Estrategia de trading de volatilidad adaptativa basada en ruptura de precios

Resumen

Esta estrategia identifica las tendencias del mercado basándose en puntos de ruptura de precios, y combina indicadores adaptativos para juzgar la tendencia general, con el fin de capturar oportunidades de reversión de precios a corto plazo. Cuando el precio supera el canal de ruptura de referencia, se generan señales de compra/venta. Esta estrategia es adecuada para el comercio de criptomonedas de alta volatilidad.

Principio de la estrategia

- Identificar los puntos extremos de precio como límites del canal. Cuando el precio alcanza un nuevo máximo o mínimo, se toma ese punto como límite del canal.

- Calcular el indicador de volatilidad adaptativa MA para determinar la dirección general de la tendencia. Cuanto mayor sea el valor de MA, más indica que se encuentra en una fase de oscilación.

- Cuando el precio supera al alza el borde superior del canal, se genera una señal de compra; cuando el precio supera a la baja el borde inferior del canal, se genera una señal de venta.

- Establecer un stop loss. El stop loss para posiciones largas se establece en el 1% del precio de entrada.

Análisis de ventajas

- El canal de precios es adaptativo, lo que permite identificar con precisión los puntos de inflexión de la tendencia.

- El indicador de volatilidad juzga la tendencia general, evitando perder la dirección principal durante las oscilaciones.

- Es una estrategia de reversión, adecuada para capturar rebotes de precios a corto plazo.

Análisis de riesgos

- En mercados con caídas continuas y significativas, es fácil activar múltiples stops, lo que genera grandes pérdidas.

- Durante la consolidación oscilante, las compras y ventas frecuentes aumentan los costos de negociación.

- Se requiere determinar manualmente el momento de entrada, y la negociación totalmente automatizada tiene riesgo de sobreajuste.

Direcciones de optimización

- Optimizar los parámetros del MA para que juzgue mejor la tendencia general.

- Agregar indicadores de volumen para evitar señales de reversión con volumen agotado.

- Agregar modelos de aprendizaje automático para lograr una optimización dinámica de los parámetros.

Resumen

La idea general de esta estrategia es clara y tiene cierto valor práctico. Sin embargo, aún es necesario prestar atención al control del riesgo de negociación para evitar pérdidas significativas en condiciones específicas del mercado. El siguiente paso puede optimizar desde múltiples dimensiones como el marco general, los parámetros de los indicadores y el control de riesgos, para que los parámetros de la estrategia y las señales de negociación sean más confiables.

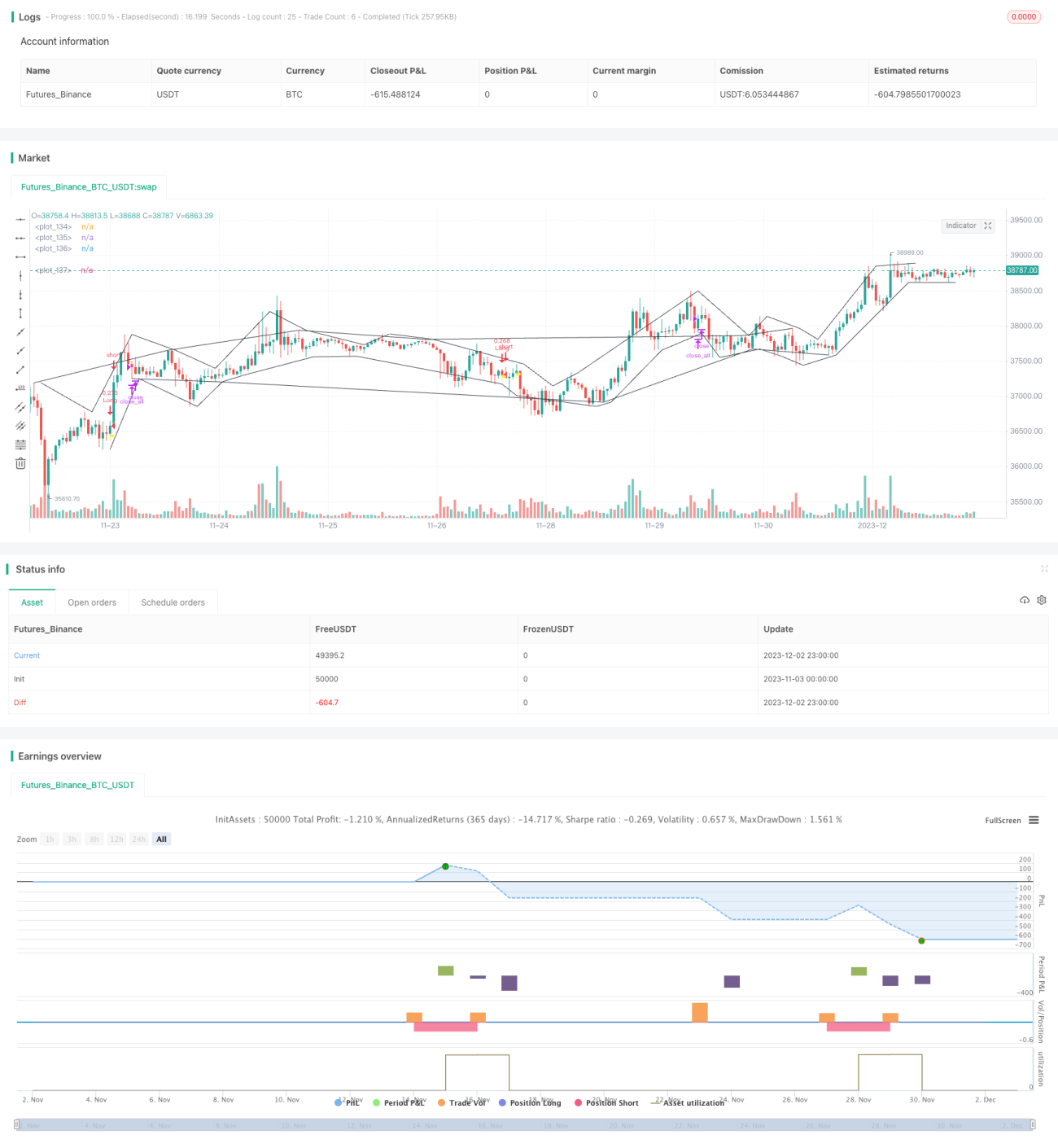

/*backtest

start: 2023-11-03 00:00:00

end: 2023-12-03 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// @version = 4

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © TradingGroundhog

- 1