Hybride Handelsstrategie

Überblick

Die handelsstrategie "S&P500 gemischte Saisonalität" ist eine quantitative Strategie, die saisonale Muster für Aktienhandel nutzt. Sie kombiniert ein verstärktes Buy-and-Hold-System, Bedingungen technischer Indikatoren und den Volumenflussindikator, um zwischen besseren und schlechteren Handelsmonaten im Jahr zu rotieren.

Strategieprinzip

Die Handelssignale und Regeln der Strategie sind wie folgt:

- Long-Einstieg bei Eröffnung des ersten Handelstages im Oktober.

- Wenn der VIX über 60 % oder der 15-Tage-ATR über 90 % liegt, werden saisonale Trades ausgesetzt, bis sich die Marktvolatilität gelegt hat.

- Schließen der Position bei Eröffnung des ersten Handelstages im August.

- Ein Ausstiegssignal wird auch ausgelöst, wenn der VIX über 120 % steigt oder der Volumenflussindikator VFI unter -20 fällt und die 10-Tage-Durchschnittslinie nach unten zeigt.

- Optional können Leerverkäufe hinzugefügt werden.

Die Strategie nutzt die ungleiche Performance des Aktienmarktes im Jahresverlauf: In historisch starken Monaten (Oktober bis April) wird long gegangen, in schwachen Monaten (Mai bis September) werden Gewinne mitgenommen oder es wird short gegangen. Gleichzeitig werden technische Indikatoren als Filter verwendet, um bei starken Marktbewegungen Trades auszusetzen und Risiken zu vermeiden.

Vorteilanalyse

Die Strategie "S&P500 gemischte Saisonalität" bietet folgende Vorteile:

- Nutzung stabiler saisonaler Muster. Die Strategie basiert auf der Tatsache, dass der S&P500-Index in verschiedenen Monaten signifikant unterschiedliche Performances aufweist.

- Kombination mehrerer Filter. Die Einbeziehung von VIX, ATR, VFI und anderen Bedingungen filtert Rauschen effektiv und erzeugt zuverlässigere Handelssignale.

- Konfigurierbare Handelsregeln. Die Strategie kann optional Long- oder Short-Positionen einbeziehen, die Handelsmonate sind anpassbar und leicht zu testen und zu optimieren.

- Integrierter Risikovermeidungsmechanismus. Die Volatilitätsprüfung durch VIX und ATR kann die Auswirkungen extremer Marktbewegungen effektiv vermeiden.

- Unterstützung durch den Volumenflussindikator. Der VFI spiegelt den Kapitalfluss der Marktteilnehmer wider und bietet eine zusätzliche Entscheidungsgrundlage.

Risikoanalyse

Die Strategie birgt auch einige potenzielle Risiken:

- Risiko des Wegfalls historischer Muster. Der Aktienmarkt ist stark unsicher, historische Muster sind nicht immer gültig.

- Risiko falscher Signale technischer Indikatoren. Indikatoren wie VIX, ATR und VFI können Fehlinterpretationen liefern.

- Risiko unzureichender Parameteroptimierung. Die Parameter können weiter getestet und optimiert werden; die aktuellen sind möglicherweise nicht optimal.

- Zusätzliches Risiko durch Leerverkäufe. Optionale Leerverkäufe bergen das Risiko unbegrenzter Verluste.

Diese Risiken können durch Risikomanagement, Indikatorkombinationen, Parameteranpassung und den Einsatz von maschinellem Lernen weiter reduziert werden.

Optimierungsmöglichkeiten

Die Strategie kann in folgenden Bereichen weiter optimiert werden:

- Test mit längeren historischen Daten. Mehr historische Daten können verwendet werden, um die Strategieparameter neu zu testen und zu optimieren.

- Integration eines Stop-Loss-Mechanismus. Ein nachlaufender Stop-Loss oder zeitbasierter Stop-Loss kann einzelne Verluste begrenzen.

- Optimierung der Indikatorparameter. Parameter von VIX, ATR und VFI können angepasst werden, um die optimale Kombination zu finden.

- Einführung von maschinellem Lernen. Neuronale Netze oder Entscheidungsbäume können zur adaptiven Parameteroptimierung eingesetzt werden.

- Strategiekombination. Tests mit anderen Strategien können die Systemrisiken durch niedrige Korrelation reduzieren.

