Trendfolgestrategie basierend auf dynamischen Unterstützungs- und Widerstandszonen

Übersicht

Diese Strategie berechnet die höchsten und niedrigsten Kurse innerhalb eines bestimmten jüngsten Zeitraums und kombiniert sie mit dem aktuellen Preis, um eine dynamische Mittellinie zu bilden. Anschließend werden basierend auf der jüngsten Volatilität ein roter Abwärtskanal und ein grüner Aufwärtskanal generiert. Diese drei Kanallinien bilden einen handelbaren Bereich. Wenn sich der Preis den Kanalgrenzen nähert, wird eine gegensätzliche Position eingenommen, mit dem Ziel, zur Mittellinie zurückzukehren und Gewinne zu erzielen. Gleichzeitig enthält die Strategie eine Trendberechnung, um Geschäfte zu filtern, die gegen den Trend laufen, und so zu verhindern, dass sie von großen Trends zerstört werden.

Strategieprinzip

- Berechnung des höchsten und niedrigsten Kurses der letzten N Perioden, kombiniert mit dem aktuellen Schlusskurs zur Bildung einer dynamischen Mittellinie

- Generierung eines dynamischen Kanalbands auf Basis des ATR und eines Multiplikators, wobei die Bandbreite mit der Marktvolatilität variiert

- Long-Position bei Abprall des Preises von der unteren Kanallinie, Short-Position bei Abprall von der oberen Kanallinie

- Logik für Take-Profit und Stop-Loss, Ziel ist die Rückkehr zur Mittellinie zur Gewinnmitnahme

- Gleichzeitige Berechnung eines Trendindex zur Filterung von Geschäften gegen den Trend

Vorteilsanalyse

- Die Position der Kanallinien ändert sich dynamisch und erfasst die Marktvolatilität in Echtzeit

- Höhere Wahrscheinlichkeit für trendkonforme Geschäfte, vorteilhaft zur Nutzung von Trends

- Stop-Loss-Logik begrenzt Verluste pro Trade

Risikoanalyse

- Falsche Parameteroptimierung kann zu übermäßigem Handel führen

- Bei starken Trends können gegentrendige Geschäfte nicht vollständig ausgefiltert werden

- Einseitiger Ausbruch aus dem Kanal kann weiterlaufen

Optimierungsmöglichkeiten

- Anpassung der Parameter der Kanallinien, um sie besser an die Eigenschaften verschiedener Instrumente anzupassen

- Anpassung der Parameter des Trendindex zur Erhöhung der Trendkonform-Wahrscheinlichkeit

- Integration von Machine-Learning-Elementen für eine dynamische Parameteroptimierung

Zusammenfassung

Diese Strategie profitiert hauptsächlich von den Schwankungseigenschaften des Marktes. Durch die dynamische Erfassung von Preisumkehrpunkten mittels des Kanals in Kombination mit der Trendfilterung können effektiv Gewinne aus Reversals erzielt werden, während das Risiko kontrolliert wird. Der Schlüssel liegt in der Parametereinstellung: Die Kanallinien müssen den Preis in Echtzeit verfolgen, aber nicht zu empfindlich sein. Gleichzeitig muss der Trendindex mit einer geeigneten Periode gewählt werden, um seine Filterfunktion zu entfalten. Die Strategie ist theoretisch trendkonform und verfügt über einen Stop-Loss; in der Praxis können durch Parameteroptimierung gute Renditen erzielt werden.

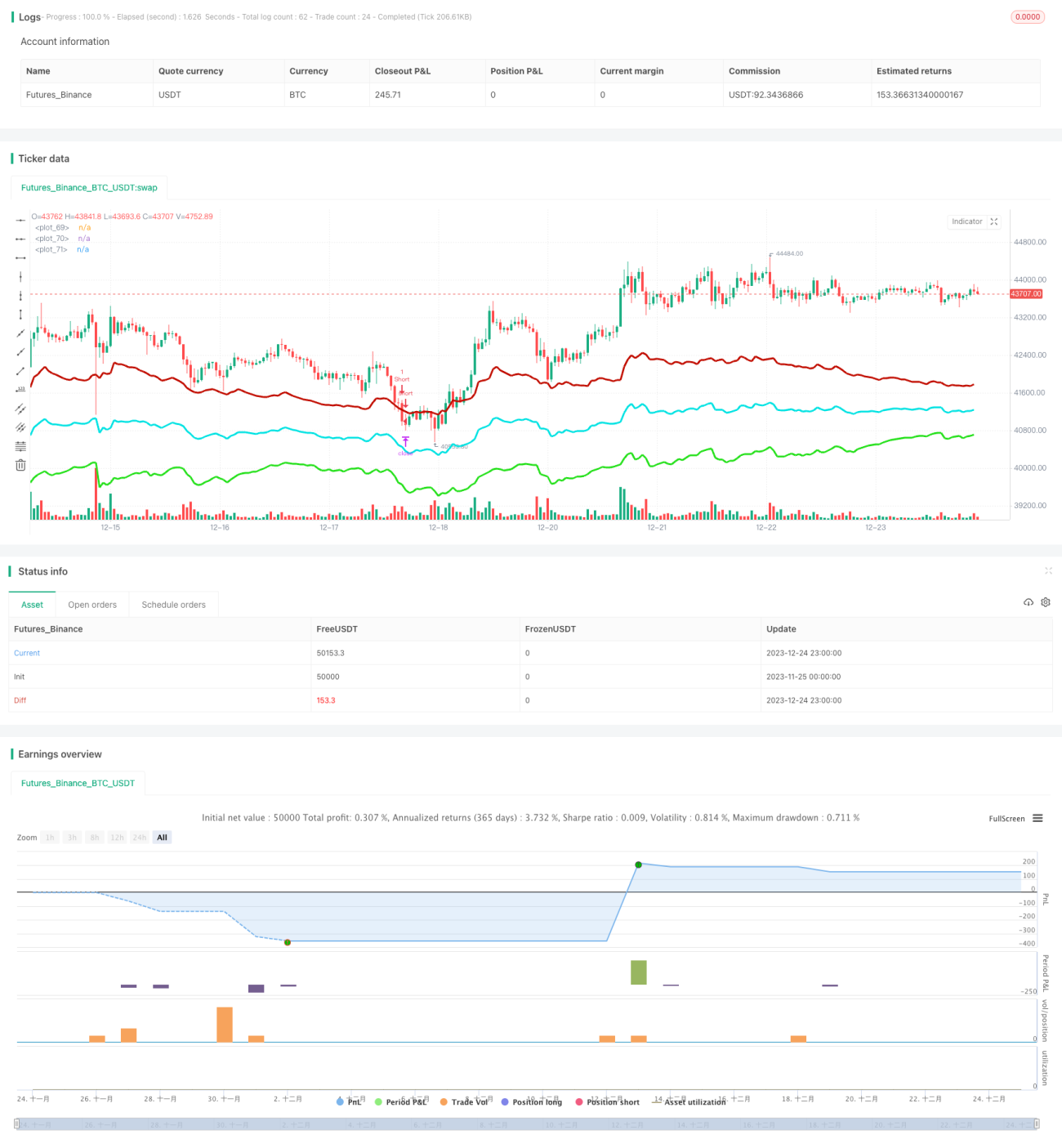

/*backtest

start: 2023-11-25 00:00:00

end: 2023-12-25 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

strategy(title="Strategy - Bobo PAPATR", overlay=true, default_qty_type = strategy.fixed, default_qty_value = 1, initial_capital = 10000)

// === STRATEGY RELATED INPUTS AND LOGIC ===- 1