Auf mehreren Indikatoren basierende Trendfolgestrategie

Überblick

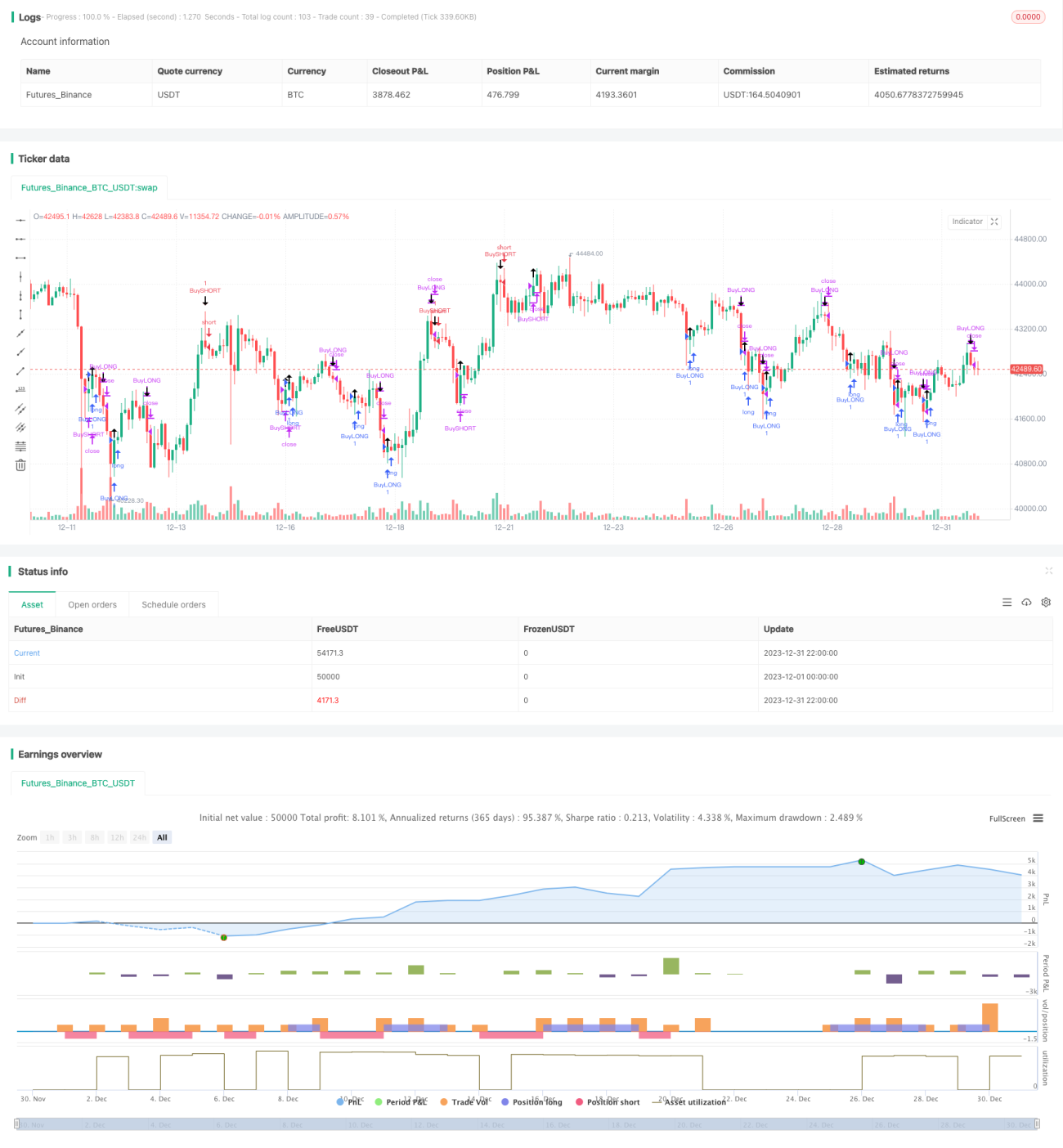

Die Strategie identifiziert Trends durch die Kombination mehrerer Indikatoren und setzt einen nachlaufenden Stop-Loss zur Sicherung von Gewinnen ein. Hauptsächlich werden Bollinger-Bänder, RSI und ADX zur Bestimmung des Einstiegszeitpunkts sowie ATR und Bollinger-Bänder für den Stop-Loss verwendet.

