Adaptive Volatilitätshandelsstrategie basierend auf Preisausbrüchen

Überblick

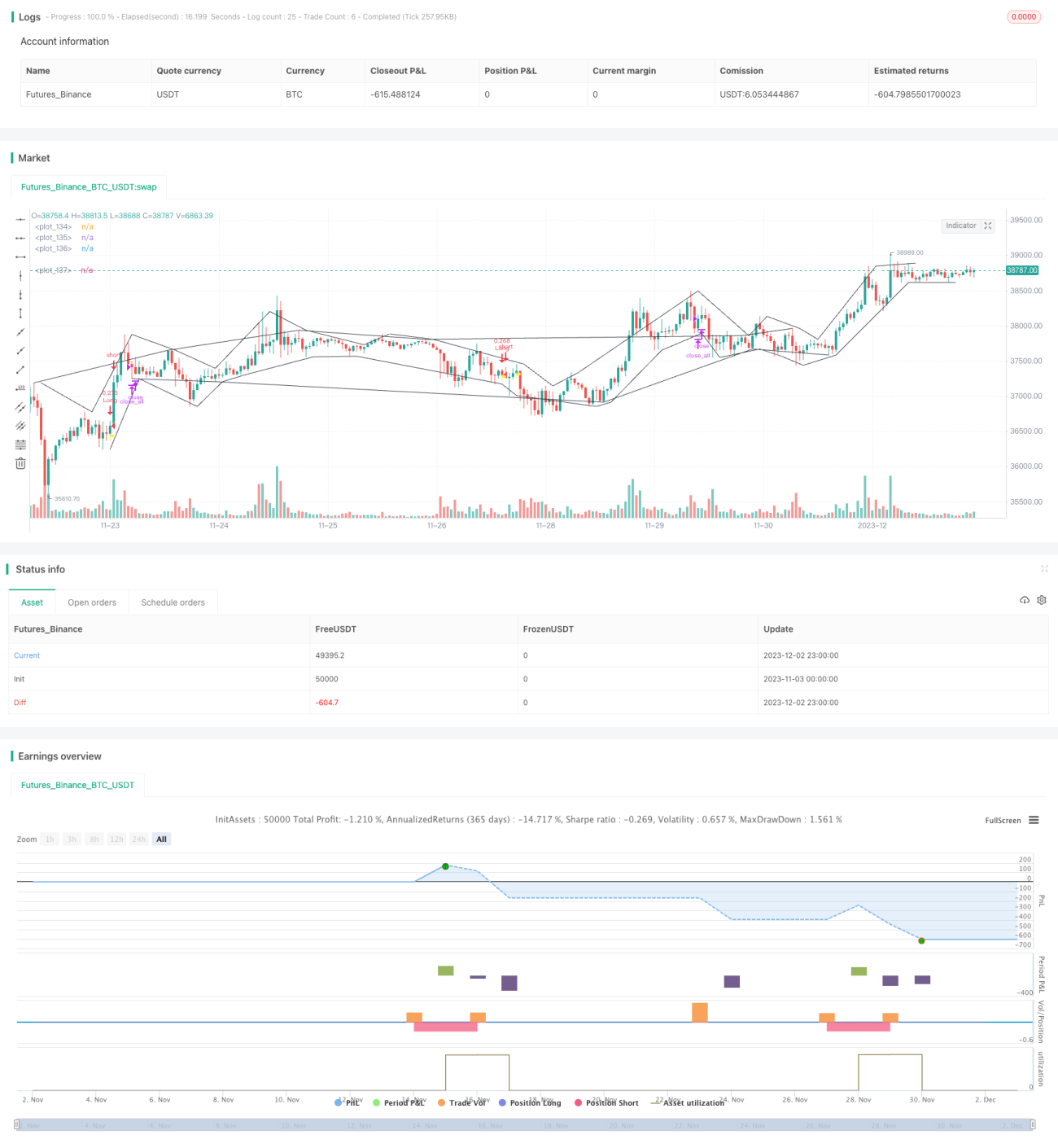

Diese Strategie identifiziert mithilfe von Preisausbruchspunkten Markttrends und kombiniert adaptive Indikatoren zur Beurteilung des übergeordneten Trends, um kurzfristige Preisumkehrmöglichkeiten zu erfassen. Wenn der Preis aus einem Referenzausbruchskanal ausbricht, werden Kauf-/Verkaufssignale generiert. Die Strategie eignet sich für den Handel mit hochvolatilen Kryptowährungen.

Strategieprinzip

- Identifizierung von Preisextrempunkten als Kanalgrenzen. Wenn der Preis ein neues Hoch oder Tief erreicht, wird dieser Punkt als Kanalgrenze festgelegt.

- Berechnung des adaptiven Volatilitätsindikators MA zur Bestimmung der allgemeinen Trendrichtung. Ein höherer MA-Wert deutet auf eine aktuelle Seitwärtsphase hin.

- Ein Kaufsignal wird generiert, wenn der Preis die obere Kanalgrenze nach oben durchbricht; ein Verkaufssignal entsteht, wenn der Preis die untere Kanalgrenze nach unten durchbricht.

- Festlegung eines Stop-Loss. Der Stop-Loss für Long-Positionen wird auf 1 % des Einstiegspreises gesetzt.

Vorteilsanalyse

- Der Preiskanal ist adaptiv und kann Trendwenden präzise erkennen.

- Der Volatilitätsindikator beurteilt den übergeordneten Trend und vermeidet das Verpassen der Hauptrichtung in Seitwärtsbewegungen.

- Reversal-Strategie, geeignet zum Erfassen kurzfristiger Preiserholungen.

Risikoanalyse

- Bei stark anhaltenden Abwärtsbewegungen können mehrere Stop-Loss ausgelöst werden, was zu erheblichen Verlusten führt.

- In Seitwärtsphasen erhöhen häufige Kauf-/Verkaufssignale die Transaktionskosten.

- Der manuelle Einstiegszeitpunkt ist erforderlich; eine vollautomatische Handel birgt das Risiko von Überanpassung.

Optimierungsrichtungen

- Optimierung der MA-Parameter, um den Gesamttrend besser zu beurteilen.

- Hinzufügen von Volumenindikatoren, um Reversalsignale bei nachlassendem Volumen zu vermeiden.

- Integration von Machine-Learning-Modellen zur dynamischen Optimierung der Parameter.

Zusammenfassung

Die Strategie hat eine klare Grundidee und einen gewissen praktischen Wert. Dennoch muss das Handelsrisiko kontrolliert werden, um in bestimmten Marktphasen große Verluste zu vermeiden. Zukünftige Optimierungen können in den Bereichen Gesamtrahmen, Indikatorparameter und Risikomanagement erfolgen, um die Strategieparameter und Handelssignale zuverlässiger zu gestalten.

/*backtest

start: 2023-11-03 00:00:00

end: 2023-12-03 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// @version = 4

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © TradingGroundhog

- 1