Estrategia de trading basada en la ruptura del histograma

Resumen

Esta estrategia utiliza el principio de ruptura del histograma, combinado con el juicio de tendencia de las medias móviles, para realizar operaciones de ruptura en la dirección de la tendencia. Cuando el precio supera el límite del histograma, se genera una señal de trading. Al mismo tiempo, se determina la dirección general de la tendencia mediante la relación de posición de las medias móviles rápidas y lentas, evitando señales falsas en rangos laterales.

Principio de la estrategia

-

Calcular la media móvil rápida (período 20) y la media móvil lenta (período 50).

-

Según las velas, determinar si se ha formado un rectángulo alcista (close>open) o un rectángulo bajista (close<open).

-

Evaluar si el rectángulo ha superado el máximo o mínimo de la vela anterior. Si es un rectángulo alcista y supera el máximo de la vela anterior, se genera una señal de ruptura larga; si es un rectángulo bajista y supera el mínimo de la vela anterior, se genera una señal de ruptura corta.

-

Al mismo tiempo, determinar si la media móvil rápida está por encima de la media móvil lenta. Si es así, se considera tendencia alcista; de lo contrario, se considera tendencia bajista.

-

Solo cuando las medias rápidas y lentas indiquen una tendencia alcista, la señal de ruptura larga es válida; solo cuando indiquen una tendencia bajista, la señal de ruptura corta es válida. Esto evita señales falsas en rangos laterales.

-

Cuando se genera una señal de ruptura larga válida, se abre una posición larga con ciertos niveles de stop loss y take profit; cuando se genera una señal de ruptura corta válida, se abre una posición corta con ciertos niveles de stop loss y take profit.

-

Si las medias móviles rápidas y lentas se cruzan en sentido inverso, se cierra la posición actual.

Análisis de ventajas

-

Utiliza el límite del histograma como punto de ruptura, lo que representa una señal de ruptura fuerte.

-

Considera la dirección de la tendencia al mismo tiempo, evitando señales falsas en rangos laterales y mejorando la precisión.

-

Combina tendencia y ruptura, lo que permite que la estrategia funcione bien en mercados con tendencia.

-

Mediante la optimización de parámetros, se puede adaptar a diferentes instrumentos y marcos temporales.

Riesgos y soluciones

-

Riesgo de ruptura fallida. La solución es seleccionar puntos de ruptura más grandes para asegurar un impulso de ruptura más fuerte.

-

Riesgo de juicio de tendencia inexacto. La solución es ajustar los parámetros de las medias móviles o agregar otros indicadores auxiliares para juzgar la tendencia.

-

Riesgo de stops demasiado ajustados que generen salidas frecuentes. La solución es ajustar dinámicamente el rango de stop loss según el instrumento y el marco temporal.

-

Riesgo de objetivos de ganancia demasiado pequeños. La solución es establecer diferentes ratios de riesgo-beneficio dinámicamente según el instrumento y el marco temporal.

Direcciones de optimización

-

En general, parámetros como los de las medias móviles, el punto de ruptura, el rango de stop loss y el ratio riesgo-beneficio deben probarse y optimizarse para cada instrumento y marco temporal, personalizando los parámetros de la estrategia.

-

Se pueden probar diferentes tipos de medias móviles (como EMA, SMA, etc.) para encontrar el indicador de media más adecuado.

-

Se pueden agregar otros indicadores auxiliares, como Momentum, para mejorar la precisión en el juicio de tendencia.

-

Se pueden utilizar métodos como el aprendizaje automático para optimizar dinámicamente varios parámetros.

-

Se puede realizar un aprendizaje estadístico sobre la tasa de éxito de las rupturas para ajustar los parámetros del punto de ruptura.

Resumen

Esta estrategia integra características de tendencia y ruptura, lo que en teoría puede filtrar una gran cantidad de señales no válidas. La clave es prestar atención a las pruebas y optimización de parámetros, personalizando la estrategia para diferentes instrumentos y marcos temporales, logrando así buenos resultados en el trading real. Además, los indicadores auxiliares y las técnicas de aprendizaje automático ofrecen direcciones para mejorar la estrategia. Mediante una optimización continua, esta estrategia puede convertirse en una estrategia de trading de ruptura de tendencia estable y confiable.

