Basado en la estrategia de cruce de SMA

Resumen

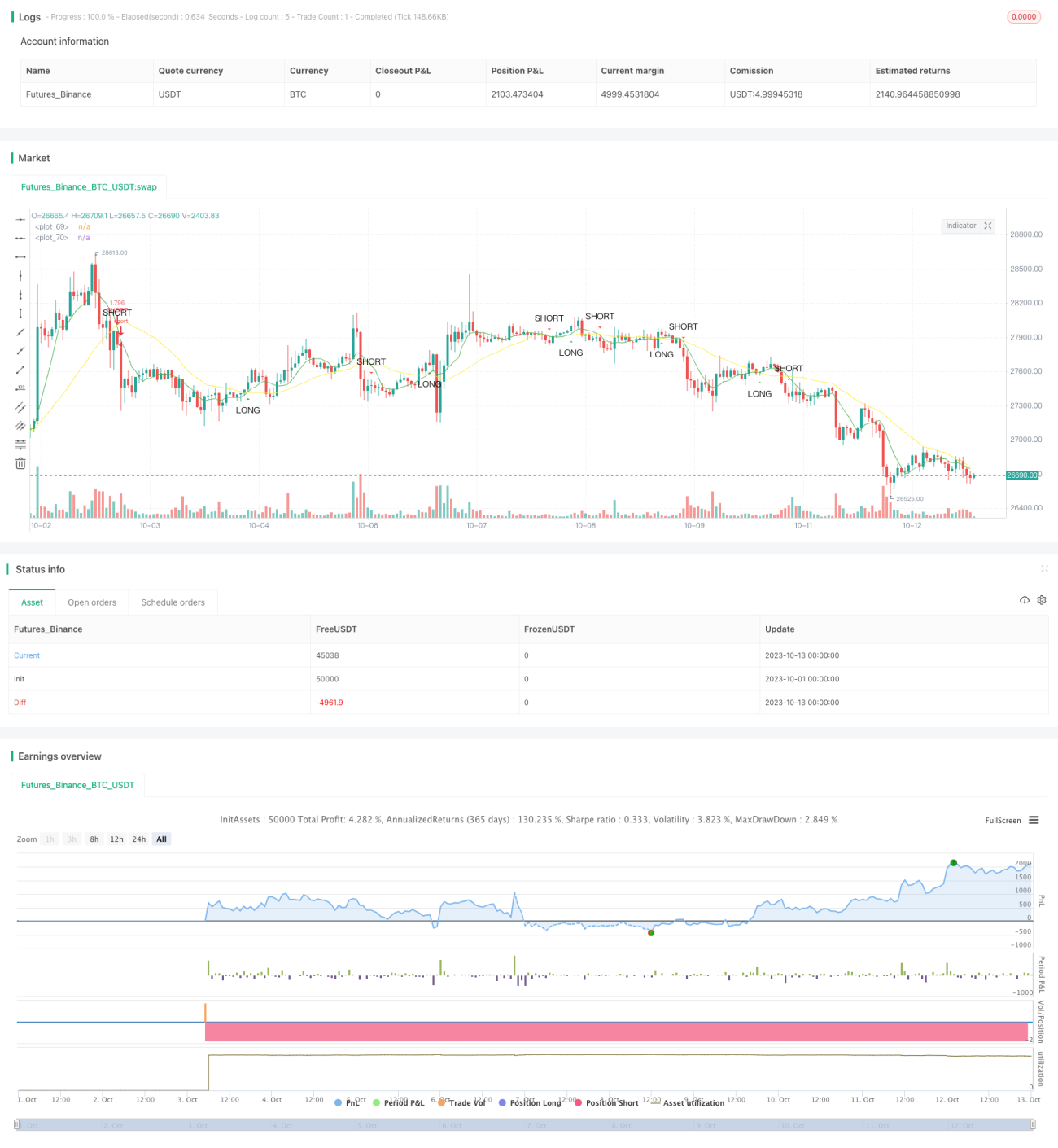

Esta estrategia genera señales de trading basándose en el principio de cruce entre una media móvil rápida y una media móvil lenta. Cuando la media móvil rápida cruza por encima de la media móvil lenta desde abajo, se genera una señal de compra; cuando la media móvil rápida cruza por debajo de la media móvil lenta desde arriba, se genera una señal de venta.

Principio

La estrategia utiliza la función sma para calcular la media móvil rápida y la media móvil lenta. fast_SMA es la media móvil rápida, con una longitud de período fast_SMA_input; slow_SMA es la media móvil lenta, con una longitud de período slow_SMA_input.

La estrategia emplea las funciones cross y crossunder para detectar los cruces entre la media móvil rápida y la lenta. Cuando la media móvil rápida cruza por encima de la media móvil lenta, la variable LONG se vuelve true, generando una señal de compra; cuando la media móvil rápida cruza por debajo de la media móvil lenta, la variable SHORT se vuelve true, generando una señal de venta.

Análisis de ventajas

Esta estrategia presenta las siguientes ventajas:

- El principio de la estrategia es simple, fácil de entender e implementar.

- Los períodos de las medias móviles son personalizables, adaptándose a diferentes entornos de mercado.

- Puede filtrar parte del ruido del mercado, generando señales de trading relativamente fiables.

- Permite capturar tanto el inicio como el cambio de tendencia.

Análisis de riesgos

Esta estrategia también presenta los siguientes riesgos:

- Si la configuración no es adecuada, puede generar demasiadas señales de trading, provocando operaciones frecuentes.

- En mercados laterales puede generar muchas señales no válidas.

- No puede determinar la duración de la tendencia, lo que podría provocar reversiones prematuras.

Métodos de control de riesgos:

- Ajustar razonablemente los parámetros de las medias móviles para equilibrar el efecto de filtrado y la sensibilidad.

- Combinar con indicadores de tendencia para filtrar señales no válidas.

- Establecer puntos de stop-loss para controlar las pérdidas por operación.

Direcciones de optimización

Esta estrategia puede optimizarse en los siguientes aspectos:

- Agregar condiciones de filtro, como verificar el volumen o indicadores de volatilidad al cruzar las medias móviles, para evitar falsos cruces.

- Combinar con indicadores de tendencia para identificar la dirección y la fuerza de la tendencia.

- Incorporar modelos de aprendizaje automático para optimizar automáticamente los parámetros de las medias móviles.

- Combinar con niveles de soporte y resistencia, Bandas de Bollinger y otros indicadores técnicos para dibujar zonas de trading, mejorando la precisión de la entrada.

Conclusión

Esta estrategia aprovecha las ventajas de las medias móviles para generar señales de trading de forma simple y efectiva. Aunque presenta algunos riesgos, se puede mejorar mediante la optimización de parámetros, la adición de filtros, etc. La estrategia de cruce de medias móviles merece más investigación y aplicación.

- 1