Estrategia de reversión RSI multifactorial

Resumen

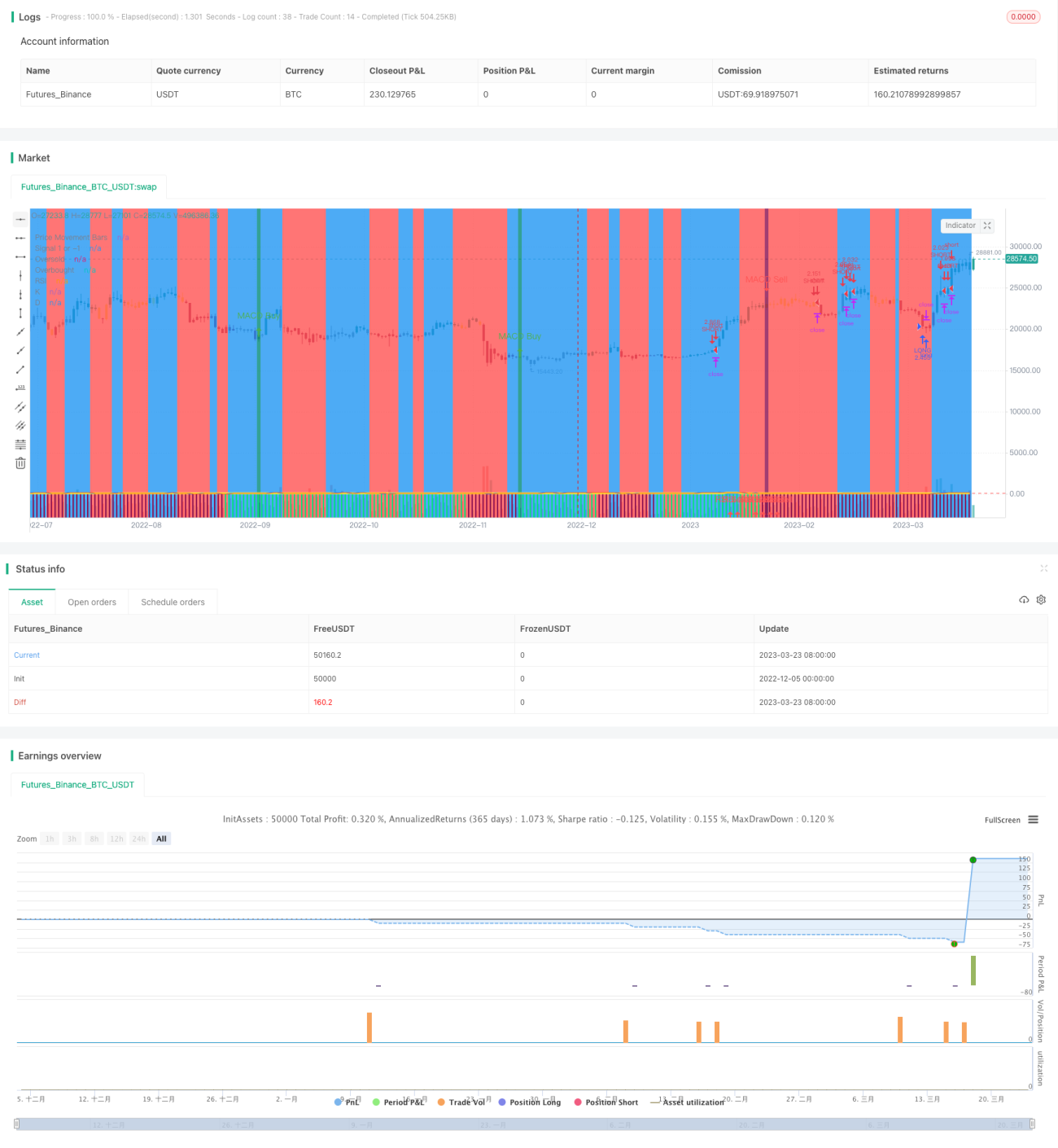

Esta estrategia utiliza el indicador RSI para identificar condiciones de sobrecompra y sobreventa, combinándolo con múltiples factores auxiliares como MACD y el indicador estocástico para las entradas. La estrategia busca capturar oportunidades de reversión a corto plazo, siendo una estrategia de reversión.

