Quantitative Strategie basierend auf der Preisänderungsrate und gleitenden Mittelwerten

Übersicht

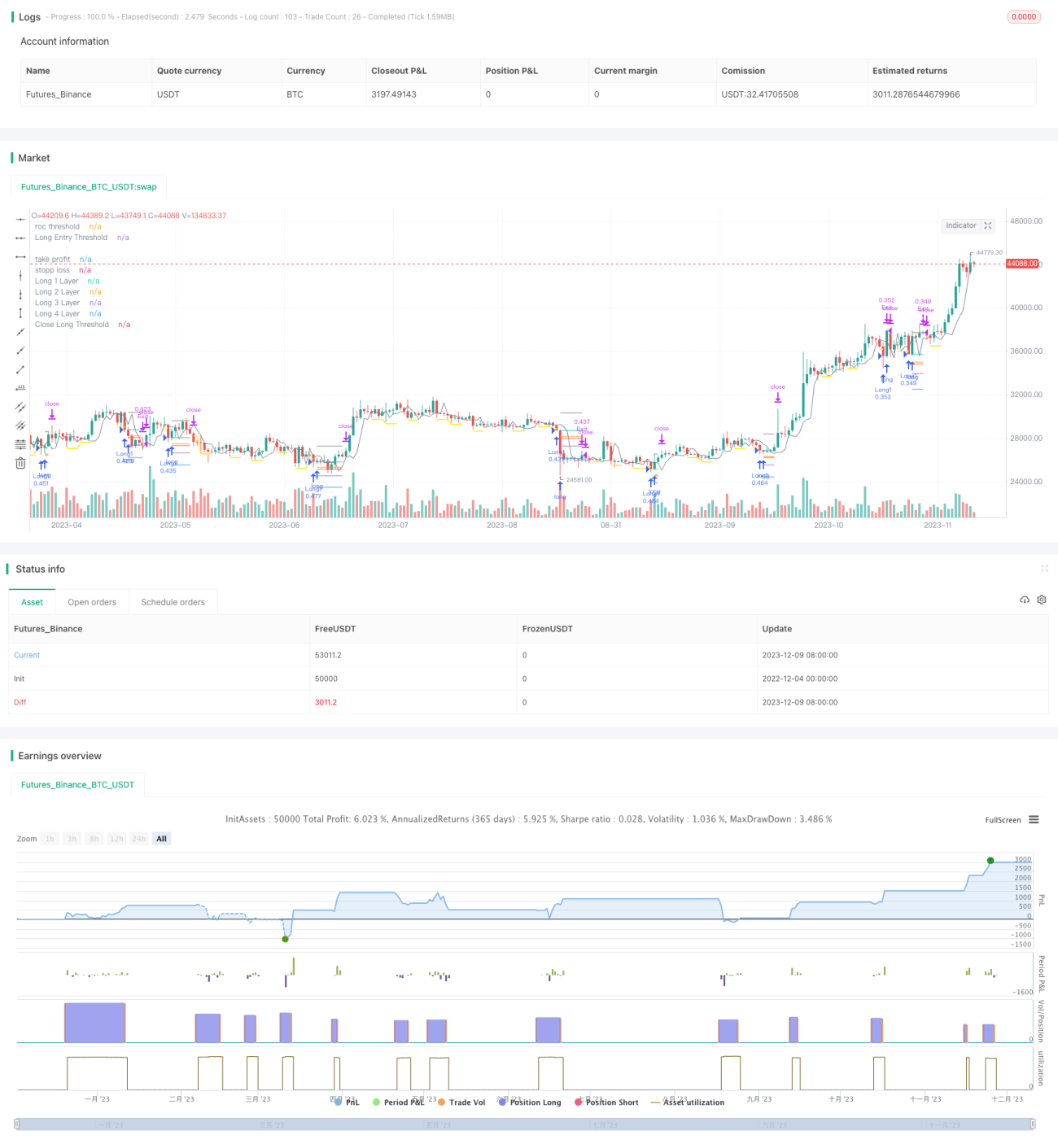

Diese Strategie kombiniert die technischen Indikatoren der Preisänderungsrate und des gleitenden Durchschnitts, um Ein- und Ausstiegspunkte präzise zu bestimmen. Wenn der Preis deutlich fällt, wird eine Kauf-Schwelle festgelegt, und bei weiterem Fall wird eine Long-Position eröffnet; wenn der Preis steigt, wird eine Verkaufs-Schwelle festgelegt, und bei weiterem Anstieg wird die Position geschlossen. Gleichzeitig wird eine Nachkauf-Methode angewendet, um in mehreren Schritten zu kaufen und die Kosten zu senken.