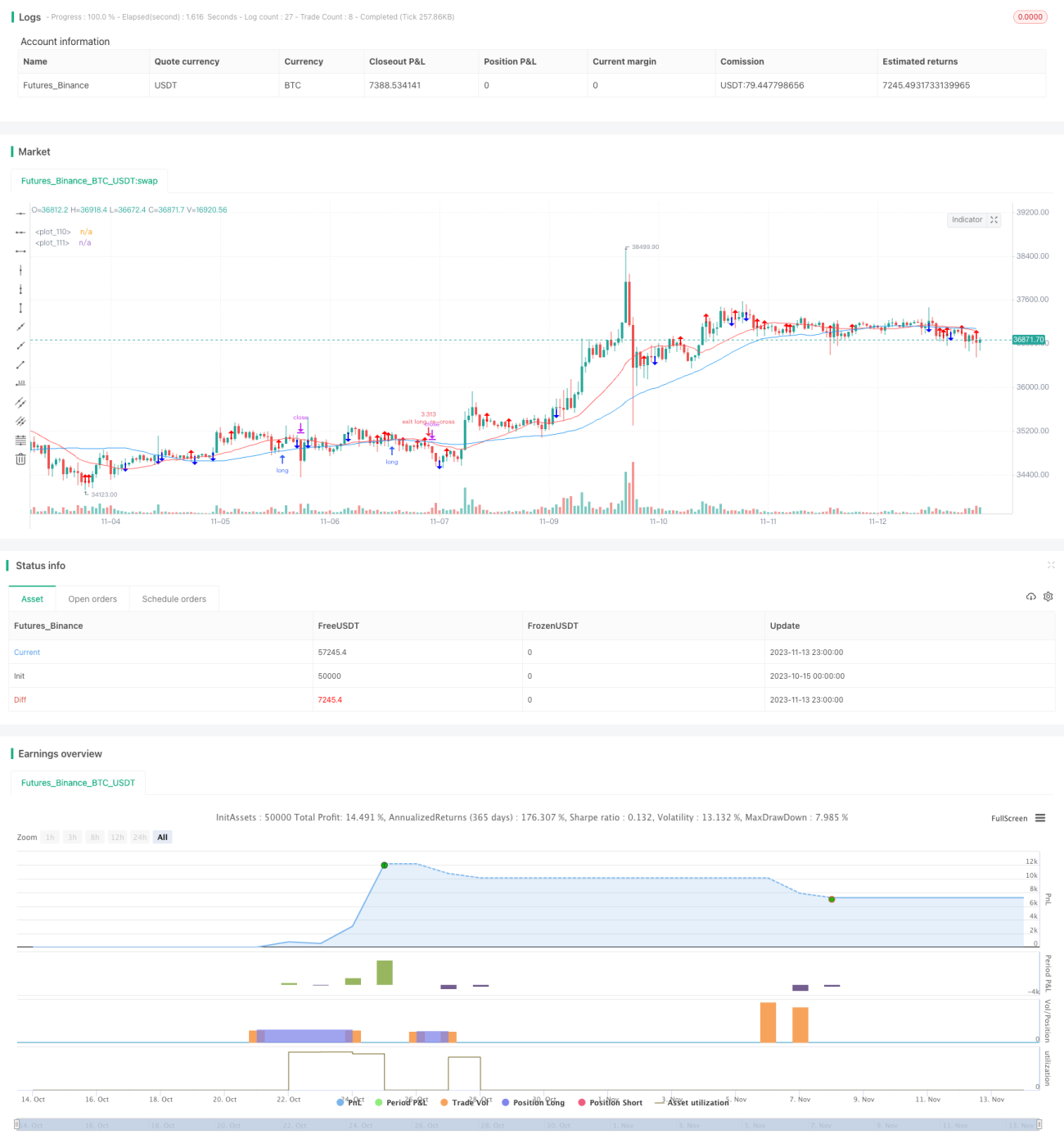

/*backtest

start: 2023-10-15 00:00:00

end: 2023-11-14 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

//Backtested Time Frame: H1

//Default Settings: Are meant to run successfully on all currency pairs to reduce over-fitting.

//Risk Warning: This is a forex trading robot, backtest performance will not equal future performance, USE AT YOUR OWN RISK.- 1