Zwei-MA-Kreuz-Pfeil-Strategie

Überblick

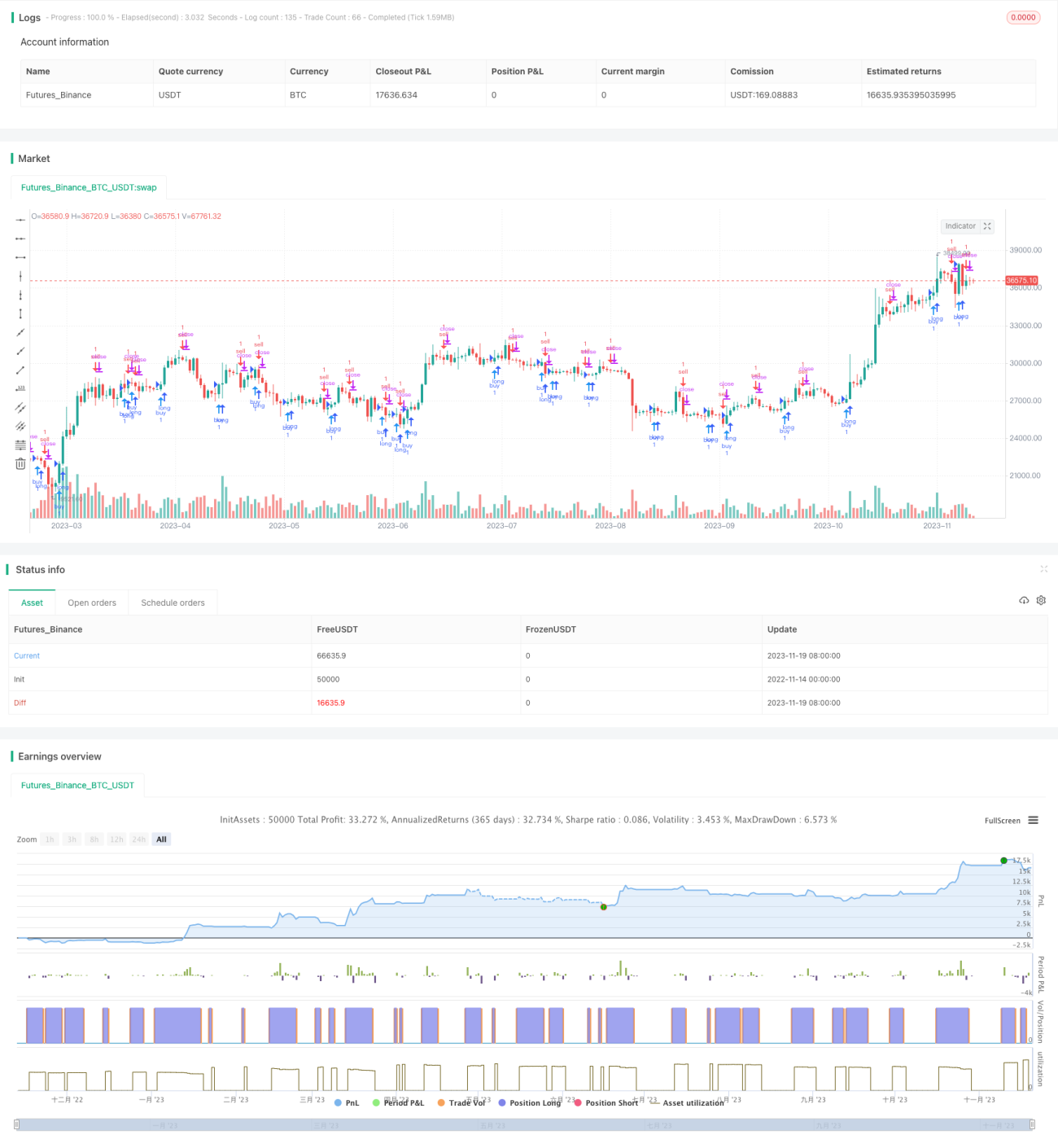

Diese Strategie identifiziert Kauf- und Verkaufssignale durch die Berechnung des MACD-Indikators und den Crossover zweier gleitender Durchschnitte. Auf dem Chart werden Pfeile eingezeichnet, um die Handelssignale anzuzeigen.

