Handelsstrategie für Bitcoin basierend auf quantitativen Indikatoren

Überblick

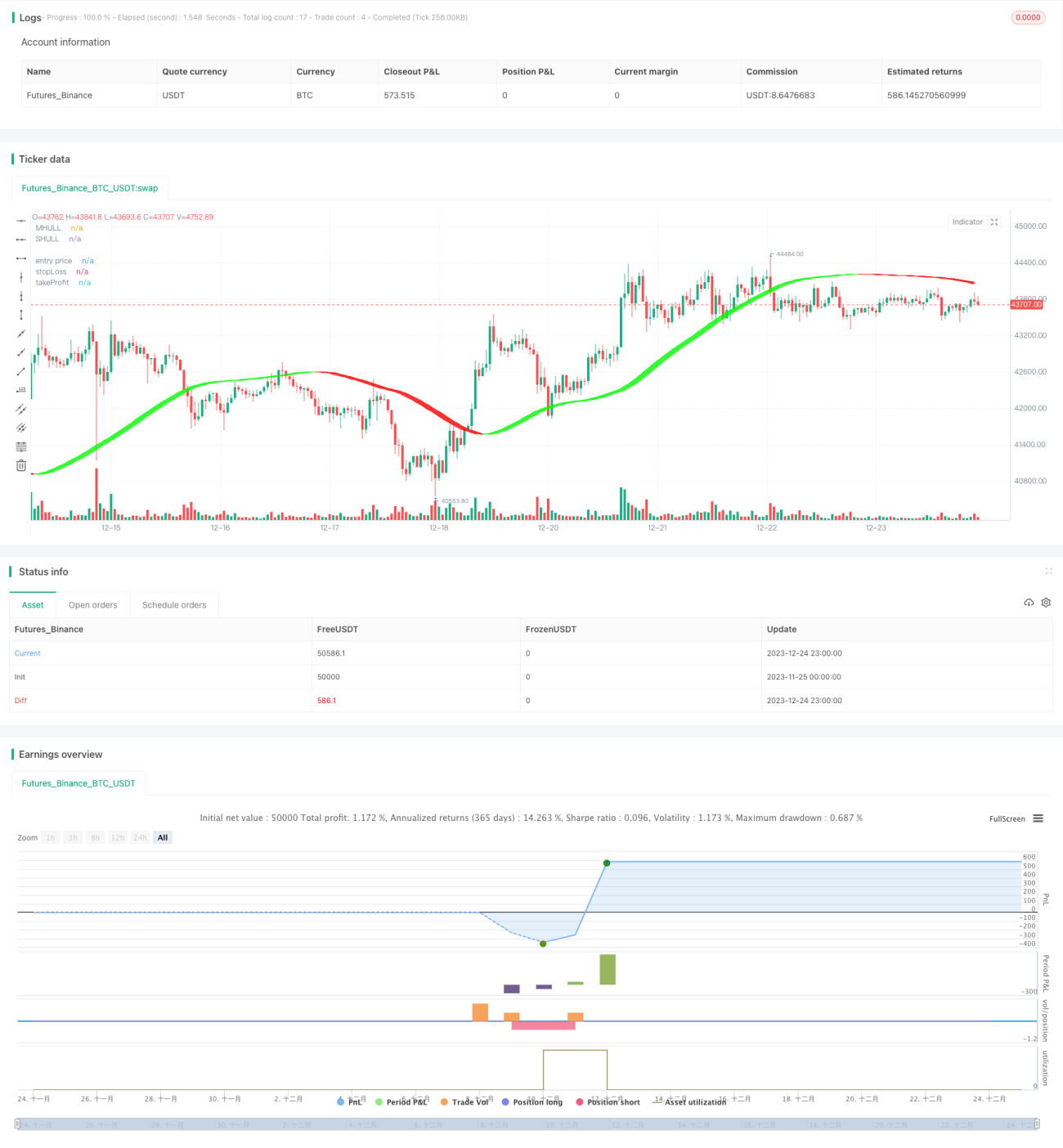

Diese Strategie verwendet mehrere quantitative Indikatoren, um Kauf- und Verkaufszeitpunkte für Bitcoin zu bestimmen und einen automatisierten Handel zu ermöglichen. Dazu gehören der Hull-Indikator (Hull), der Relative-Stärke-Index (RSI), die Bollinger-Bänder (BB) und der Volumen-Oszillator (VO).

