Doppel-MA-Momentum-Durchbruchsstrategie

Übersicht

Die Dual-MA-Momentum-Ausbruchsstrategie ist eine quantitative Handelsstrategie, die einen doppelten gleitenden Durchschnitt (MA) mit dem RSI-Indikator kombiniert. Die Strategie berechnet einen schnellen gleitenden Durchschnitt, einen langsamen gleitenden Durchschnitt und den RSI-Indikator, legt überkaufte/überverkaufte Schwellenwerte für den Momentum-Indikator RSI fest und geht bei einem Goldenen Kreuz der beiden MAs long, bei einem Todeskreuz short, um Trendbewegungen des Marktes zu erfassen.

Funktionsprinzip

Die Dual-MA-Momentum-Ausbruchsstrategie basiert hauptsächlich auf dem doppelten gleitenden Durchschnitt und dem RSI-Indikator. Zunächst werden ein schneller und ein langsamer gleitender Durchschnitt berechnet: Die schnelle Linie ist ein 10-Tage gewichteter gleitender Durchschnitt, die langsame Linie ein 100-Tage linear adaptiver gleitender Durchschnitt. Dann wird der 14-Tage-RSI berechnet und überkaufte/überverkaufte Schwellenwerte festgelegt. Wenn die schnelle Linie die langsame Linie von unten nach oben kreuzt, wird ein bullischer Trend angenommen; kreuzt die schnelle Linie die langsame Linie von oben nach unten, ein bärischer Trend. Gleichzeitig mit der Trendbestimmung muss der RSI über der überkauften Linie oder unter der überverkauften Linie liegen, um falsche Ausbrüche effektiv zu filtern.

Konkret: Bei bullischem Trend, wenn der RSI über der überkauften Linie liegt, wird eine Long-Position eröffnet; bei bärischem Trend, wenn der RSI unter der überverkauften Linie liegt, wird eine Short-Position eröffnet. Nach der Eröffnung wird bei Umkehr des Handelssignals die gegenteilige Position eröffnet.

Vorteile der Strategie

Die Dual-MA-Momentum-Ausbruchsstrategie kombiniert die doppelten MAs mit dem RSI-Indikator, um Markttrends effektiv zu identifizieren und mithilfe des RSI falsche Ausbrüche zu filtern, wodurch die Zuverlässigkeit der Handelssignale erhöht wird. Im Vergleich zu einem einfachen MA-System reduziert diese Strategie die Anzahl ineffektiver Trades erheblich. Darüber hinaus bietet die Parametrisierung des RSI Flexibilität für die Strategie.

Risiken der Strategie

Die Dual-MA-Momentum-Ausbruchsstrategie birgt auch gewisse Risiken. Das Dual-MA-System reagiert sehr empfindlich auf Parameter und erfordert sorgfältige Tests von Parameterkombinationen für verschiedene Märkte. Zudem können falsch gewählte Schwellenwerte des RSI zu verpassten Handelsmöglichkeiten führen. Schließlich kann ein aggressiver nachlaufender Stop-Loss unter bestimmten Marktbedingungen durchbrochen werden; die Stop-Loss-Punkte sollten daher anhand von Backtest-Ergebnissen angepasst werden.

Optimierung der Strategie

Die Dual-MA-Momentum-Ausbruchsstrategie kann in folgenden Bereichen optimiert werden:

- Optimierung der Parameter des schnellen und langsamen MA zur Ermittlung der besten Parameterkombination.

- Optimierung der RSI-Parameter durch Anpassung der überkauften/überverkauften Schwellenwerte.

- Einführung eines adaptiven nachlaufenden Stop-Loss-Mechanismus zur Risikokontrolle.

- Hinzufügen eines Moduls zur Optimierung des Eröffnungsvolumens, um die Kapitaleffizienz zu steigern.

Zusammenfassung

Die Dual-MA-Momentum-Ausbruchsstrategie nutzt das Dual-MA-System zur Bestimmung der Trendrichtung und filtert Signale mit dem RSI-Indikator, wodurch die Nachteile eines einfachen MA-Systems wirksam behoben werden. Die Strategie bietet großen Spielraum für Parameteroptimierung und kann adaptiv angepasst werden; sie ist eine exzellente Trendfolgestrategie.

