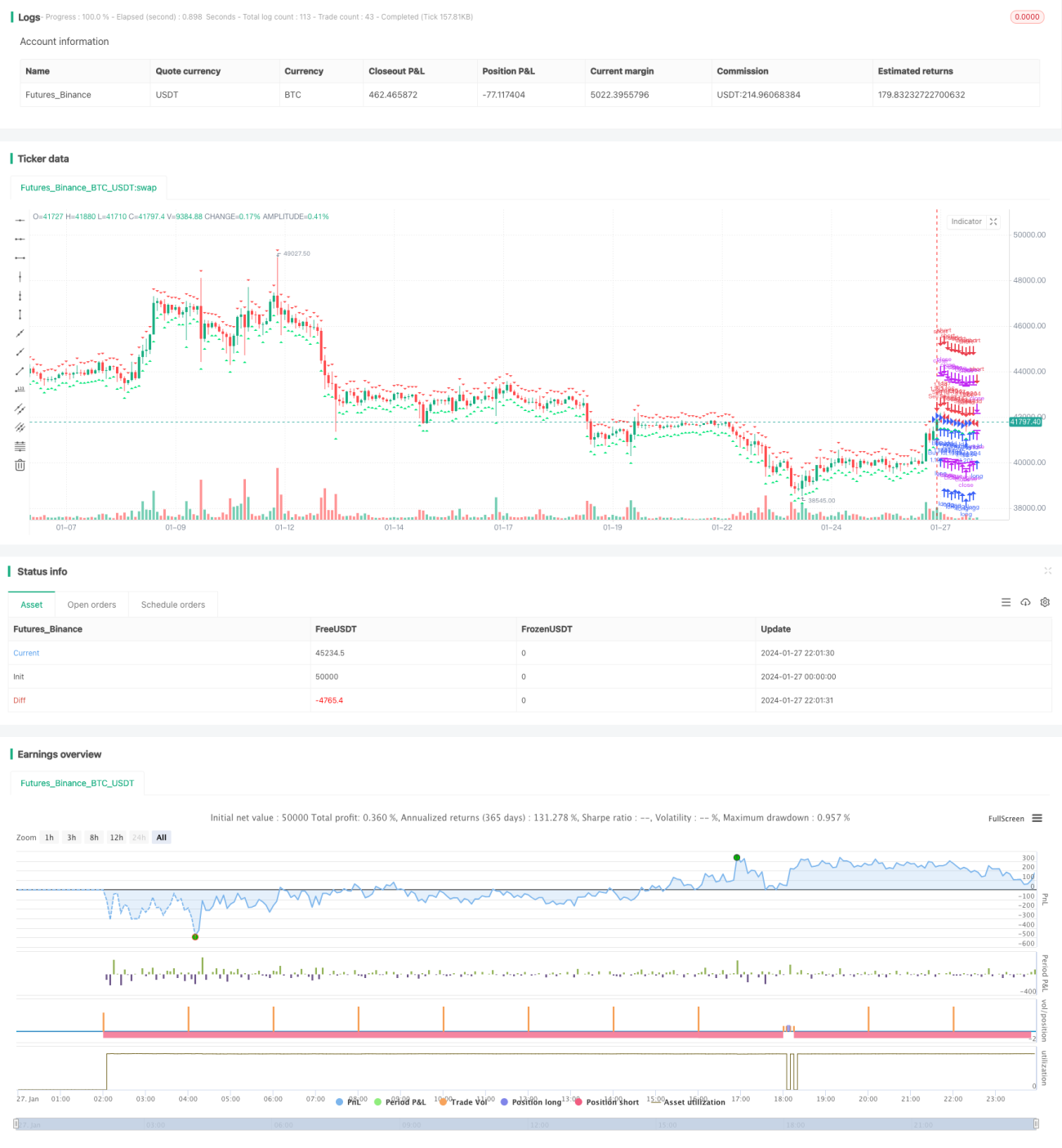

PPO Preissensitive Momentum-Double-Bottom-Directional-Trading-Strategie

Überblick

Die PPO-Price Sensitivity Dynamics Binary-Orientierung ist eine Handelsstrategie, bei der der Preis-Sensitivity-Dynamics-Indikator genutzt wird, um Trends zu verfolgen, die die Preis-Dynamics bilden. Es kombiniert die Binary-Bildung der PPO-Indikatoren mit der Preis-Dynamics-Charakteristik, um die genaue Position des Preis-Dynamics-Wendepunkts zu ermitteln und somit ein Handelssignal zu erzeugen.