Funktionsweise der Strategie

-

Der modifizierte gleitende Durchschnitt nach Hull wird verwendet, um den vorherrschenden Trend der Marktrichtung zu bestimmen, während die Bollinger-Bänder unterstützend zur Erkennung von Durchbruchspunkten für Käufe/Verkäufe eingesetzt werden.

-

Der RSI-Indikator wird in Kombination mit einem adaptiven Schwankungsbereich verwendet, um überkaufte und überverkaufte Zonen zu identifizieren und Handelssignale zu generieren. Gleichzeitig werden zwei Parametersätze als Duplikatsignal-Validierung eingerichtet.

-

Der Volumen-Oszillator bewertet die Kauf- und Verkaufsdynamik, um falsche Ausbrüche zu vermeiden.

-

Basierend auf den Parametern für das Verhältnis von Stop-Loss- zu Take-Profit-Kursen werden voreingestellte Stop-Loss- und Take-Profit-Niveaus festgelegt, um das Risikomanagement zu ermöglichen.

Vorteilsanalyse

-

Die Hull-Kurve kann Trendwechsel schneller erfassen, und die unterstützende Bewertung durch die Bollinger-Bänder reduziert Fehlsignale.

-

Die optimierte Parametereinstellung des RSI-Indikators und die Duplikatsignal-Validierung erhöhen die Zuverlässigkeit.

-

Der Volumen-Oszillator kombiniert mit Trend- und Indikatorsignalen vermeidet ungenaue Trades.

-

Die voreingestellte Stop-Loss- und Take-Profit-Methode kann automatisch Einzelhandelsgewinne/-verluste kontrollieren und das Gesamtrisiko effektiv steuern.

Risikoanalyse

-

Eine falsche Parametereinstellung kann zu übermäßiger Handelshäufigkeit oder einer Verschlechterung der Signalqualität führen.

-

Bei plötzlichen Ereignissen, die zu extremen Marktschwankungen führen, kann der Stop-Loss durchbrochen werden, was zu erheblichen Verlusten führt.

-

Beim Wechsel des Handelsinstruments auf eine andere Kryptowährung müssen die Parameter erneut getestet und optimiert werden.

-

Fehlen von Volumendaten, wird der Volumen-Oszillator unwirksam.

Optimierungsmöglichkeiten

-

Durchführung weiterer Kombinationstests der RSI-Parameter, um die optimalen Werte zu finden.

-

Testen der Kombination anderer Indikatoren wie MACD, KD mit dem RSI, um die Signalgenauigkeit zu verbessern.

-

Hinzufügen eines Modellvorhersagemoduls, das maschinelles Lernen zur Bestimmung der Marktrichtung nutzt.

-

Testen der Parameterwirkung beim Wechsel auf andere Handelsinstrumente.

-

Optimierung des Stop-Loss- und Take-Profit-Algorithmus, um die Gewinne zu maximieren.

Zusammenfassung

Diese Strategie integriert mehrere quantitative technische Indikatoren, um Kauf- und Verkaufszeitpunkte zu bestimmen. Durch Parameteroptimierung, Risikokontrolle und andere Methoden wird ein automatisierter Bitcoin-Handel ermöglicht. Die Ergebnisse sind recht gut, aber es sind fortlaufende Tests und Optimierungen erforderlich, um sich an Marktveränderungen anzupassen. Sie kann Anlegern als Referenz dienen und die Handelsentscheidungen unterstützen.

- 1