Quantitative Kombinationsstrategie aus dreifachem gleitendem Durchschnitt und MACD

Überblick

Diese Strategie entwickelt durch die Kombination eines dreifachen gleitenden Durchschnitts (EMA) und des MACD-Indikators einen relativ stabilen und zuverlässigen quantitativen Handelsansatz. Ziel ist es, zukünftige Trends zu erfassen, insbesondere für mittel- bis langfristige Positionen.

Strategieprinzip

Die Strategie basiert hauptsächlich auf der Kombination eines dreifachen gleitenden Durchschnitts und des MACD-Indikators.

Zunächst werden drei exponentielle gleitende Durchschnitte (EMAs) mit den Längen 3, 7 und 2 verwendet. Diese drei gleitenden Durchschnitte bilden ein System von schnell zu langsam, um die zukünftige Trendrichtung zu bestimmen. Wenn der kurzfristige gleitende Durchschnitt den längerfristigen von unten nach oben kreuzt, ist dies ein Long-Signal; kreuzt er von oben nach unten, ist dies ein Short-Signal.

Zweitens wird gleichzeitig der MACD-Indikator mit den Parametern 3 und 7 eingesetzt. Wenn die MACD-Hauptlinie die Signallinie von unten nach oben kreuzt, ist dies ein Long-Signal; kreuzt sie von oben nach unten, ein Short-Signal.

Durch die Kombination zweier Indikatoren können mehrfache Fehlsignale eines einzelnen Indikators vermieden werden, was die Stabilität der Strategie erhöht.

Vorteile der Strategie

- Doppelte Indikatorfilterung verbessert die Signalqualität

- Parameter wurden mehrfach getestet und optimiert – stabil und zuverlässig

- Das dreifache gleitende Durchschnittssystem filtert Marktrauschen effektiv und erkennt zukünftige Trends

- Die relativ schnelle MACD-Parametrierung ermöglicht das schnelle Erfassen kurzfristiger Chancen

Risiken der Strategie

- Besteht ein gewisses Risiko von Drawdowns und aufeinanderfolgenden Verlusten

- In Phasen ohne klaren Trend treten vermehrt Fehltrades auf

- Der MACD-Indikator neigt zu Fehlsignalen und muss mit gleitenden Durchschnitten kombiniert werden

Lösungsansätze

- Einsatz geeigneter Stop-Loss-Strategien zur Begrenzung des maximalen Drawdowns

- Bei eindeutig trendlosem Markt die Handelsfrequenz reduzieren

- Optimierung der MACD-Parameter und Kombination mit anderen Indikatoren

Optimierungsmöglichkeiten

- Testen und Optimieren der Parameter der gleitenden Durchschnitte und des MACD, um die beste Kombination zu finden

- Hinzufügen von Hilfsindikatoren wie KDJ oder VRSI zur Vermeidung von Fehlsignalen

- Integration von Machine-Learning-Modellen zur Marktanalyse und dynamischen Anpassung

- Kombination mit einer Stop-Loss-Strategie zur Festlegung optimaler Ausstiegspunkte

Zusammenfassung

Diese Strategie erzielt durch die Kombination von gleitenden Durchschnitten und MACD eine stabile Trendfolge. Ihr Vorteil liegt in der Verwendung mehrerer Indikatoren, die Fehlsignale effektiv reduzieren und somit eine bessere Performance ermöglichen. In einem nächsten Schritt kann die Strategie durch Parameteroptimierung, Einführung von Stop-Loss und dynamische Anpassung weiter verbessert werden, um ein effektives Werkzeug für die Suche nach mittel- bis langfristigen Chancen zu werden.

