Estrategia de trading bidireccional con brechas de múltiples medias móviles

Resumen

Esta estrategia utiliza el indicador Williams High/Low para identificar señales de reversión alcista y bajista, combinado con múltiples medias móviles para operar en brechas (gap trading), y complementado con el indicador RSI para filtrar señales falsas, logrando una operativa bidireccional eficiente.

Principio de la estrategia

-

El indicador Williams High/Low utiliza los máximos y mínimos en un periodo determinado para detectar puntos de inflexión y generar señales de compra y venta.

-

Las medias móviles de 20, 50 y 100 días forman un sistema de medias múltiples. Cuando el precio supera dos de ellas, se genera una señal de operación.

-

El indicador RSI identifica zonas de sobrecompra y sobreventa, utilizándose para filtrar señales inciertas.

-

La estrategia determina qué dos medias móviles ha superado el precio y, combinando la señal del indicador Williams y el filtro del RSI, genera señales estables de compra y venta.

-

Criterio de entrada: cuando la media móvil de corto plazo cruza al alza las medias de medio y largo plazo, y al mismo tiempo se produce una señal de nuevo mínimo de Williams junto con una lectura baja del RSI, se abre una posición larga. Cuando la media móvil de corto plazo cruza a la baja las medias de medio y largo plazo, y al mismo tiempo se produce una señal de nuevo máximo de Williams junto con una lectura alta del RSI, se abre una posición corta.

-

Stop loss y take profit: se fijan niveles fijos de stop loss y take profit en porcentaje.

Ventajas de la estrategia

-

El indicador Williams identifica con precisión soportes y resistencias clave, detectando señales de reversión.

-

El cruce de múltiples medias móviles evita señales erróneas provocadas por la volatilidad de una sola media.

-

El indicador RSI ayuda a filtrar señales falsas, haciendo que los puntos de entrada sean más precisos y fiables.

-

El sistema fijo de stop loss y take profit controla el riesgo, proporcionando una relación riesgo-beneficio más clara.

-

La combinación de indicadores de reversión y tendencia proporciona una doble confirmación, haciendo que las señales de operación sean más precisas y fiables.

Riesgos de la estrategia

-

La selección inadecuada del instrumento de negociación puede requerir ajustes de parámetros según el activo.

-

Una elección incorrecta del marco temporal requiere ajustar los parámetros para cada periodo.

-

El stop loss y take profit fijos no se adaptan a los cambios del mercado, lo que puede provocar un cierre prematuro de pérdidas o una recogida de beneficios insuficiente.

-

Cuando las medias móviles oscilan lateralmente, es fácil que se generen señales erróneas.

-

Cuando los indicadores divergen, las señales pueden retrasarse.

Direcciones de optimización

-

Optimizar los parámetros dinámicamente según los diferentes instrumentos de negociación.

-

Incorporar un sistema automático de ajuste de stop loss y take profit para que la relación riesgo-beneficio sea más razonable.

-

Añadir más filtros de indicadores, como MACD, Estocástico, etc., para reducir señales falsas.

-

Incorporar algoritmos de aprendizaje automático para identificar automáticamente los mejores momentos de entrada.

-

Combinar más indicadores de tendencia para reconocer movimientos direccionales.

Conclusión

Esta estrategia utiliza de forma integral múltiples herramientas de análisis técnico, como el indicador Williams, las medias móviles y el RSI. Al reducir las señales falsas mediante una doble confirmación, captura eficazmente las oportunidades de reversión, y controla el riesgo con stops fijos. En conjunto, es una estrategia de operativa bidireccional fiable y práctica. Los próximos pasos para mejorar su rendimiento incluyen la optimización de parámetros, el ajuste de stops y take profit, y la integración de modelos.