Strategieprinzip

Die wichtigsten Indikatoren der Strategie sind Bollinger-Bänder, RSI und ADX. Wenn sich der Preis dem unteren Bollinger-Band nähert und der RSI unter 30 liegt, wird dies als überverkauft eingestuft und es wird long gegangen. Wenn sich der Preis dem oberen Bollinger-Band nähert und der RSI über 70 liegt, wird dies als überkauft eingestuft und es wird short gegangen. Wenn der ADX über 25 liegt, wird ein Trend als vorhanden betrachtet, wodurch die Long-/Short-Signale effektiver werden.

Nach der Eröffnung einer Position werden der ATR-Indikator und die oberen/unteren Bollinger-Bänder für den Stop-Loss verwendet. Konkret dient der ATR zum maximalen Stop-Loss-Abstand: Wird der maximale Stop-Loss-Punkt erreicht, wird die Position geschlossen. Die oberen/unteren Bollinger-Bänder dienen zur Festlegung des nachlaufenden Stop-Loss-Punktes, der je nach Preisverlauf in Echtzeit aktualisiert wird.

Vorteilsanalyse

Die Strategie kombiniert mehrere Indikatoren zur Identifizierung von Trends und nutzt einen Stop-Loss-Mechanismus zur Gewinnsicherung und Risikominimierung, was sie zu einer relativ soliden Strategie macht. Die konkreten Vorteile sind:

- Die Verwendung von Bollinger-Bändern zur Erkennung von Überkauft-/Überverkauft-Situationen ermöglicht die Identifizierung von Wendepunkten.

- Die Kombination mit dem RSI-Indikator erhöht die Genauigkeit der Signale.

- Der ADX-Indikator bestätigt das Vorhandensein eines Trends und stellt sicher, dass die Handelsrichtung korrekt ist.

- Der nachlaufende Stop-Loss auf Basis von ATR und Bollinger-Bändern maximiert die Gewinnsicherung.

Risikoanalyse

Die Strategie birgt jedoch auch einige Risiken:

- Mehrere Indikatoren und deren Parametereinstellungen sind anfällig für Überoptimierung.

- Bei breiten Bollinger-Bändern können Überkauft-/Überverkauft-Signale weniger effektiv sein.

- Ein falsch eingestellter nachlaufender Stop-Loss kann zu größeren Verlusten führen.

Um diese Risiken zu mindern, können folgende Maßnahmen ergriffen werden:

- Mehrere Parametersätze testen, um Überoptimierung zu vermeiden.

- Die Bollinger-Band-Parameter an die Marktvolatilität anpassen.

- Den Stop-Loss-Abstand testen, um sicherzustellen, dass normale Preisschwankungen verkraftet werden.

Optimierungsmöglichkeiten

Die Strategie kann in folgenden Bereichen optimiert werden:

- Hinzufügen einer Positionsgrößensteuerung, die die Positionsgröße basierend auf dem Stop-Loss-Multiplikator anpasst.

- Ein Modul für Geldmanagement einbauen, um den maximalen Verlust pro Trade streng zu begrenzen.

- Testen anderer Stop-Loss-Indikatoren wie DMI, Envelopes usw.

- Integration eines maschinellen Lernmodells zur Bewertung der Trendwahrscheinlichkeit, um die Effektivität zu steigern.

Zusammenfassung

Insgesamt handelt es sich bei dieser Strategie um einen relativ robusten Trendfolgeansatz. Durch die Mehrfachindikatoranalyse zur Bestimmung der Trendrichtung und den Einsatz von Stop-Loss-Maßnahmen zur Risikokontrolle lassen sich gute Renditen erzielen. Es wurden mehrere Optimierungsrichtungen vorgeschlagen, die bei weiterer Verfeinerung zu noch besseren Ergebnissen führen können.

/*backtest

start: 2023-12-01 00:00:00

end: 2023-12-31 23:59:59

period: 2h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=3

// THIS SCRIPT IS MEANT TO ACCOMPANY COMMAND EXECUTION BOTS

// THE INCLUDED STRATEGY IS NOT MEANT FOR LIVE TRADING

// THIS STRATEGY IS PURELY AN EXAMLE TO START EXPERIMENTATING WITH YOUR OWN IDEAS- 1