Estrategia de ruptura de tendencia con filtro de doble media móvil

Resumen

Se trata de una estrategia que utiliza medias móviles y Bandas de Bollinger para determinar la tendencia, combinada con filtros de ruptura y principios de stop loss. Puede capturar señales oportunamente cuando la tendencia cambia, reduciendo señales falsas mediante el filtro de doble media móvil y estableciendo stop loss para controlar el riesgo.

Principio de la estrategia

La estrategia se compone principalmente de las siguientes partes:

-

Determinación de tendencia: Utiliza el MACD para identificar la tendencia de los precios, distinguiendo entre tendencias alcistas y bajistas.

-

Filtro de rango: Usa las Bandas de Bollinger para determinar el rango de fluctuación del precio, filtrando señales que no superan el rango.

-

Confirmación con doble media móvil: Compuesta por una EMA rápida y una EMA lenta, para confirmar la señal de tendencia. Solo cuando la EMA rápida es mayor que la EMA lenta se genera una señal de compra.

-

Mecanismo de stop loss: Establece un punto de stop loss; cuando el precio supera este punto en dirección desfavorable, se cierra la posición para limitar pérdidas.

La lógica para generar señales de entrada es la siguiente:

- El MACD indica una tendencia alcista.

- El precio supera la banda superior de Bollinger.

- La EMA rápida está por encima de la EMA lenta.

Cuando se cumplen simultáneamente estas tres condiciones, se genera una señal de compra.

La lógica de cierre de posición se divide en dos tipos: cierre por take profit y cierre por stop loss. El punto de take profit es el precio de entrada multiplicado por un cierto porcentaje, y el punto de stop loss es el precio de entrada multiplicado por otro porcentaje. Cuando el precio supera uno de estos puntos, se cierra la posición.

Análisis de ventajas

Esta estrategia presenta las siguientes ventajas:

- Captura oportunamente los cambios de tendencia, con pocos retrocesos (traceback).

- Filtra señales falsas mediante la doble media móvil, mejorando la calidad de las señales.

- El mecanismo de stop loss controla eficazmente las pérdidas por operación.

- Amplio margen de optimización de parámetros, permitiendo ajustarlos al mejor estado.

Análisis de riesgos

La estrategia también conlleva algunos riesgos:

- En mercados laterales, las señales falsas generadas pueden provocar pérdidas.

- Un ajuste inadecuado del stop loss puede ocasionar pérdidas innecesarias.

- Parámetros incorrectos pueden llevar a un rendimiento deficiente de la estrategia.

Para mitigar estos riesgos, se puede optimizar ajustando parámetros, modificando la ubicación del stop loss, entre otras mejoras.

Direcciones de optimización

La estrategia se puede optimizar desde los siguientes aspectos:

- Ajustar la longitud de las medias móviles (rápida y lenta) para encontrar la mejor combinación de parámetros.

- Probar diferentes métodos de stop loss, como stop loss dinámico (trailing stop), stop loss basado en volatilidad, etc.

- Probar distintos parámetros del MACD para encontrar los valores óptimos.

- Utilizar aprendizaje automático para la optimización automática de parámetros.

- Añadir condiciones adicionales para filtrar señales.

Mediante pruebas con diferentes configuraciones de parámetros y evaluando la rentabilidad y el ratio de Sharpe, se puede encontrar el estado óptimo de esta estrategia.

Conclusión

Se trata de una estrategia cuantitativa que combina determinación de tendencia, filtro de rango, confirmación con doble media móvil y stop loss. Es capaz de identificar eficazmente la dirección de la tendencia, encontrando un equilibrio entre la maximización de beneficios y el control de riesgos. A través de la optimización de parámetros y el aprendizaje automático, esta estrategia aún tiene un gran potencial de mejora para obtener mejores resultados.

