Multi-Faktor-RSI-Reversal-Strategie

Übersicht

Diese Strategie nutzt den RSI-Indikator, um überkaufte und überverkaufte Zustände zu identifizieren, und kombiniert dabei mehrere Hilfsfaktoren wie MACD und Stochastic für den Einstieg. Die Strategie zielt darauf ab, kurzfristige Umkehrchancen zu erfassen und gehört zu den Reversal-Strategien.

Funktionsweise der Strategie

Die Strategie verwendet hauptsächlich den RSI-Indikator, um zu beurteilen, ob sich der Markt in einem überkauften oder überverkauften Zustand befindet. Wenn der RSI-Indikator die eingestellte überkaufte Linie überschreitet, deutet dies auf einen möglicherweise überkauften Markt hin, und die Strategie entscheidet sich für eine Short-Position. Wenn der RSI-Indikator unter die eingestellte überverkaufte Linie fällt, deutet dies auf einen möglicherweise überverkauften Markt hin, und die Strategie entscheidet sich für eine Long-Position. So werden kurzfristige Handelsmöglichkeiten genutzt, die beim Übergang des Kurses von einem extremen Zustand zum anderen entstehen.

Darüber hinaus werden mehrere Hilfsfaktoren wie MACD und Stochastic integriert. Diese Hilfsfaktoren dienen dazu, mögliche falsch-positive Handelssignale herauszufiltern. Erst wenn der RSI-Indikator ein Signal gibt und die Hilfsfaktoren dieses Signal unterstützen, führt die Strategie einen tatsächlichen Trade aus. Diese Multi-Faktor-Kombination verbessert die Zuverlässigkeit der Signale und damit die Stabilität der Strategie.

Analyse der Vorteile

Der größte Vorteil dieser Strategie liegt in der hohen Erfassungseffizienz und der Verbesserung der Signalqualität durch Multi-Faktor-Verifizierung. Im Einzelnen zeigt sich dies in folgenden Aspekten:

- Der RSI-Indikator selbst hat eine starke Fähigkeit, Marktregime zu erkennen, und kann überkaufte/überverkaufte Phänomene effektiv identifizieren.

- Durch die Nutzung mehrerer Hilfsinstrumente zur Multi-Faktor-Überprüfung wird die Signalqualität verbessert und eine große Anzahl falsch-positiver Signale ausgefiltert.

- Die Strategie ist unempfindlich gegenüber Parametern und leicht optimierbar.

Risiken und Lösungen

Die Strategie birgt auch gewisse Risiken, die sich hauptsächlich auf zwei Aspekte konzentrieren:

- Risiko des gescheiterten Reversals. Reversal-Signale basieren von Natur aus auf statistischen Arbitragemöglichkeiten, und die Wahrscheinlichkeit einzelner fehlgeschlagener Reversals kann nicht ausgeschlossen werden. Das Risiko kann durch Reduzierung der Positionsgröße oder Setzen von Stop-Losses kontrolliert werden.

- Verlustrisiko in bullischen Märkten. Die Strategie handelt insgesamt immer noch gegen den Trend, sodass sie in bullischen Märkten unweigerlich gewisse Verluste erleiden kann. Dies erfordert eine genaue Einschätzung des übergeordneten Trends und gegebenenfalls manuelle Eingriffe, um ungünstige Marktphasen zu überspringen.

Optimierungsmöglichkeiten

Die Strategie sollte in den folgenden Bereichen optimiert werden:

- Test verschiedener Instrumente und Suche nach optimalen Parameterkombinationen. Obwohl die Strategie unempfindlich gegenüber Parametern ist, wird dennoch empfohlen, für verschiedene Instrumente die optimalen Parameter zu ermitteln.

- Hinzufügen eines adaptiven Ausstiegsmechanismus. Es kann getestet werden, ob dynamische Stop-Losses oder zeitbasierte Ausstiege die Strategie besser an Marktveränderungen anpassen.

- Integration von maschinellen Lernalgorithmen. Es kann versucht werden, das Modell die Wahrscheinlichkeit eines erfolgreichen Reversals lernen zu lassen, um die Gewinnquote der Strategie zu erhöhen.

Zusammenfassung

Insgesamt handelt es sich bei dieser Strategie um eine kurzfristige Reversal-Strategie. Sie nutzt die Fähigkeit des RSI-Indikators, überkaufte und überverkaufte Zustände zu erkennen, und kombiniert mehrere Hilfsinstrumente zur Multi-Faktor-Verifizierung, wodurch die Signalqualität verbessert wird. Die Strategie hat eine hohe Erfassungseffizienz und eine gute Stabilität. Sie ist es wert, weiter getestet und optimiert zu werden, um letztendlich profitable Ergebnisse zu erzielen.

