Eine auf TFO und ATR basierende Trendfolge-Trailing-Stop-Strategie

Übersicht

Diese Strategie basiert auf dem Trend-Flex-Oszillator (TFO) von Dr. John Ehlers und dem Average True Range (ATR)-Indikator und ist eine Trendfolge-Stopp-Strategie. Sie eignet sich für bullische Märkte und eröffnet Long-Positionen, wenn der Kurs nach einer überverkauften Phase umkehrt. In der Regel werden Positionen innerhalb weniger Tage geschlossen, es sei denn, der Markt wird bärisch erwischt – in diesem Fall wird die Position gehalten. Die Strategie erlaubt die Anpassung konfigurierbarer Parameter durch einfache Backtests, jedoch sollten Backtest-Ergebnisse nicht blind vertraut werden.

Funktionsweise

Die Strategie kombiniert TFO und ATR: Sie eröffnet Long-Positionen, wenn die Kaufbedingungen erfüllt sind, und schließt sie bei Verkaufssignalen.

Kaufbedingung:

Wenn der TFO unter einem bestimmten Schwellenwert liegt (überverkauft), der TFO-Wert des vorherigen Candlesticks niedriger ist als der aktuelle (Umkehr nach oben), und gleichzeitig der ATR über einem festgelegten Volatilitäts-Schwellenwert liegt (steigende Marktvolatilität), wird eine Long-Position eröffnet.

Verkaufsbedingung:

Wenn der TFO über einem bestimmten Schwellenwert liegt (überkauft) und der ATR über dem Volatilitäts-Schwellenwert liegt, werden alle Long-Positionen geschlossen. Zusätzlich verfügt die Strategie über einen Trailing-Stop: Unterschreitet der Kurs den festgelegten Trailing-Stop-Kurs, werden ebenfalls alle Long-Positionen geschlossen. Der Nutzer kann wählen, ob die Strategie auf Basis der Indikatorsignale oder nur auf Basis des Stopp-Kurses schließen soll.

Die Strategie kann maximal 15 Long-Positionen gleichzeitig halten. Ihre Parameter sind anpassbar und für verschiedene Zeitrahmen geeignet.

Vorteile der Strategie

-

Kombination von Trend- und Volatilitätsbewertung für stabile Marktrichtung: TFO erkennt frühe Signale von Trendausbrüchen, ATR erfasst zunehmende Marktvolatilität.

-

Flexibel einstellbare Kauf-/Verkaufsparameter und Stopp-Parameter: Der Nutzer kann Parameter an den Markt anpassen, um eine Optimierung zu erreichen.

-

Integrierte Stopp-Funktion reduziert Verluste bei extremen Marktbewegungen: Stop-Strategien sind ein wichtiger Bestandteil des quantitativen Handels.

-

Unterstützt Nachkauf- und Teilverkaufsmodi, um durch größere Positionen Gewinne zu verstärken – geeignet für bullische Märkte.

Risiken der Strategie

-

Die Strategie geht nur Long, nicht Short, und kann daher in fallenden Märkten keine Gewinne erzielen. Bei heftigen Bärenmärkten können massive Verluste entstehen.

-

Falsche Parametereinstellungen können zu übermäßigem Handel oder Fehlkäufen/-verkäufen führen. Es ist eine wiederholte Optimierung erforderlich, um die beste Parameterkombination zu finden.

-

In extremen Marktphasen kann der Stopp wirkungslos sein und große Verluste nicht verhindern – ein Problem, das alle Stopp-Strategien betrifft.

-

Backtests spiegeln nicht vollständig den Echtzeithandel wider; die Ergebnisse im Live-Handel können abweichen.

Optimierungsmöglichkeiten

-

Ein Moving-Stop-Loss könnte in die Verkaufsbedingungen integriert werden, um rechtzeitig zu stoppen und das Abwärtsrisiko effektiv zu kontrollieren.

-

Eine Short-Mechanik könnte hinzugefügt werden: Wenn der TFO nach unten dreht und der ATR ausreichend groß ist, Short-Positionen eröffnen – damit wäre die Strategie auch für Bärenmärkte geeignet.

-

Weitere Filter könnten integriert werden, z. B. Volumenänderungen, um den Einfluss anomaler Marktbewegungen zu reduzieren.

-

Parameter und Backtest-Ergebnisse für verschiedene Zeitrahmen könnten getestet werden, um den optimalen Zeitrahmen und die beste Parameterkombination zu finden.

