Doppelte Umkehr-Trendfolgestrategie

Übersicht

Dies ist eine Trendfolgestrategie, die zwei gegenläufige Signale kombiniert. Sie integriert die 123-Umkehrstrategie und die Performance-Index-Strategie, um Preisumkehrpunkte zu verfolgen und eine zuverlässigere Trendbestimmung zu erreichen.

Strategieprinzip

Die Strategie besteht aus zwei Unterstrategien:

-

123-Umkehrstrategie

Verwendet 14-Tage-Kerzen, um Umkehrsignale zu erkennen. Die spezifischen Regeln sind:

- Long-Signal: Die Schlusskurse der letzten beiden Tage fallen, der aktuelle Kerzenschlusskurs liegt über dem Schlusskurs des vorherigen Tages, der 9-Tage-Stochastic-Slow liegt unter 50.

- Short-Signal: Die Schlusskurse der letzten beiden Tage steigen, der aktuelle Kerzenschlusskurs liegt unter dem Schlusskurs des vorherigen Tages, der 9-Tage-Stochastic-Fast liegt über 50.

-

Performance-Index-Strategie

Berechnet die prozentuale Veränderung der letzten 14 Tage als Indikator. Die Regeln lauten:

- Performance-Index > 0 → Long-Signal

- Performance-Index < 0 → Short-Signal

Das endgültige Signal ist die Kombination beider Signale. Es sind gleichgerichtete Long-/Short-Signale erforderlich, um tatsächliche Kauf-/Verkaufsoperationen auszulösen.

Dadurch können Rauschen teilweise gefiltert und die Signale zuverlässiger gemacht werden.

Strategievorteile

Dieses duale Umkehrsystem bietet folgende Vorteile:

- Kombination zweier Faktoren für zuverlässigere Signale

- Effektive Filterung von Marktrauschen zur Vermeidung von Fehlsignalen

- Das 123-Muster ist klassisch und praktisch, einfach zu erkennen und zu reproduzieren

- Der Performance-Index kann die zukünftige Trendrichtung abschätzen

- Flexible Parameterkombinationen, die weiter optimiert werden können

Strategierisiken

Die Strategie birgt auch einige Risiken:

- Mögliches Verpassen plötzlicher Umkehrungen, unvollständige Erfassung von Trends

- Geringere Signalhäufigkeit durch doppelte Bedingungen, was die Rentabilität beeinträchtigen kann

- Erfordert gleichgerichtete Beurteilung, anfällig für individuelle Aktienvolatilität

- Falsche Parametereinstellungen können zu Signalabweichungen führen

Mögliche Optimierungsansätze:

- Anpassung von Parametern wie Kerzenlänge, Stochastic-Perioden etc.

- Optimierung der Logik zur Beurteilung doppelter Signale

- Einbeziehung weiterer Faktoren wie Volumen

- Hinzufügen eines Stop-Loss-Mechanismus

Zusammenfassung

Die Strategie kombiniert duale Umkehrsignale und kann Preiswendepunkte effektiv erkennen. Obwohl die Signalwahrscheinlichkeit sinkt, ist die Zuverlässigkeit höher und eignet sich für mittel- bis langfristige Trends. Durch Parameteranpassungen und Multifaktor-Optimierung kann die Strategiewirkung weiter verstärkt werden.

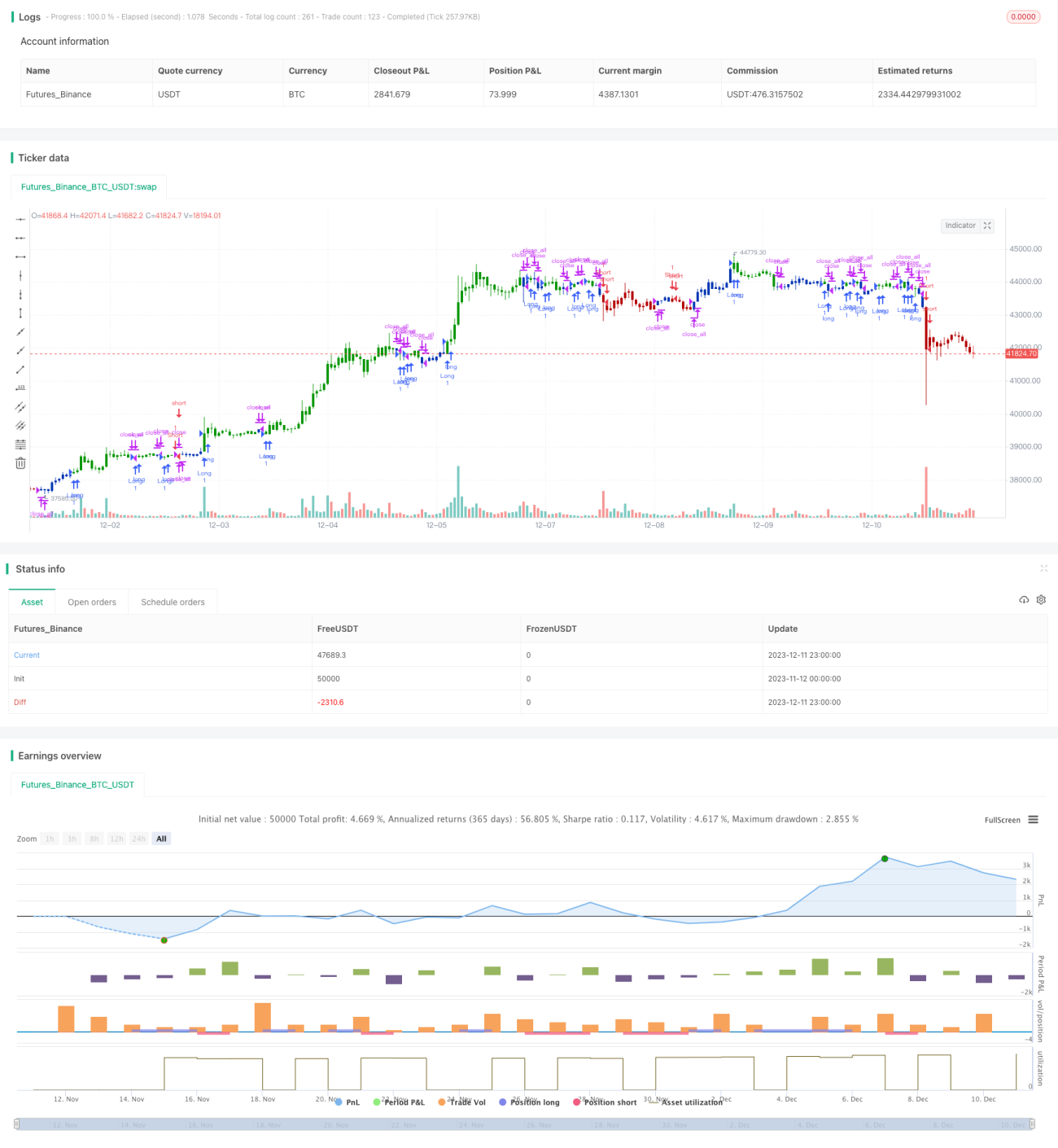

/*backtest

start: 2023-11-12 00:00:00

end: 2023-12-12 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

////////////////////////////////////////////////////////////

// Copyright by HPotter v1.0 15/04/2021

// This is combo strategies for get a cumulative signal. - 1