Strategieprinzip

Kauf-Logik

- Berechnung der Preisänderungsrate (ROC) und Festlegung einer Kauf-Schwellenlinie.

- Wenn der Preis die Kauf-Schwellenlinie nach unten durchbricht, wird dieser Punkt notiert und eine Kauf-Begrenzungslinie aktiviert.

- Die Kauf-Begrenzungslinie hat eine über Parameter festgelegte Dauer und wird nach Ablauf deaktiviert.

- Wenn der Preis weiter fällt und die Kauf-Begrenzungslinie nach unten durchbricht, wird die erste Long-Position eröffnet.

Verkaufs-Logik

- Berechnung der Preisänderungsrate (ROC) und Festlegung einer Verkaufs-Schwellenlinie.

- Wenn der Preis die Verkaufs-Schwellenlinie nach oben durchbricht, wird dieser Punkt notiert und eine Verkaufs-Begrenzungslinie aktiviert.

- Die Verkaufs-Begrenzungslinie hat eine über Parameter festgelegte Dauer und wird nach Ablauf deaktiviert.

- Wenn der Preis weiter steigt und die Verkaufs-Begrenzungslinie nach oben durchbricht, werden alle Long-Positionen geschlossen.

Risikomanagement

Die Strategie verfügt über integrierte Stop-Loss und Take-Profit Funktionen, deren Parameter individuell eingestellt werden können, um das Risiko offener Positionen in Echtzeit zu kontrollieren.

Nachkauf-Methode

Bei jeder Eröffnung einer Handels-Position wird der nachfolgende Kaufpreis basierend auf Eingabeparametern in einem bestimmten Verhältnis festgelegt, um einen schrittweisen Nachkauf (Durchschnittskosteneffekt) zu erreichen.

Vorteile

- Verwendung des ROC-Indikators zur präzisen Bestimmung von Kauf- und Verkaufspunkten; ROC reagiert sehr empfindlich auf Preisänderungen und ermöglicht genaue Ein- und Ausstiege.

- Die Begrenzungslinie bestätigt den Handelszeitpunkt weiter und vermeidet Fehlsignale (falsche Ausbrüche).

- Die Nachkauf-Methode ermöglicht es, dem Marktwert zu folgen, während das Risiko kontrollierbar bleibt.

- Integrierte Stop-Loss und Take-Profit kontrollieren streng das Risiko einzelner Positionen.

Risiken und Lösungen

- Bei starken Marktschwankungen kann die Strategie zu viele Positionen eröffnen. Lösung: Angemessene Parameter für den Nachkauf setzen und die Gesamtzahl der Positionen begrenzen.

- In Seitwärtsbewegungen mit unklarem Trend können Stop-Loss oder Take-Profit häufig ausgelöst werden. Lösung: Stop-Loss/Take-Profit-Abstände großzügiger wählen oder die Funktion deaktivieren.

Optimierungsvorschläge

- Kombination mit anderen Indikatoren zur Filterung von Einstiegssignalen, z.B. nur ROC-Signale verwenden, wenn der Preis unter dem gleitenden Durchschnitt liegt.

- Optimierung der Nachkauf-Logik: Nachkauf nur unter bestimmten Bedingungen starten, z.B. nur wenn der Preis um mehr als einen bestimmten Betrag weiter fällt.

- Parametereinstellungen variieren stark je nach Instrument; umfangreiches Backtesting und Papierhandel sind notwendig, um die optimale Parameterkombination zu finden.

- Adaptive Stop-Loss/Take-Profit: Unterschiedliche Stop-Abstände je nach Marktvolatilität.

Zusammenfassung

Diese Strategie nutzt den ROC-Indikator zur präzisen Bestimmung von Ein- und Ausstiegspunkten, filtert Signale mit Begrenzungslinien, integriert Stop-Loss/Take-Profit zur Risikokontrolle und erweitert Gewinne durch Nachkäufe. Bei angemessener Parametereinstellung kann sie überdurchschnittliche Renditen erzielen, während das Risiko kontrollierbar bleibt. Zukünftige Optimierungen der Signalfilter und des Risikomanagements können die Strategie an weitere Marktbedingungen anpassen.

- 1