Das Breakout-Reversal-Modell basierend auf der Turtle-Trading-Strategie

Übersicht

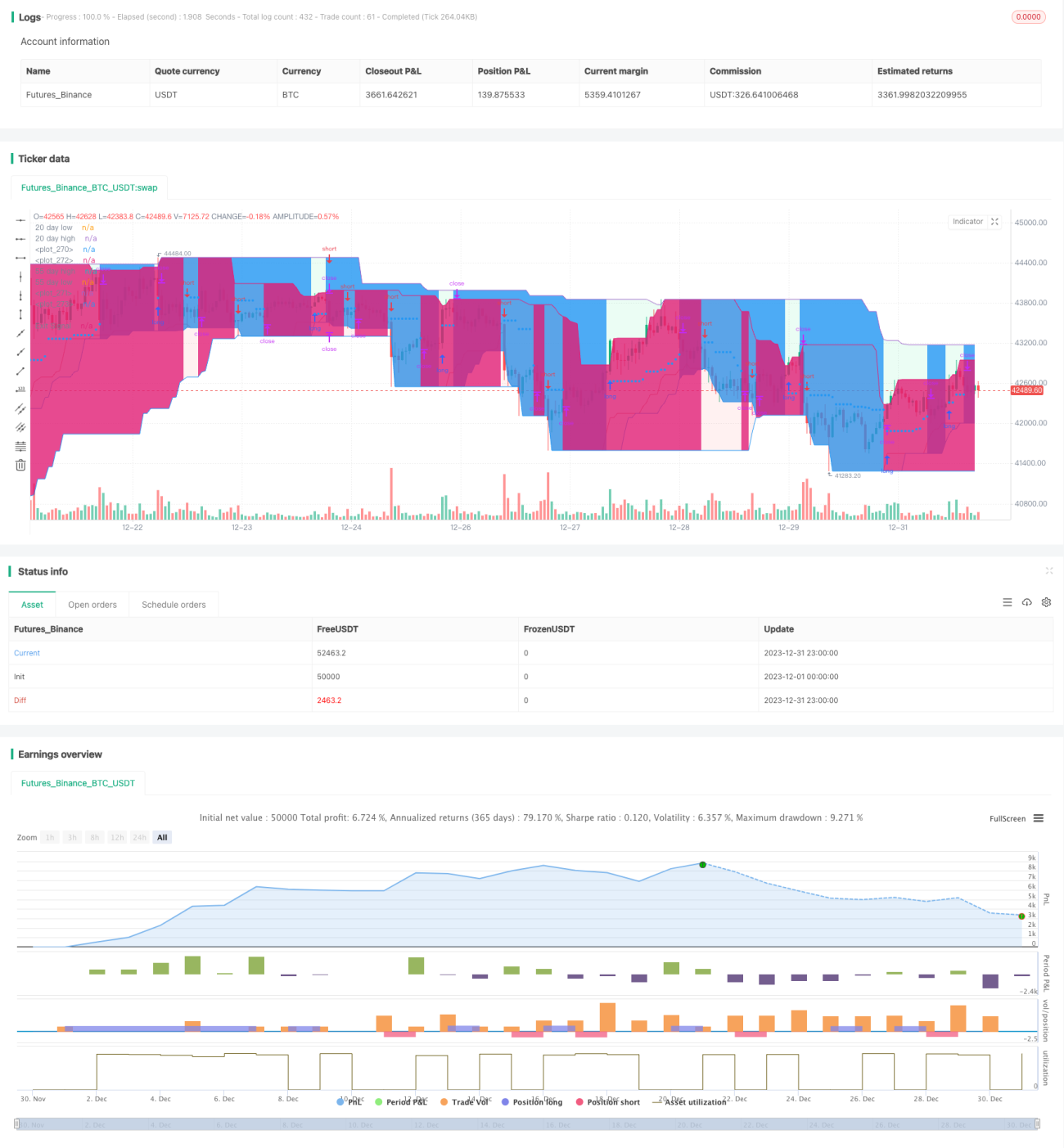

Diese Strategie basiert auf der bekannten 'Turtle-Trader-Strategie', die seit vielen Jahren validiert ist. Sie generiert Long- und Short-Signale und ermöglicht bis zu 5 Pyramid-Orders, was bedeutet, dass die Strategie bis zu 5 Aufträge in derselben Richtung auslösen kann. Sie verfügt über ein gutes Risiko- und Geldmanagement.

Es ist zu beachten, dass die Strategie zwei zusammenarbeitende Systeme (S1 und S2) kombiniert.

Strategieprinzip

Die Positionsgröße ist für Turtle Trader sehr wichtig, um Risiken angemessen zu managen. Diese Positionsanpassungsstrategie passt sich der Marktvolatilität und dem Konto (Gewinne und Verluste) an. Sie basiert auf dem ATR (Average True Range), auch als 'N' bezeichnet. Die Länge beträgt standardmäßig 20.

