Estrategia cuantitativa de líneas de distracción entrelazadas diarias

Resumen

La estrategia cuantitativa de líneas de distracción envolventes diarias es una estrategia de trading cuantitativo a corto plazo basada en medias móviles e indicadores de precio máximo y mínimo. Utiliza las flechas EXIT del indicador mixto SSL para determinar puntos de compra y venta, combinado con el indicador QQE como filtro, y emplea el indicador ATR para calcular niveles de stop-loss y posiciones de scaling-in por lotes. Esta estrategia es adecuada para inversores sensibles a la volatilidad del mercado y con un estricto control de riesgos.

Principio de la estrategia

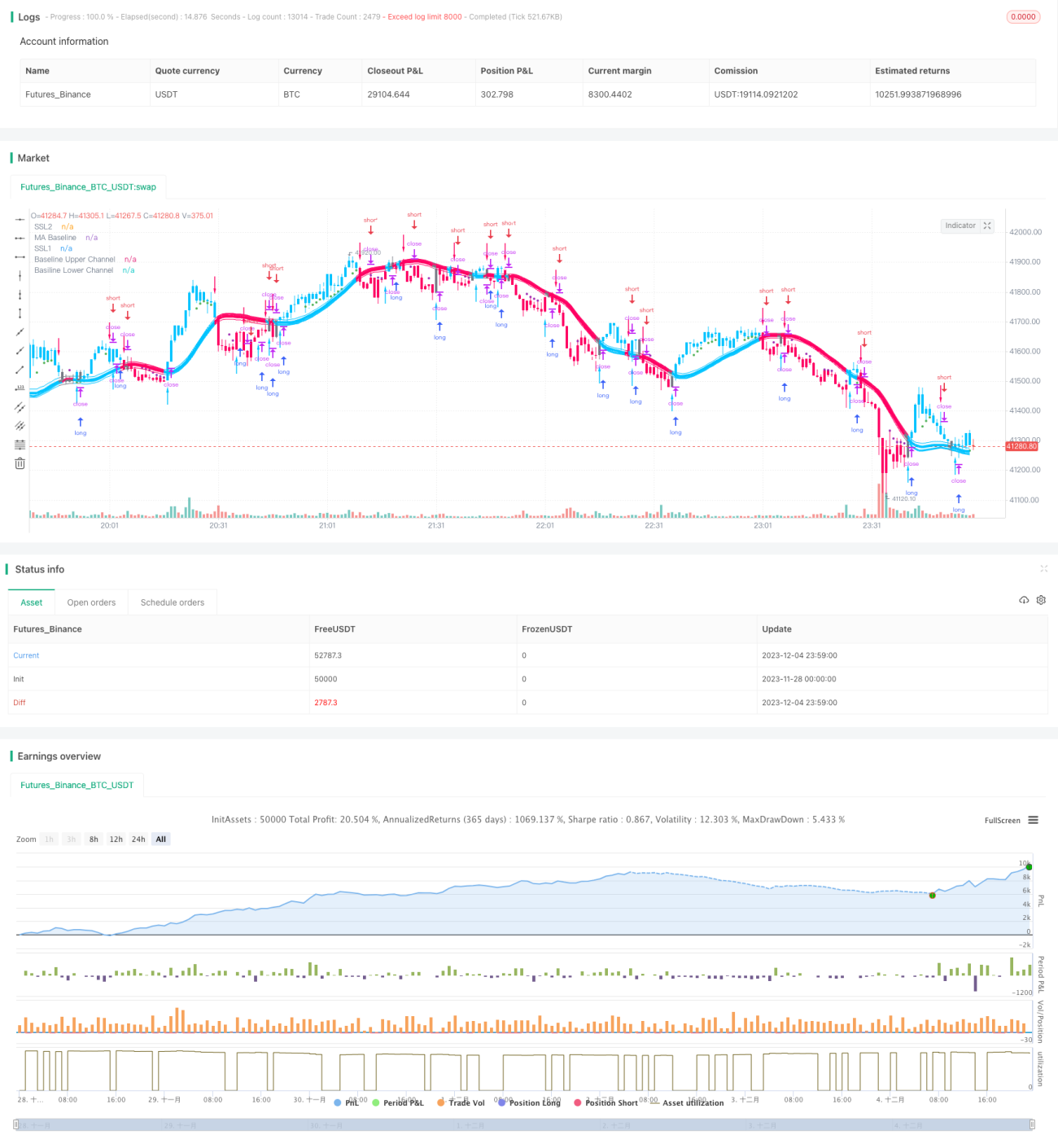

La estrategia utiliza las flechas EXIT del indicador mixto SSL para determinar los puntos de entrada y salida. Por encima de la flecha EXIT está el punto alto de EXIT, y por debajo está el punto bajo de EXIT. Cuando el precio de cierre cruza hacia abajo desde el punto alto de EXIT, se genera una señal de venta; cuando el precio de cierre cruza hacia arriba desde el punto bajo de EXIT, se genera una señal de compra.

Para mejorar la fiabilidad de las señales, la estrategia introduce el indicador QQE como condición de filtro auxiliar. Las señales generadas por la flecha EXIT solo se ejecutan cuando el indicador QQE está en la misma dirección.

Para controlar el riesgo, la estrategia utiliza el indicador ATR con un multiplicador para calcular los niveles de stop-loss y de scaling-in por lotes. El stop-loss para posiciones cortas es precio de cierre + ATR × 1.8; el stop-loss para posiciones largas es precio de cierre - ATR × 1.8. El scaling-in se realiza en tres lotes, cada lote con un monto del 10% del capital inicial, y los niveles de scaling-in son precio de cierre - ATR × 0.1, precio de cierre - ATR × 0.3 y precio de cierre - ATR × 0.7.

Cada lote de scaling-in tiene su propio stop-loss. El 20% del capital del primer lote se detiene en pérdidas al alcanzar el nivel de stop-loss, mientras que el resto de la posición continúa manteniéndose.

Ventajas de la estrategia

- Obtener ganancias mediante las flechas EXIT y detener pérdidas a tiempo, controlando eficazmente el riesgo.

- El filtro del indicador QQE mejora la precisión de las señales.

