Kanalausbruch-Umkehrhandelsstrategie

Übersicht

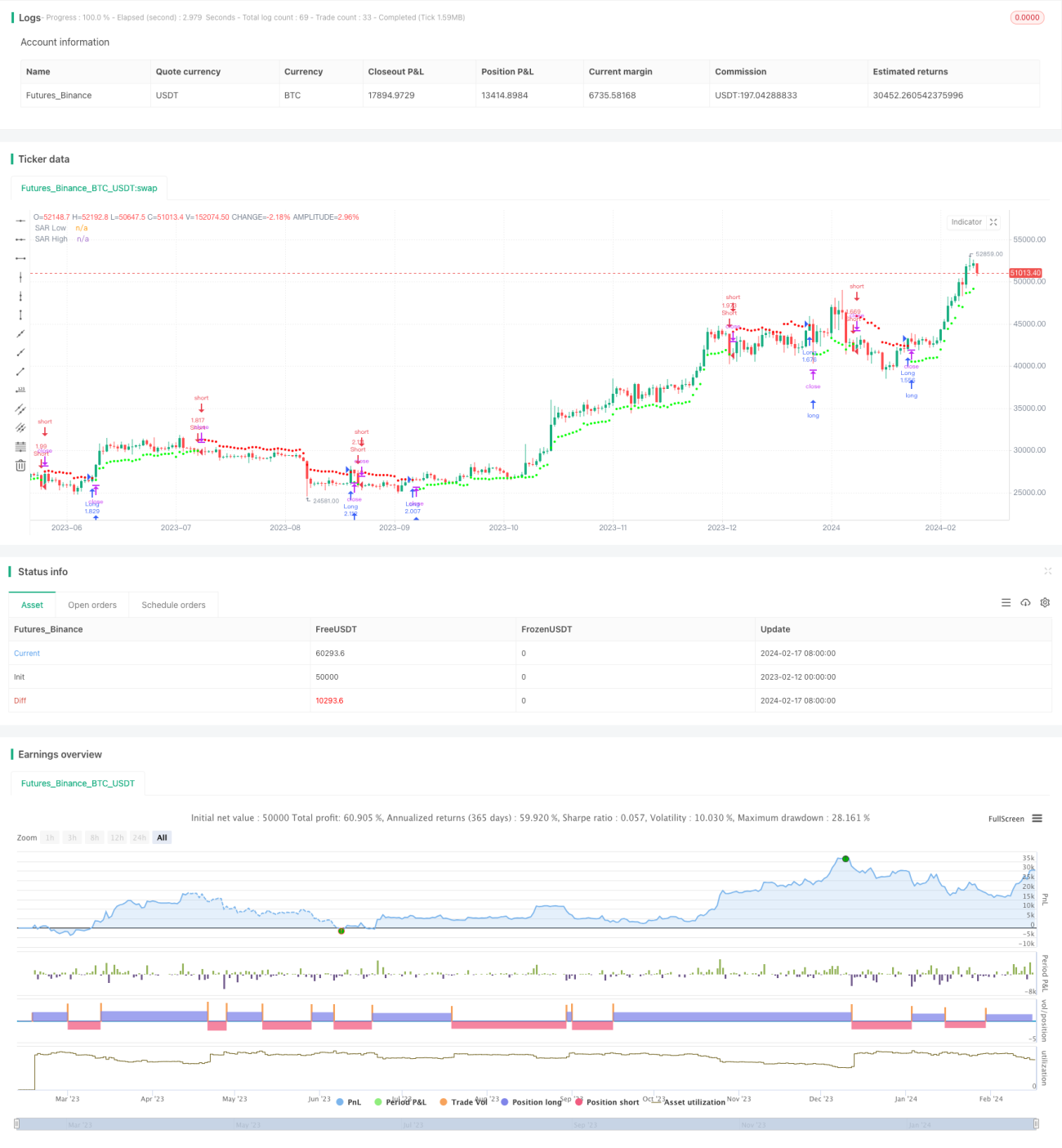

Die Channel-Breakout-Reversal-Strategie ist eine Reversal-Handelsstrategie, die einen gleitenden Take-Profit und Stop-Loss entlang eines Preiskorridors verfolgt. Sie verwendet eine gewichtete gleitende Durchschnittsmethode zur Berechnung des Preiskorridors und eröffnet Long- oder Short-Positionen, wenn der Preis den Korridor durchbricht.

Funktionsweise der Strategie

Die Strategie berechnet zunächst die Volatilität des Preises mithilfe des Average True Range (ATR) von Wilder. Aus dem ATR-Wert wird dann die Average Range Constant (ARC) berechnet. Der ARC entspricht der halben Breite des Preiskorridors. Anschließend werden die obere und untere Schiene des Korridors berechnet, also die Take-Profit- und Stop-Loss-Punkte, die als SAR-Punkte bezeichnet werden. Wenn der Preis die obere Schiene durchbricht, wird short gegangen; bei einem Durchbruch der unteren Schiene wird long gegangen.

Im Einzelnen: Zuerst wird der ATR der letzten N Kerzen berechnet. Dann wird der ATR mit einem Koeffizienten multipliziert, um den ARC zu erhalten. Der mit dem Koeffizienten multiplizierte ATR steuert die Breite des Korridors. Der ARC wird zum höchsten Schlusskurs der letzten N Kerzen addiert, um die obere Schiene (hoher SAR) zu erhalten. Der ARC wird vom niedrigsten Schlusskurs subtrahiert, um die untere Schiene (niedriger SAR) zu erhalten. Wenn der Schlusskurs die obere Schiene durchbricht, wird short gegangen; bei einem Durchbruch der unteren Schiene wird long gegangen.

Vorteile der Strategie

- Durch die Nutzung der Preisvolatilität zur Berechnung eines adaptiven Korridors kann dieser Marktveränderungen verfolgen.

- Reversal-Handel, geeignet für Trendwende-Märkte.

- Gleitende Take-Profit- und Stop-Loss-Levels ermöglichen es, Gewinne zu sichern und Risiken zu kontrollieren.

Risiken der Strategie

- Reversal-Handel kann leicht zu Fehlsignalen führen, Parameter müssen angemessen angepasst werden.

- In stark volatilen Märkten können Positionen leicht ausgelöst werden.

- Ungeeignete Parameter können zu übermäßigem Handel führen.

Lösungsansätze:

- Optimierung des ATR-Zeitraums und des ARC-Koeffizienten, um eine angemessene Korridorbreite zu gewährleisten.

- Kombination mit Trendindikatoren zur Filterung von Einstiegszeitpunkten.

- Vergrößerung des ATR-Zeitraums, um die Handelsfrequenz zu verringern.

Optimierungsmöglichkeiten

- Optimierung des ATR-Zeitraums und des ARC-Koeffizienten.

- Hinzufügen von Eröffnungsbedingungen, z. B. in Kombination mit dem MACD-Indikator.

- Hinzufügen einer Stop-Loss-Strategie.

Zusammenfassung

Die Channel-Breakout-Reversal-Strategie nutzt den Korridor, um Preisbewegungen zu verfolgen, eröffnet bei zunehmender Volatilität Reversal-Positionen und setzt adaptive gleitende Take-Profit- und Stop-Loss-Levels. Diese Strategie eignet sich für seitwärts gerichtete Märkte mit vorherrschenden Trendwendungen und kann bei genauer Identifizierung der Wendepunkte gute Renditen erzielen. Es ist jedoch darauf zu achten, dass die Stop-Loss-Levels nicht zu weit gefasst sind und dass die Parameter optimiert werden.

- 1