Zusammenfassung

Die Strategie vereint die Vorteile von Trendanalyse und Volatilitätsüberwachung, indem sie mit TFO und ATR die Marktrichtung bestimmt. Sie umfasst Mechanismen wie Nachkauf, Teilverkauf und Trailing-Stop, um Gewinne zu maximieren und Risiken zu kontrollieren – ideal für bullische Märkte. Es gibt zudem erweiterbare Optimierungsmöglichkeiten durch zusätzliche Indikatorenfilter und Parameter-Tuning, um die Performance weiter zu verbessern. Grundsätzlich erfüllt die Strategie die Kernanforderungen einer quantitativen Handelsstrategie und ist eine vertiefte Untersuchung und Anwendung wert.

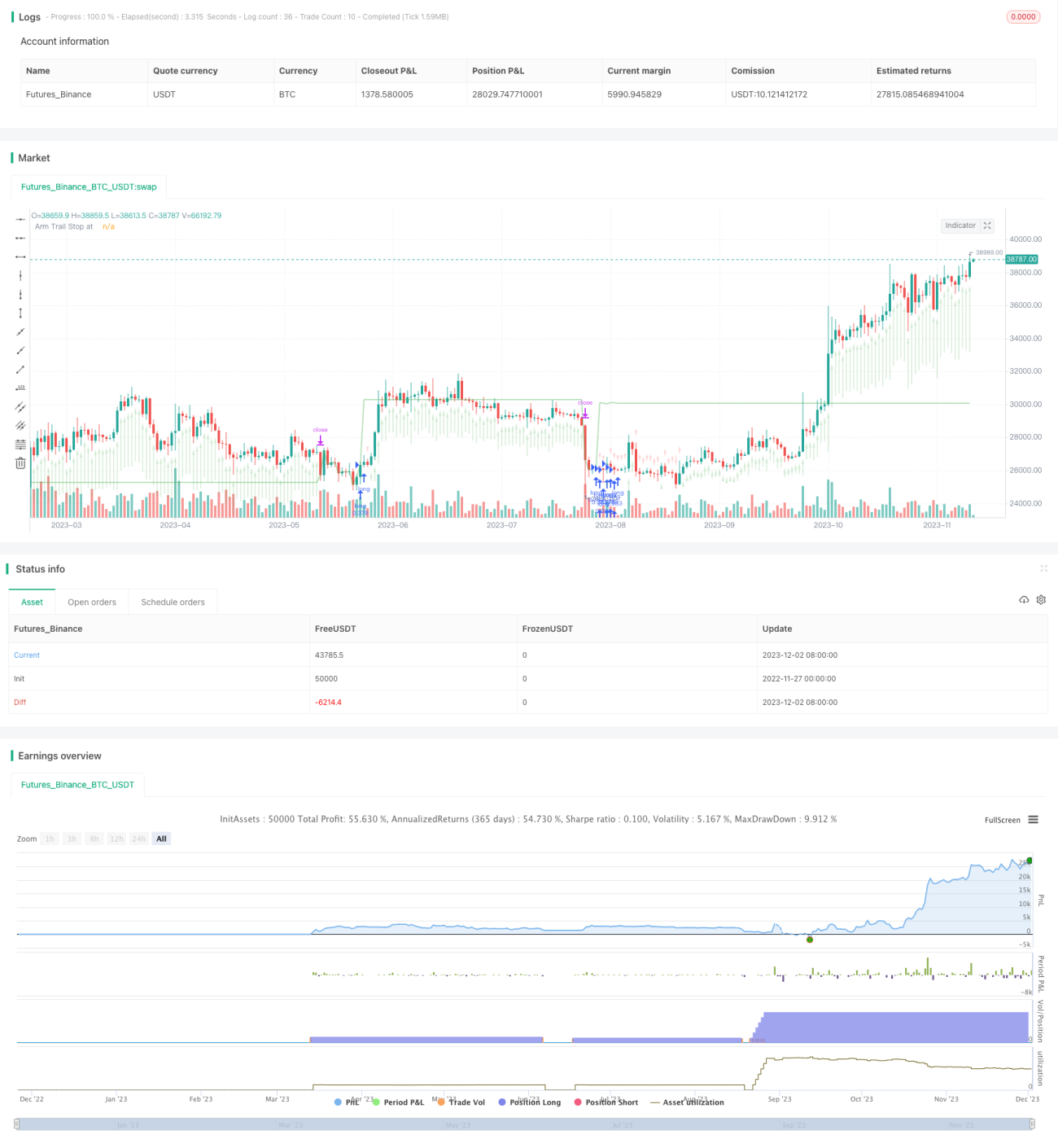

/*backtest

start: 2022-11-27 00:00:00

end: 2023-12-03 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © Chart0bserver

//

// Open Source attributions:- 1