Die Anzahl der Einheiten beträgt:

unit = (percentage_to_risk/100)*account/atr*syminfo.pointvalue

Je nach Ihrer Risikobereitschaft können Sie den Prozentsatz des Kontos erhöhen, aber die Turtle Trader verwenden standardmäßig 1%. Wenn Sie Kontrakte handeln, muss die Einheit standardmäßig abgerundet werden.

Es gibt eine zusätzliche Regel, um das Risiko zu verringern, wenn der Kontowert unter das Anfangskapital fällt: In diesem Fall muss in der Einheitenformel Folgendes ersetzt werden:

account := (strategy.equity-strategy.openprofit)*(strategy.equity-strategy.openprofit)/strategy.initial_capital

Es gibt zwei Systeme, die zusammenarbeiten:

Ein Ausbruch ist ein neues Hoch oder ein neues Tief. Wenn es ein neues Hoch ist, eröffnen wir eine Long-Position, umgekehrt, wenn es ein neues Tief ist, gehen wir eine Short-Position ein.

Wir fügen eine zusätzliche Regel hinzu:

Diese zusätzliche Regel erlaubt es dem Händler, am Haupttrend teilzunehmen, wenn das Signal von System 1 ausgelassen wurde. Wenn das Signal von System 1 ausgelassen wurde und die nächste Kerze ebenfalls einen neuen 20-Tage-Ausbruch darstellt, sendet S1 kein Signal. Wir müssen auf das Signal von S2 warten oder auf eine Kerze, die keinen neuen Ausbruch erzeugt, um S1 zu reaktivieren.

Vorteilsanalyse

Die Turtle-Strategie erlaubt es uns, zusätzliche Einheiten zur Position hinzuzufügen, wenn sich der Kurs zu unseren Gunsten bewegt. Ich habe die Strategie so konfiguriert, dass bis zu 5 Aufträge in derselben Richtung hinzugefügt werden können. Wenn sich der Kurs also vom Einstiegskurs wegbewegt, fügen wir Einheiten hinzu.

Wir setzen den ersten Auftrag (Long oder Short) als maximalen Auftrag. Die nachfolgenden Pyramid-Orders werden weniger Einheiten haben als der erste Auftrag.

Wir setzen einen maximalen Stop-Loss von 10% für den ersten Auftrag, was bedeutet, dass Sie nicht mehr als 10% des Wertes des ersten Auftrags verlieren. Da der Stop-Loss jedoch um 0,5 * ATR(20) erhöht/verringert wird, können Ihre Pyramid-Orders mehr verlieren, wobei dann nicht garantiert ist, dass der Verlust 10% nicht übersteigt. Das Risiko ist dennoch gut gemanagt, da diese Aufträge einen geringeren Wert als der erste Auftrag haben.

Risikoanalyse

Das größte Risiko dieser Strategie liegt in übermäßig großen Positionen. Da die Aufträge als Market Orders ausgeführt werden, können mehrere große Market Orders gleichzeitig einen erheblichen Einfluss auf den Kurs haben und große Slippage verursachen. Dies kann zu erheblichen Kapitalverlusten führen.

Ein weiteres Risiko ist eine unangemessene Konfiguration des Geldmanagements. Fehlerhafte Stop-Loss-Einstellungen oder zu große Prozentsätze können zu enormen Verlusten führen. Dies erfordert eine sorgfältige Konfiguration entsprechend der eigenen Risikobereitschaft.

Optimierungsrichtungen

-

Es können verschiedene Parameter hinsichtlich ihrer Auswirkungen auf Rendite und Sharpe Ratio getestet werden, wie ATR-Periode, ATR-Multiplikator des Stop-Loss usw. Finden Sie die optimale Parameterkombination.

-

Es können verschiedene Ein- und Ausstiegsregeln getestet werden, z.B. die Verwendung von Kerzenformationen als zusätzliche Filterbedingungen.

-

Es können andere Arten von Stop-Loss ausprobiert werden, wie Trailing Stop, dynamischer Stop-Loss. Dies kann die Wahrscheinlichkeit verringern, dass der Stop-Loss durchbrochen wird.

-

Es kann die Anzahl der Pyramid-Orders getestet werden. Je mehr Aufträge, desto höher der Hebel und das Risiko. Finden Sie den optimalen Gleichgewichtspunkt.

-

Es kann versucht werden, den Handel in bestimmten Zeiträumen (z.B. vor der Veröffentlichung der US-Arbeitsmarktdaten) zu stoppen, um die Auswirkungen wichtiger Ereignisse zu vermeiden.

Zusammenfassung

Insgesamt weist die Strategie ein ausgewogenes Verhältnis von Risiko und Ertrag auf und eignet sich für mittel- bis langfristige Trendgeschäfte. Sie hat Vorteile wie systematischen Handel und kontrollierbares Risiko. Durch Optimierung können die Stabilität und die Rendite der Strategie weiter verbessert werden.

- 1