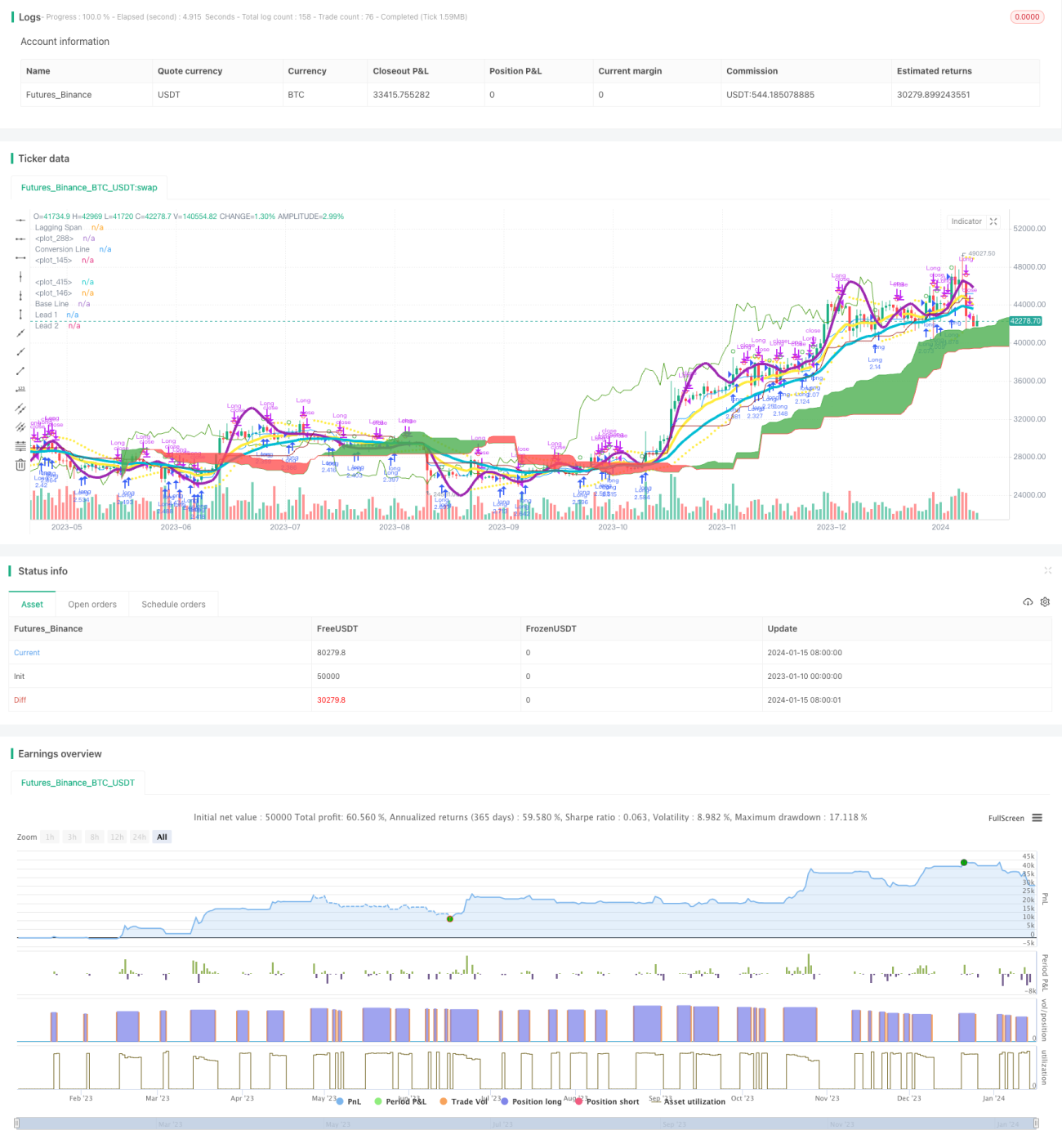

/*backtest

start: 2023-01-10 00:00:00

end: 2024-01-16 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=3

strategy("Matt's MACD Algo v1", shorttitle="Matt's MACD Algo v1", overlay=true, pyramiding = 0, default_qty_type = strategy.percent_of_equity, default_qty_value = 100, initial_capital=7000, calc_on_order_fills = true, commission_type=strategy.commission.percent, commission_value=0, currency = currency.USD)

//study("MFI Fresh", shorttitle="MFI Fresh", overlay=true)

- 1