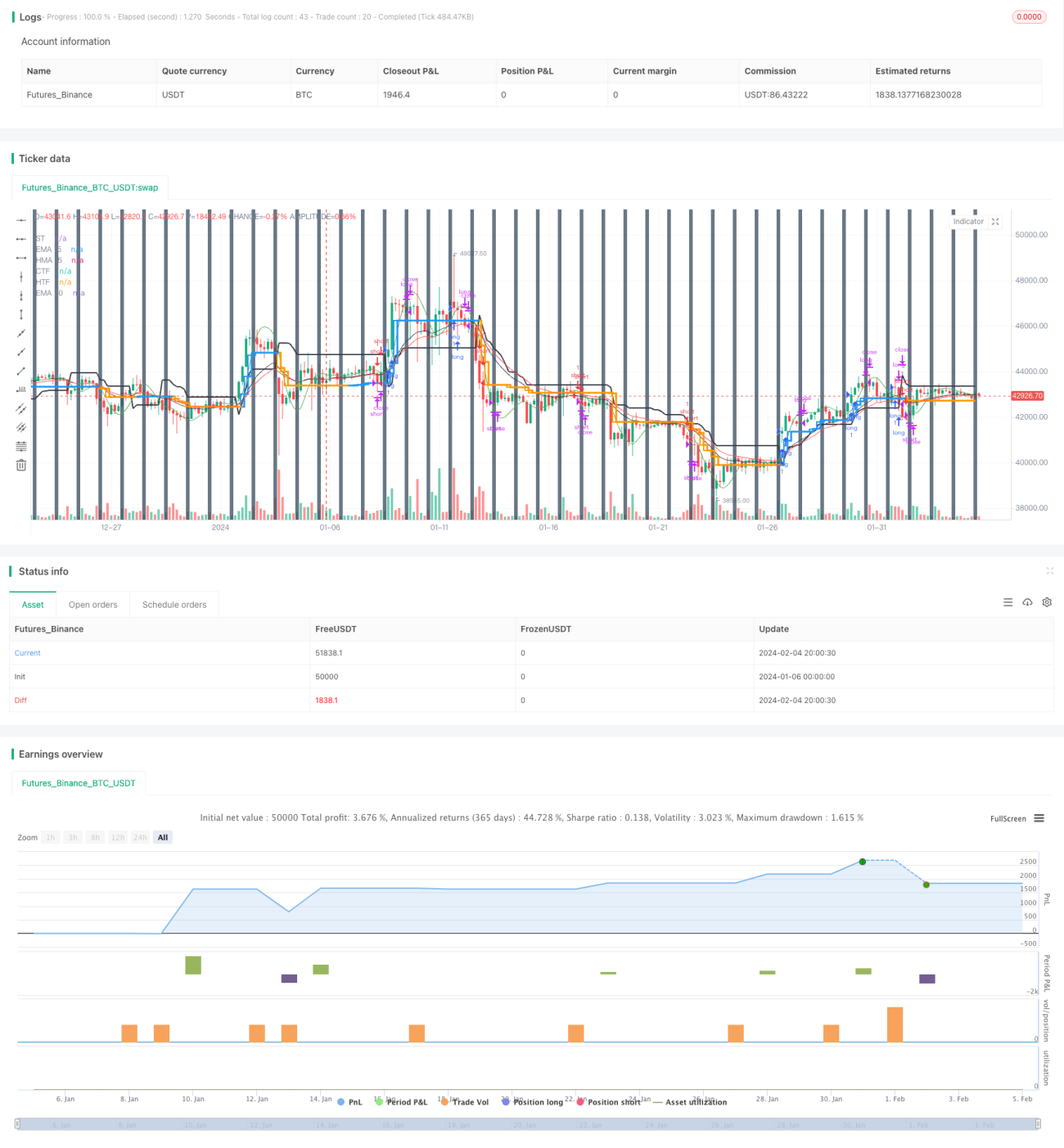

Auf Heikin Ashi basierte Super-Trend-Trailing-Stop-Loss-Strategie

Strategieübersicht

Diese Strategie ist eine Trendfolge-Stopp-Loss-Strategie, die Heikin-Ashi-Kerzen und den Supertrend-Indikator kombiniert. Sie nutzt Heikin-Ashi-Kerzen, um Marktrauschen zu filtern, den Supertrend-Indikator zur Bestimmung der Trendrichtung und verwendet den Supertrend als dynamische Stopp-Loss-Linie, um effizientes Trendfolgen und Risikomanagement zu erreichen.