Strategieprinzip

Die Strategie nutzt die PPO-Anzeige, um die doppelte Basis zu bestimmen, und die niedrigsten Punkte in Verbindung mit dem Preis zu bestimmen, um in Echtzeit zu überwachen, ob die PPO-Anzeige eine Bottom-Charakteristik aufweist. Wenn die PPO-Anzeige eine doppelte Basis aufweist, die von unten nach oben umgedreht wird, zeigt dies, dass sie sich derzeit an einem Kaufgelegenheitspunkt befindet.

Auf der anderen Seite arbeitet die Strategie mit dem Preisminimum zusammen, um zu bestimmen, ob der Preis in einem niedrigen Bereich ist. Wenn der Preis in einem niedrigen Bereich ist, erzeugt der PPO-Indikator ein Kaufsignal, wenn ein Bodenzeichen auftritt.

Durch die doppelte Beurteilung der PPO-Indikator-Umkehrcharakteristik und der Bestätigung der Preisposition kann die Chance auf eine Preisumkehr effektiv erkannt, einige falsche Signale gefiltert und die Qualität der Signale verbessert werden.

Analyse der Stärken

-

Die Doppel-Boden-Form des PPO-Indikators ermöglicht eine genaue Bestimmung des Kaufzeitpunkts.

-

In Kombination mit der Bestimmung der Preisposition kann das falsche Signal, das von höheren Punkten erzeugt wird, gefiltert und die Signalqualität verbessert werden.

-

Die PPO-Indikatoren sind empfindlich und können schnell Trendveränderungen bei den Preisen erfassen. Sie sind geeignet, Trends zu verfolgen.

-

Die Verwendung von Doppelbestätigungsmechanismen verringert das Transaktionsrisiko.

Risiken und Lösungen

-

PPO-Indikatoren sind leicht zu falschen Signalen und müssen mit anderen Indikatoren bestätigt werden. Sie können mit einem Gleichgewichts- oder Schwankungsindikator unterstützt werden.

-

Die doppelte Bottom-Reversal ist nicht dauerhaft, es besteht die Gefahr, wieder zu fallen. Sie können einen Stop-Loss-Punkt setzen, um die Positionsverwaltung zu optimieren.

-

Unkorrekt eingestellte Parameter können zu einem Risiko von Leakage oder Fehlverkäufen führen. Die Parameterkombinationen müssen wiederholt getestet und optimiert werden.

-

Es gibt eine große Menge an Code, der weiter modularisiert werden kann, wodurch die Anzahl der Duplikate reduziert wird.

Optimierungsrichtung

-

Die Einführung eines Stop-Loss-Moduls und die Optimierung der Positionsmanagement-Strategie.

-

Zusätzliche Bestätigung durch die Einführung von Mittellinien- oder Schwankungsindikatoren.

-

Modularisierte Codes, reduziert die Logik der Wiederholung der Urteile.

-

Weiter optimieren, um die Stabilität zu verbessern.

-

Test der Anwendung von Arbitrage bei weiteren Sorten.

Zusammenfassen

Die PPO-Preissensitivitätsdynamik bi-Basis-orientierte Handelsstrategie ermöglicht die effektive Positioning für die Preiswendepunkte durch die Erfassung der doppelten Basis-Charakteristik des PPO-Indikators in Verbindung mit der doppelten Bestätigung der Preisposition. Im Vergleich zu einer einzelnen Indikatorentscheidung hat die Strategie den Vorteil, dass sie eine genauere Urteilsfähigkeit und ein besseres Geräuschfilter hat.

- 1