Zusammenfassung

Die Strategie "S&P500 gemischte Saisonalität" kombiniert bewährte saisonale Muster, technische Indikatoren und den Volumenflussindikator. Sie vermeidet die schwächsten Monate des Aktienmarktes, investiert in die besseren Handelsmonate und verfügt über einen integrierten Filter für Marktvolatilität, was zu stabilen Überrenditen führen kann. Gleichzeitig ist die Strategie leicht zu testen, zu optimieren und anzupassen und bietet quantitativen Händlern einen referenzierbaren und weiterentwickelbaren Rahmen. Durch die Einbeziehung weiterer Daten, Stop-Loss-Maßnahmen, Parameteranpassungen und Kombinationen kann die Wirkung der Strategie voraussichtlich verstärkt werden.

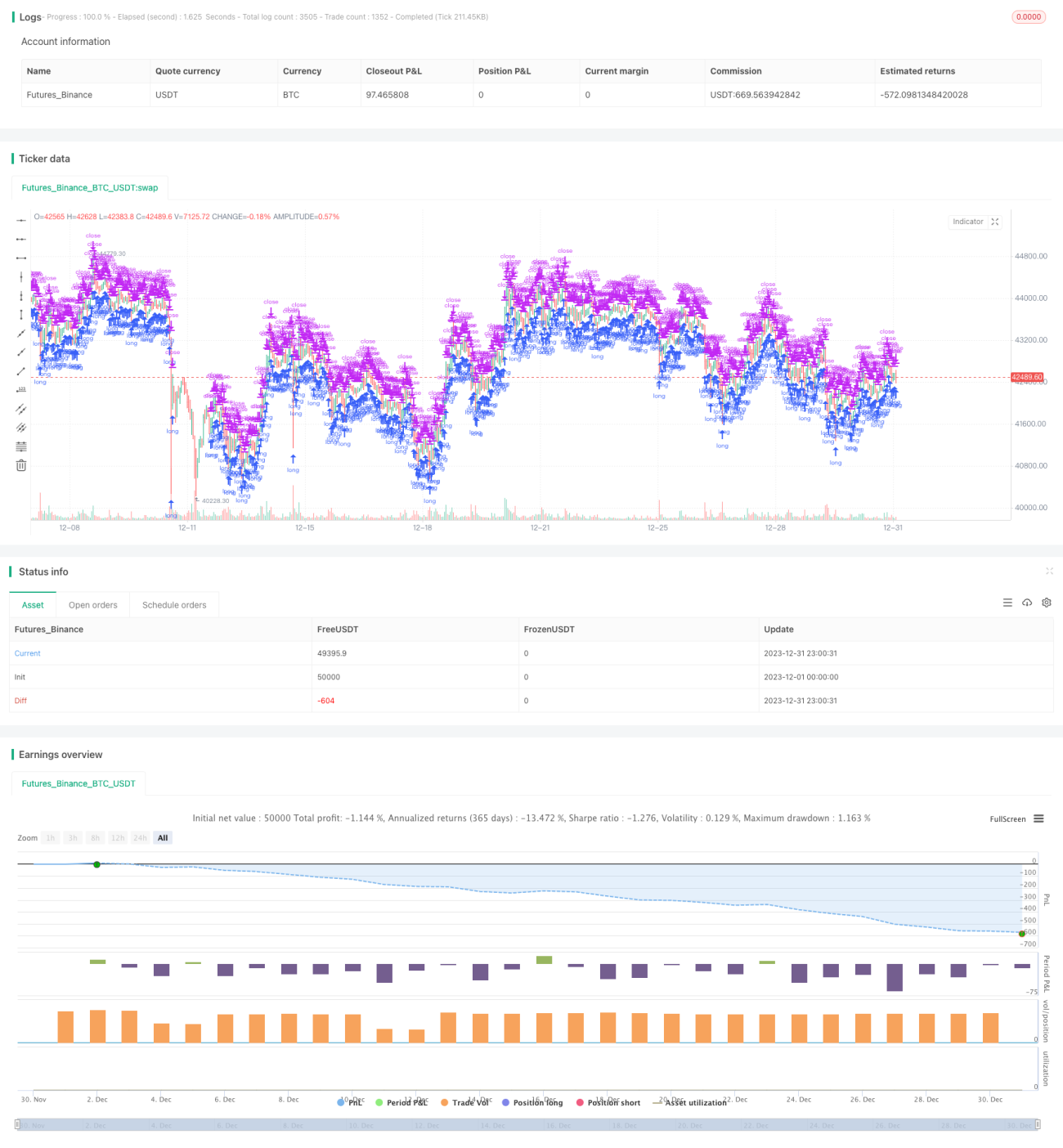

/*backtest

start: 2023-12-01 00:00:00

end: 2023-12-31 23:59:59

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// TASC Issue: April 2022 - Vol. 40, Issue 4

// Article: Sell In May? Stock Market Seasonality

// Article By: Markos Katsanos

// Language: TradingView's Pine Script v5- 1