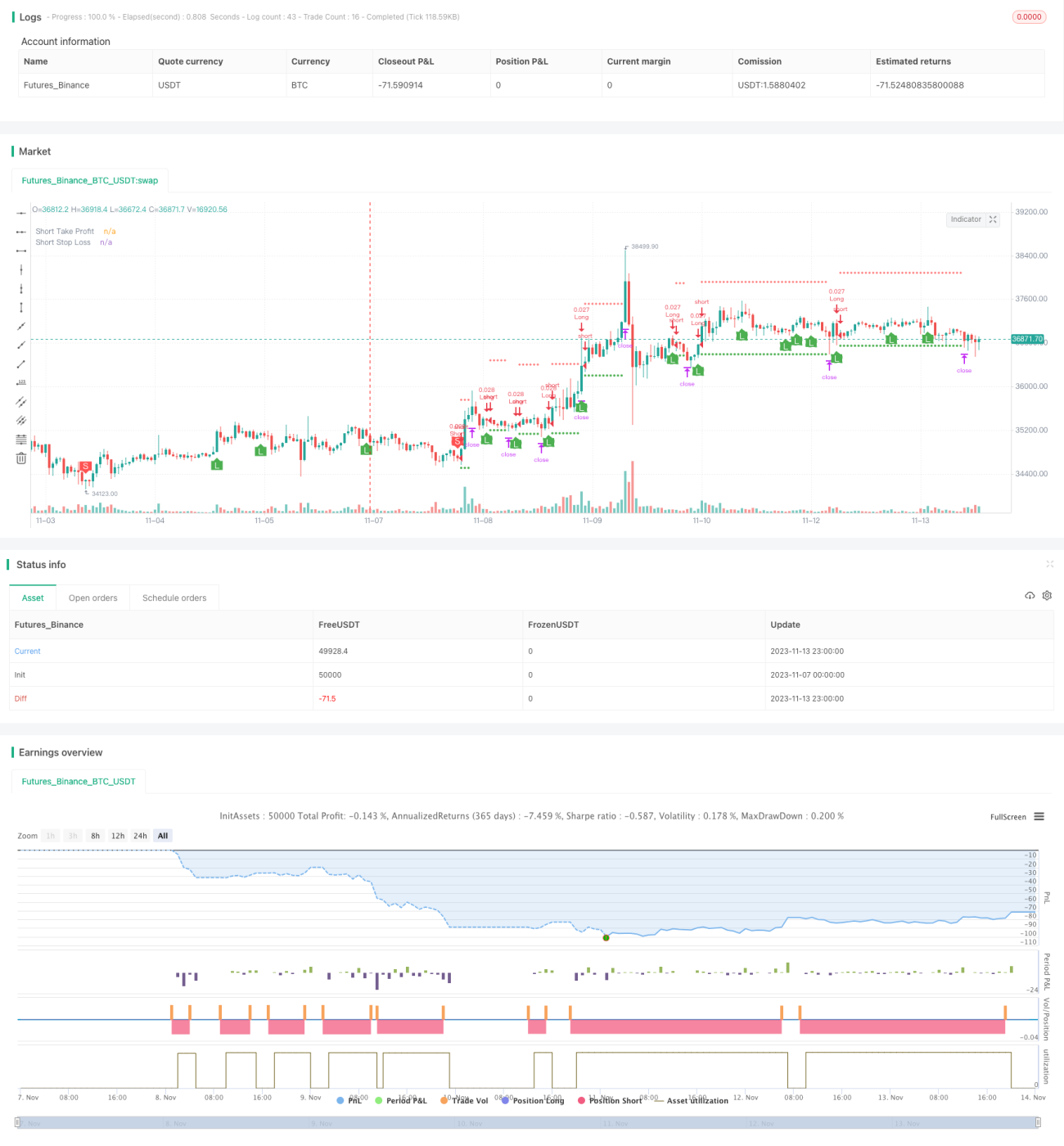

/*backtest

start: 2023-11-07 00:00:00

end: 2023-11-14 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © B_L_A_C_K_S_C_O_R_P_I_O_N

// v 1.1

- 1