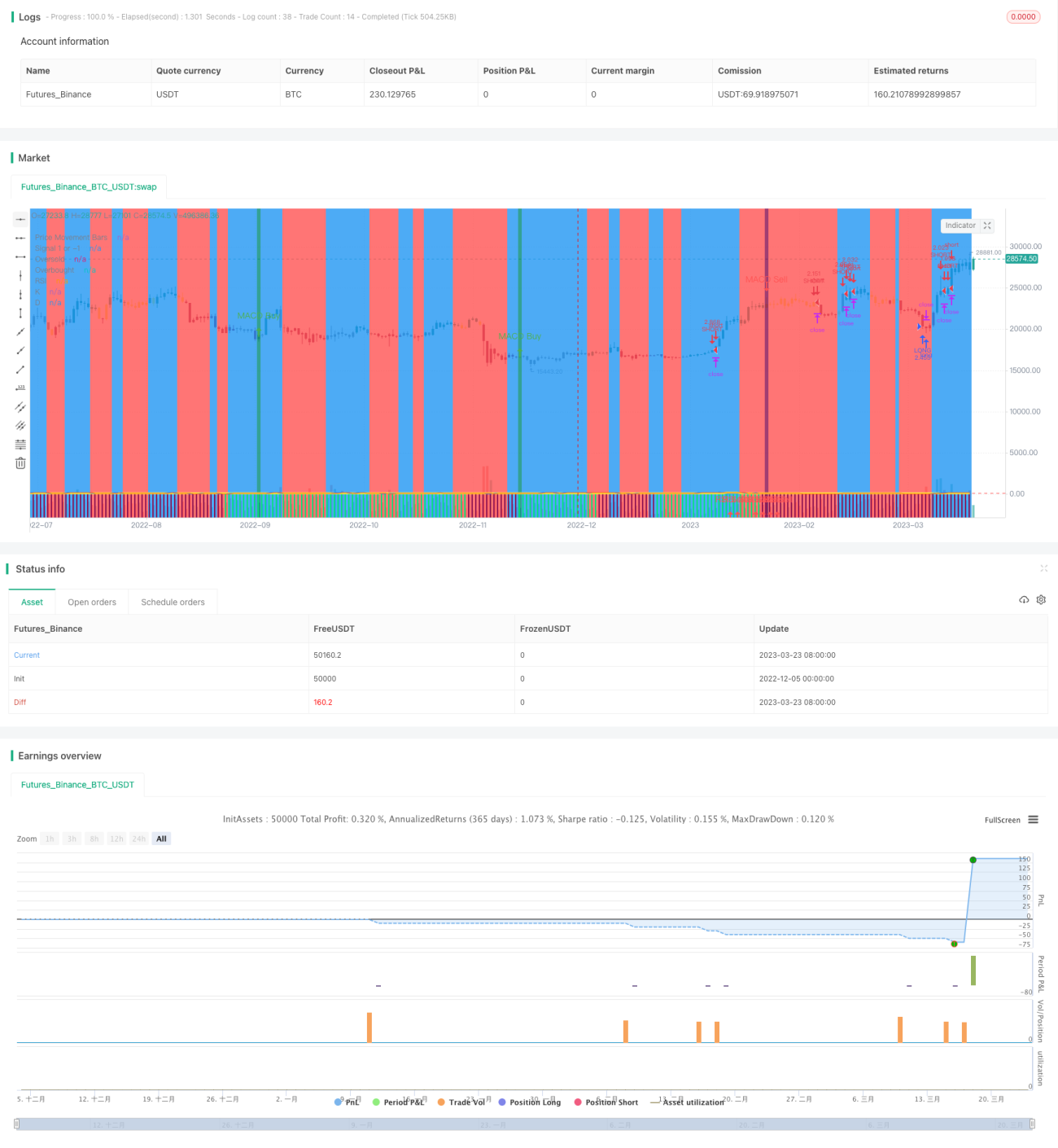

/*backtest

start: 2022-12-05 00:00:00

end: 2023-03-24 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

//@version=4

strategy(shorttitle='Ain1',title='All in One Strategy', overlay=true, initial_capital = 1000, process_orders_on_close=true, default_qty_type = strategy.percent_of_equity, default_qty_value = 100, commission_type=strategy.commission.percent, commission_value=0.18, calc_on_every_tick=true)- 1