Dynamische Durchschnittskosten-Sparplan- und Zinseszinstrategie

Überblick

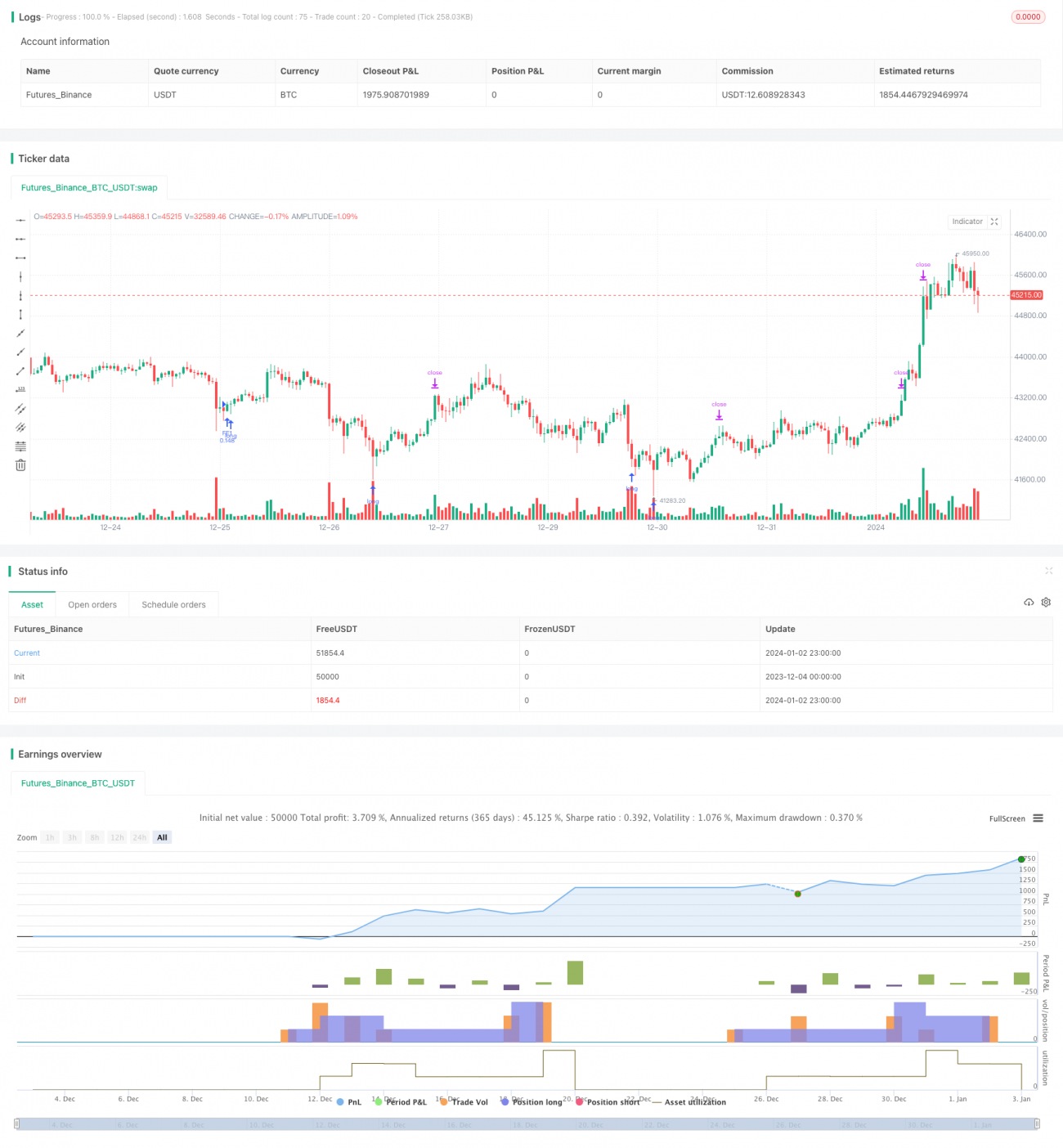

Die dynamische Durchschnittskosten-Dollar-Cost-Averaging-Strategie passt die Anzahl der Eröffnungspositionen dynamisch an. Zu Beginn eines Trends wird zunächst eine kleine Position eröffnet, und mit zunehmender Korrekturtiefe wird die Positionsgröße schrittweise erhöht. Die Strategie verwendet eine Exponentialfunktion zur Berechnung der Stop-Loss-Niveaus für jede Stufe und löst beim Erreichen dieser Niveaus eine erneute schrittweise Neueröffnung von Positionen aus, sodass die durchschnittlichen Kosten exponentiell sinken. Mit zunehmender Tiefe können die Positionskosten allmählich nach unten gedrückt werden. Sobald der Preis umkehrt, werden die Positionen gestaffelt mit Gewinn geschlossen, um höhere Renditen zu erzielen.

