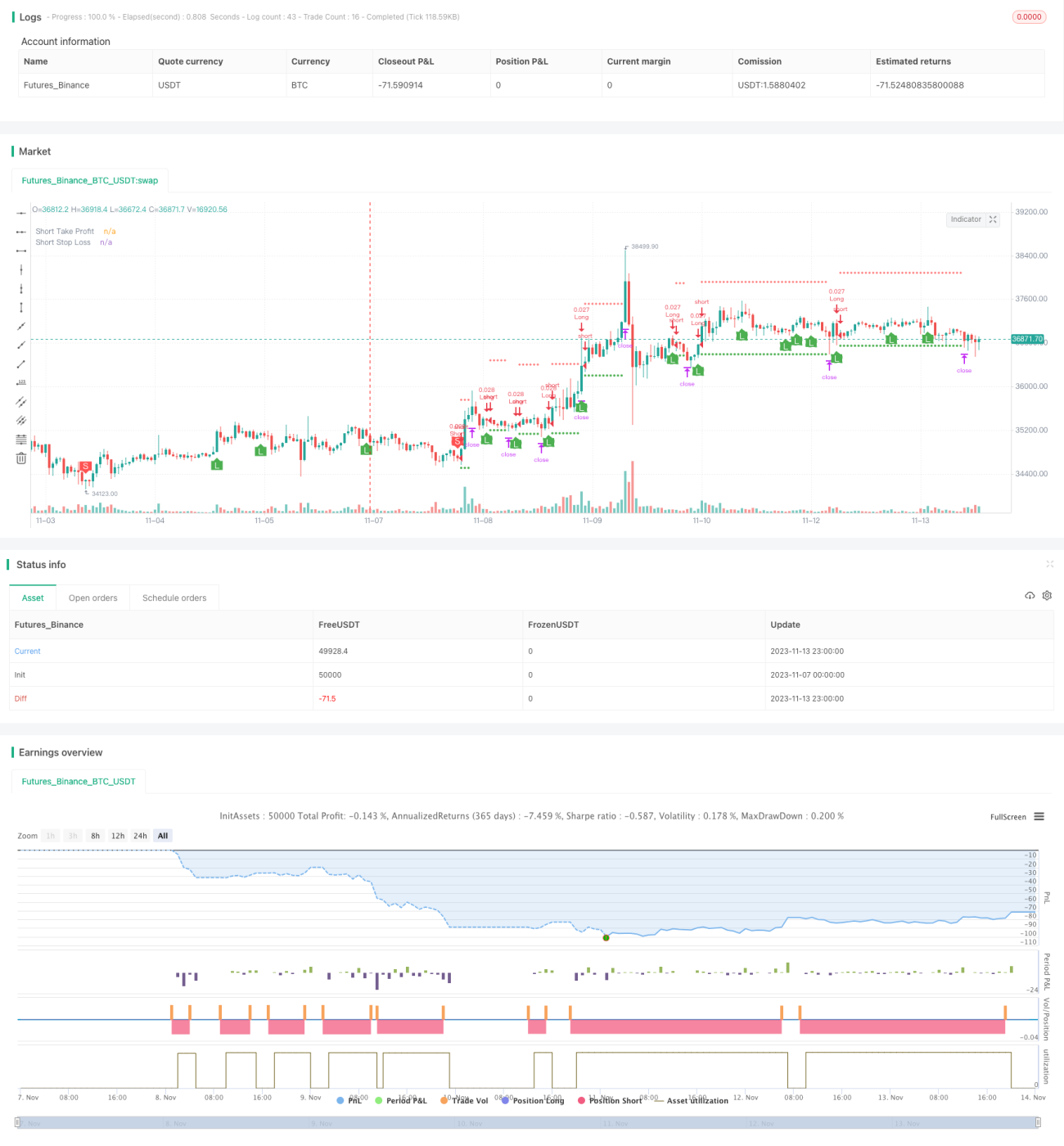

/*backtest

start: 2023-11-07 00:00:00

end: 2023-11-14 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © B_L_A_C_K_S_C_O_R_P_I_O_N

// v 1.1

- 1