Strategieprinzip

- Berechnung der Heikin-Ashi-Kerzen: einschließlich Eröffnungskurs, Schlusskurs, Höchstkurs, Tiefstkurs.

- Berechnung des Supertrend-Indikators: Berechnung der oberen und unteren Bänder basierend auf ATR und Kurs.

- Kombination von Heikin-Ashi-Kerzen und Supertrend zur Bestimmung der Trendrichtung.

- Wenn der Schlusskurs des Heikin Ashi näher am oberen Band des Supertrends liegt als der Schlusskurs der vorherigen Kerze, handelt es sich um einen Aufwärtstrend; wenn der Schlusskurs des Heikin Ashi näher am unteren Band des Supertrends liegt als der Schlusskurs der vorherigen Kerze, handelt es sich um einen Abwärtstrend.

- Im Aufwärtstrend wird das obere Band des Supertrends als Trailing-Stopp-Loss verwendet; im Abwärtstrend wird das untere Band des Supertrends als Trailing-Stopp-Loss verwendet.

Strategievorteile

- Durch die Verwendung von Heikin Ashi zur Filterung von Fehlausbrüchen werden Trendsignale zuverlässiger erkannt.

- Der Supertrend dient als dynamischer Stopp-Loss, der die Gewinne des Trends maximal sichert und zu große Drawdowns vermeidet.

- Die Kombination verschiedener Zeitrahmen zur Beurteilung von Long/Short verbessert die Zuverlässigkeit der Signale für Hoch- und Tiefpunkte.

- Die zeitgesteuerte Positionsschließung verhindert die Auswirkungen irrationaler Marktbewegungen zu bestimmten Zeiten.

Strategierisiken

- Bei Trendumkehrungen kann es leicht zu Stopp-Loss-Verlusten kommen. Dieses Risiko kann durch eine etwas großzügigere Stopp-Loss-Linie reduziert werden.

- Eine falsche Einstellung der Supertrend-Parameter kann zu einem zu weiten oder zu engen Stopp-Loss führen. Es sollten verschiedene Parameterkombinationen getestet werden.

- Das Problem des Money-Managements wird nicht berücksichtigt. Es sollte eine Positionsgrößenkontrolle eingerichtet werden.

- Die Transaktionskosten werden nicht berücksichtigt. Die Auswirkungen der Kosten sollten berechnet werden.

Optimierungsrichtungen

- Optimierung der Supertrend-Parameterkombinationen zur Suche nach optimalen Parametern.

- Hinzufügen einer Positionsgrößenkontrollfunktion.

- Berücksichtigung von Kosten wie Gebühren, Slippage usw.

- Flexible Anpassung des Stopp-Loss-Bereichs je nach Trendstärke.

- Erwägung der Kombination mit anderen Indikatoren zur Filterung von Einstiegssignalen.

Zusammenfassung

Diese Strategie vereint die Vorteile von Heikin Ashi und dem Supertrend-Indikator, um die Trendrichtung zu erfassen und gleichzeitig mit dem Supertrend einen automatisierten dynamischen Trailing-Stopp-Loss zu realisieren, wodurch die Trendgewinne gesichert werden. Die Hauptrisiken der Strategie liegen in Trendumkehrungen und Parameteroptimierung, die beide durch weitere Optimierung verbessert werden können. Insgesamt erhöht die Strategie durch die Integration der Indikatoren die Stabilität des Handelssystems und den Gewinnspielraum.

- 1