Strategieprinzip

Diese Strategie kombiniert einfache RSI-Überverkaufssignale mit einer gleitenden Durchschnittslinie zur Timing-Auswahl für den Einstieg. Ein erstes Kaufsignal wird ausgelöst, wenn der RSI unter die Überverkaufslinie fällt und der Schlusskurs unter dem gleitenden Durchschnitt liegt. Nach der ersten Eröffnung berechnet die Strategie auf Basis einer Exponentialfunktion die untere Grenze des Preisrückgangs, um ein DCA-Signal zu generieren. Bei jedem DCA wird die Positionsgröße so angepasst, dass jede Handelseinheit gleich groß ist. Aufgrund der dynamischen Veränderungen von Positionsgröße und -kosten entsteht ein Hebel-effekt-ähnlicher Effekt.

Mit zunehmender DCA-Anzahl sinken die durchschnittlichen Kosten kontinuierlich, sodass bereits eine geringe Erholung für einen Gewinn ausreicht. Nach mehreren aufeinanderfolgenden Eröffnungen wird eine Stop-Loss-Linie oberhalb des Durchschnittskurses eingezeichnet. Sobald der Preis diese Linie nach oben durchbricht und über den Durchschnittskurs steigt, wird die Position geschlossen.

Der größte Vorteil dieser Strategie liegt darin, dass mit sinkenden Durchschnittskosten auch in Seitwärtsmärkten schrittweise die Kosten reduziert werden können. Wenn der Trend umkehrt, sind die Durchschnittskosten bereits deutlich unter dem Marktpreis, sodass ein deutlich größerer Gewinn erzielt werden kann.

Risiken und Nachteile

Das größte Risiko der Strategie liegt in der anfänglich begrenzten Positionsgröße. In einem anhaltend fallenden Trend besteht ein Stop-Loss-Risiko. Daher sollte ein akzeptabler Stop-Loss-Bereich festgelegt werden.

Darüber hinaus gibt es auch zwei Extreme bei der Festlegung des Stop-Loss-Bereichs. Ein zu großer Stop-Loss-Bereich verhindert, dass eine ausreichend tiefe Erholung genutzt wird. Ein zu kleiner Stop-Loss-Bereich erhöht die Wahrscheinlichkeit, dass der Preis in einer mittelfristigen Korrektur wieder auf das vorherige Hoch steigt und umkehrt. Daher ist es entscheidend, je nach Markt und eigener Risikobereitschaft den passenden Stop-Loss-Bereich zu wählen.

Wenn der DCA-Zeitraum lang ist und viele Ebenen entstehen, kann ein starker Preisanstieg dazu führen, dass die Positionskosten zu hoch werden und ein Stop-Loss nicht mehr möglich ist. Dies erfordert eine angemessene Festlegung der DCA-Ebenen, abhängig vom gesamten Positionsvolumen und den maximal tragfähigen Positionskosten.

Optimierungsvorschläge

-

Optimierung des Timing-Signals: Es können verschiedene Parameter und Indikatorkombinationen getestet werden, um Signale mit höherer Trefferquote auszuwählen.

-

Optimierung des Stop-Loss-Mechanismus: Es kann getestet werden, ob ein Λ-förmiger Stop-Loss oder ein bogenförmiger Stop-Loss den einfachen Trailing-Stop-Loss ersetzt, um bessere Stop-Loss-Ergebnisse zu erzielen. Auch eine gestaffelte Positionsanpassung zur Änderung des Stop-Loss-Bereichs ist möglich.

-

Optimierung der Gewinnmitnahme: Verschiedene Arten von trailing Gewinnmitnahmen können getestet werden, um bessere Ausstiegszeitpunkte zu finden und die Gesamtrendite zu steigern.

-

Einführung eines Anti-Erholungsmechanismus: Nach einem Stop-Loss kann es vorkommen, dass erneut ein DCA-Signal ausgelöst wird und eine neue Position eröffnet wird. In diesem Fall kann ein gewisser Anti-Erholungsbereich eingeführt werden, um eine sofortige aggressive Neueröffnung nach einem Stop-Loss zu vermeiden.

Zusammenfassung

Diese Strategie nutzt den RSI-Indikator zur Bestimmung des Kaufzeitpunkts sowie eine dynamische DCA-Strategie mit exponentiell berechneten Stop-Loss-Ebenen, um die Anzahl und Kosten der Positionen dynamisch anzupassen und so einen Preisvorteil in Schwankungsmärkten zu erzielen. Die Optimierungsansätze konzentrieren sich hauptsächlich auf Ein- und Ausstiegssignale sowie Stop-Loss- und Gewinnmitnahmemethoden. Insgesamt verwendet die Strategie das Kernprinzip der exponentiellen DCA, um die Positionskosten kontinuierlich zu senken, was in Seitwärtsmärkten mehr Spielraum und in Trendmärkten höhere Renditen ermöglicht. Dennoch müssen je nach eigenem Kapitalmanagementplan geeignete Parameter gewählt werden, um das Gesamtpositionsrisiko zu kontrollieren.

- 1