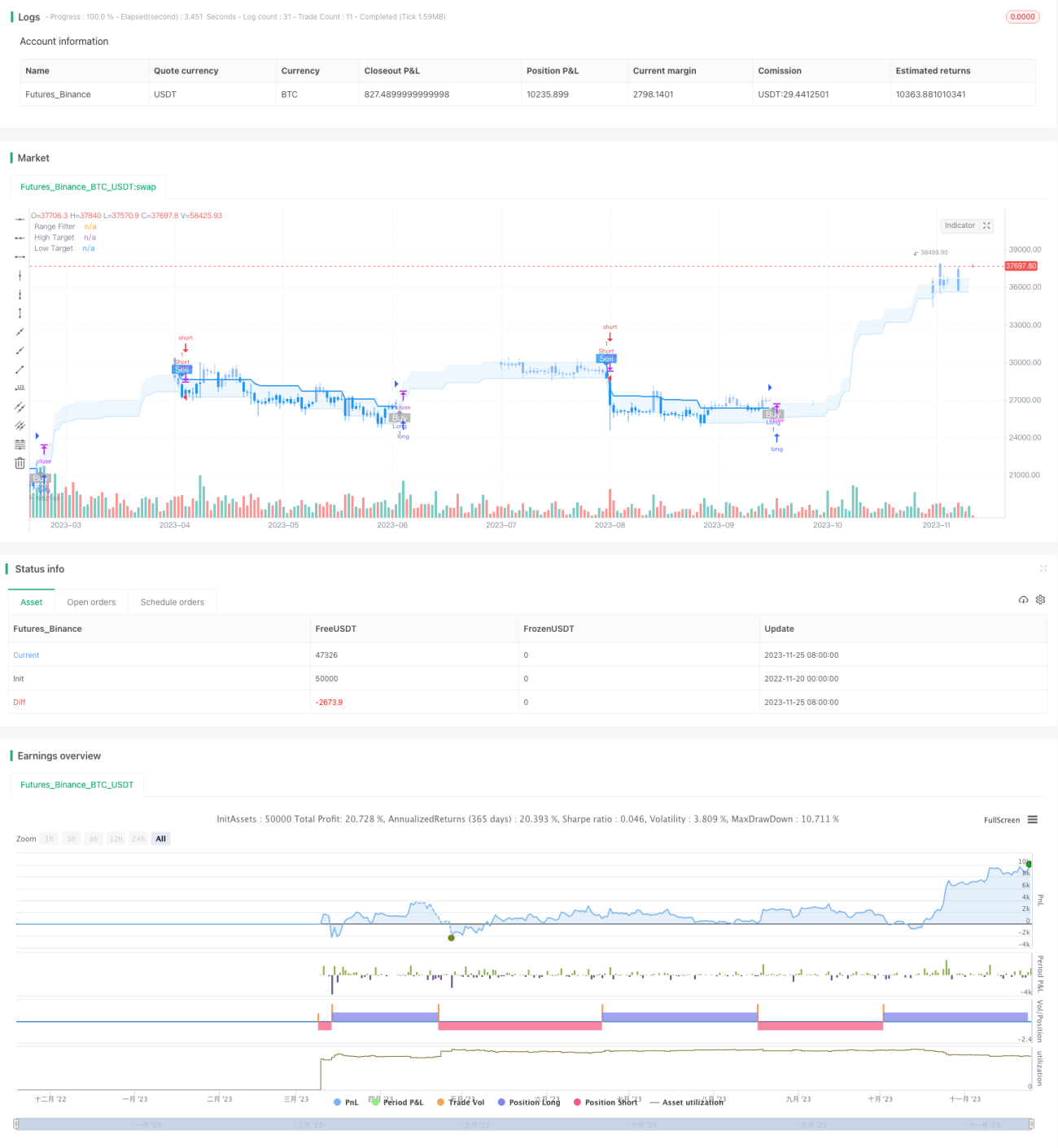

/*backtest

start: 2022-11-20 00:00:00

end: 2023-11-26 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

strategy(title="Range Filter Buy and Sell Strategies", shorttitle="Range Filter Strategies", overlay=true,pyramiding = 5)

// Original Script > @DonovanWall- 1