Principio de la estrategia

La estrategia utiliza principalmente el indicador RSI para determinar si el mercado se encuentra en estado de sobrecompra o sobreventa. Cuando el RSI supera el nivel de sobrecompra establecido, indica que el mercado podría estar sobrecomprado, y la estrategia opta por vender en corto. Cuando el RSI cae por debajo del nivel de sobreventa establecido, indica que el mercado podría estar sobrevendido, y la estrategia opta por comprar. De esta manera, se aprovechan las oportunidades de trading a corto plazo generadas durante el proceso de reversión en el que el mercado pasa de un estado extremo a otro.

Además, la estrategia incorpora varios factores auxiliares como MACD y el indicador estocástico. La función de estos factores auxiliares es filtrar posibles señales de trading falsas positivas. Solo cuando el RSI emite una señal y los factores auxiliares también la respaldan, la estrategia toma una acción de trading real. Esta combinación de múltiples factores mejora la fiabilidad de las señales de la estrategia, aumentando así su estabilidad.

Análisis de ventajas

La mayor ventaja de esta estrategia radica en su alta eficiencia de captura y la verificación multifactorial que mejora la calidad de las señales. Específicamente, se refleja en los siguientes aspectos:

- El indicador RSI tiene una fuerte capacidad para identificar regímenes de mercado, pudiendo detectar eficazmente condiciones de sobrecompra y sobreventa.

- El uso de múltiples herramientas auxiliares para la verificación multifactorial mejora la calidad de las señales y filtra una gran cantidad de falsos positivos.

- La estrategia es poco sensible a los parámetros, lo que facilita su optimización.

Riesgos y soluciones

Esta estrategia también enfrenta ciertos riesgos, principalmente en dos aspectos:

- Riesgo de fallo en la reversión. La señal de reversión en sí misma se basa en oportunidades de arbitraje estadístico, y no se descarta la probabilidad de que algunas reversiones fallen. Se puede controlar el riesgo reduciendo el tamaño de la posición o estableciendo stop-loss.

- Riesgo de pérdidas en mercados alcistas. La estrategia opera principalmente en contra de la tendencia dominante, por lo que es inevitable que sufra pérdidas en mercados alcistas. Esto requiere un juicio preciso de la tendencia general y, si es necesario, intervenir manualmente para saltarse condiciones de mercado desfavorables.

Direcciones de optimización

Esta estrategia necesita ser optimizada en los siguientes aspectos:

- Probar diferentes activos para encontrar la mejor combinación de parámetros. Aunque la estrategia no es muy sensible a los parámetros, se recomienda buscar los parámetros óptimos para cada activo.

- Incorporar un mecanismo de salida adaptativo. Se pueden probar métodos como el stop-loss dinámico o la salida por tiempo para que la estrategia se adapte mejor a los cambios del mercado.

- Introducir algoritmos de aprendizaje automático. Se puede intentar que el modelo aprenda a estimar la probabilidad de éxito de una reversión, mejorando así la tasa de aciertos de la estrategia.

Conclusión

En general, esta estrategia es una estrategia de reversión a corto plazo. Utiliza la capacidad del indicador RSI para identificar condiciones de sobrecompra y sobreventa, y emplea múltiples herramientas auxiliares para la verificación multifactorial, mejorando así la calidad de las señales. La estrategia tiene una alta eficiencia de captura y una buena estabilidad. Merece la pena probarla y optimizarla aún más para lograr finalmente la rentabilidad.

/*backtest

start: 2022-12-05 00:00:00

end: 2023-03-24 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

//@version=4

strategy(shorttitle='Ain1',title='All in One Strategy', overlay=true, initial_capital = 1000, process_orders_on_close=true, default_qty_type = strategy.percent_of_equity, default_qty_value = 100, commission_type=strategy.commission.percent, commission_value=0.18, calc_on_every_tick=true)- 1