Funktionsweise

Die Strategie berechnet zunächst die schnelle Linie (EMA 12 Perioden), die langsame Linie (EMA 26 Perioden) und die MACD-Differenz. Anschließend werden Kauf- und Verkaufssignale basierend auf dem Golden Cross und Death Cross der schnellen und langsamen Linie sowie dem Vorzeichen der MACD-Differenz ermittelt:

- Kaufsignal: Wenn die schnelle Linie die langsame Linie von unten nach oben kreuzt (Golden Cross) und die MACD-Differenz die Nulllinie von unten nach oben durchbricht.

- Verkaufssignal: Wenn die schnelle Linie die langsame Linie von oben nach unten kreuzt (Death Cross) und die MACD-Differenz die Nulllinie von oben nach unten durchbricht.

Um Fehlsignale zu filtern, wird im Code auch der Signalstatus der vorherigen Kerze berücksichtigt. Das aktuelle Signal wird nur ausgelöst, wenn das vorherige Signal das Gegenteil war (z. B. von Kauf zu Verkauf oder umgekehrt).

Zusätzlich werden Pfeile auf den Kerzen eingezeichnet, um Kauf- und Verkaufszeitpunkte anzuzeigen.

Vorteile

Die Strategie bietet folgende Vorteile:

- Durch die Verwendung des Crossovers zweier gleitender Durchschnitte können Marktstörungen effektiv gefiltert und Trends erkannt werden.

- Die Einbeziehung der MACD-Differenz vermeidet Fehlausführungen und Fehlinterpretationen.

- Die Pfeilmarkierungen für Kauf- und Verkaufszeitpunkte machen die Handelssignale klarer.

- Die Regeln sind einfach, klar und leicht zu verstehen und nachzuvollziehen.

Risiken und Lösungen

Die Strategie birgt auch einige Risiken:

- Der Crossover zweier gleitender Durchschnitte kann Fehlsignale erzeugen und zu übermäßigem Handel führen. Durch Anpassung der Parameter der gleitenden Durchschnitte oder Hinzufügen weiterer Filterbedingungen kann die Anzahl der Fehlsignale reduziert werden.

- In Seitwärtsphasen eines Trends können Verluste auftreten. Die Kombination mit Trendindikatoren wie ADX kann dies vermeiden.

- Die festgelegten Kauf- und Verkaufsbedingungen machen die Strategie mechanisch und unflexibel gegenüber Marktveränderungen. Adaptive Optimierungen wie maschinelles Lernen könnten Abhilfe schaffen.

Optimierungsmöglichkeiten

Die Strategie kann in folgenden Bereichen optimiert werden:

- Testen verschiedener Parameterkombinationen, um die besten Werte für schnelle, langsame Linie und MACD zu finden.

- Hinzufügen weiterer Einstiegsbedingungen, z. B. eines Handelsvolumenausbruchs, um Signale zu filtern.

- Integration eines Stop-Loss-Mechanismus zur Begrenzung einzelner Verluste.

- Berücksichtigung von Volatilitätsindikatoren wie VIX zur Risikoeinschätzung.

- Einsatz von Modellen des maschinellen Lernens anstelle fester Regeln, um eine adaptive Optimierung der Strategie zu erreichen.

Zusammenfassung

Diese Doppel-Gleitender-Durchschnitt-Crossover-Pfeil-Strategie ist insgesamt einfach und praktisch. Durch den Crossover zweier gleitender Durchschnitte und die Filterung über die MACD-Differenz können Kauf- und Verkaufspunkte in mittel- bis langfristigen Trends identifiziert werden, ohne Wendepunkte zu verpassen. Die Pfeile machen die Handelssignale noch klarer. Durch Parameteroptimierung, das Hinzufügen von Filtern und andere Maßnahmen kann die Stabilität und Rentabilität der Strategie weiter verbessert werden.

/*backtest

start: 2022-11-14 00:00:00

end: 2023-11-20 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=3

//Daniels stolen code

strategy(shorttitle="Daniels Stolen Code", title="Daniels Stolen Code", overlay=true, calc_on_order_fills=true, pyramiding=0)

- 1