- El uso del indicador ATR para calcular stop-loss y niveles de scaling-in según la volatilidad del mercado permite un control de riesgos más preciso.

- El scaling-in por lotes permite aprovechar al máximo las tendencias para obtener ganancias.

Riesgos de la estrategia

- Si una posición rentable alcanza un stop-loss parcial, las posiciones restantes pueden enfrentar el riesgo de detenerse en pérdidas. Se puede considerar un take-profit general o un take-profit basado en los fundamentos del activo subyacente.

- Las flechas EXIT y el indicador QQE tienen diferente sensibilidad a la volatilidad del mercado, lo que puede generar señales contradictorias. Se deben ajustar los parámetros para reducir conflictos de señales.

- Un scaling-in demasiado agresivo puede llevar a comprar en techos y vender en suelos. Se debe evaluar la situación y reducir el apalancamiento.

Direcciones de optimización

- Combinar indicadores fundamentales del activo subyacente para el take-profit, como establecer niveles razonables de take-profit basados en la relación precio/valor contable, la relación precio/beneficio y la tasa de dividendos.

- Ajustar los parámetros del indicador QQE para que coincidan con las señales generadas por las flechas EXIT.

- Reducir la proporción de scaling-in según el calor del mercado, disminuyendo el scaling-in en mercados laterales.

- Probar la mejor combinación de parámetros basándose en indicadores como la máxima reducción y la relación ganancia/pérdida.

Resumen

Esta estrategia tiene como núcleo las flechas EXIT del indicador mixto SSL, utilizando los indicadores QQE y ATR para filtrar y detener pérdidas. Mediante el scaling-in por lotes se amplifican las ganancias. Es una estrategia cuantitativa a corto plazo, adecuada para seguir las tendencias a corto plazo del mercado. La estrategia cuenta con capacidad de control de reducciones y gestión de riesgos, pero también hay que prestar atención a riesgos como conflictos de señales y comprar en techos/vender en suelos. Si se combina con métodos de take-profit basados en fundamentos y se es más prudente al evaluar la lateralidad del mercado y ajustar la proporción de scaling-in, el potencial de ganancias de la estrategia será mayor.

- 1