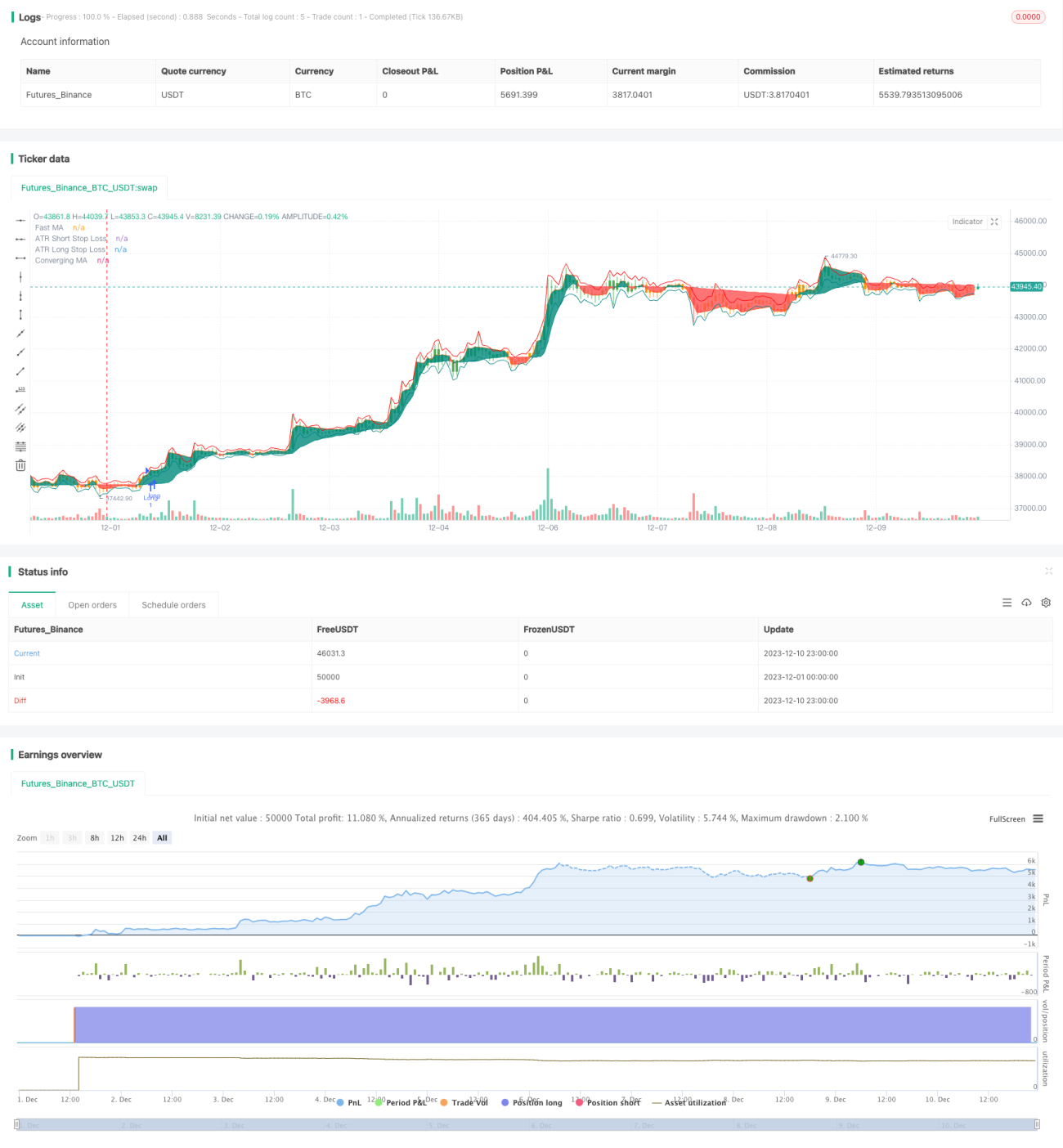

/*backtest

start: 2023-12-01 00:00:00

end: 2023-12-10 23:59:59

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This work is licensed under a Attribution-NonCommercial-ShareAlike 4.0 International (CC BY-NC-SA 4.0) https://creativecommons.org/licenses/by-nc-sa/4.0/

// © Salman4sgd

//@version=5- 1