Estrategia cuantitativa basada en la tasa de cambio de precio y la media móvil

Resumen

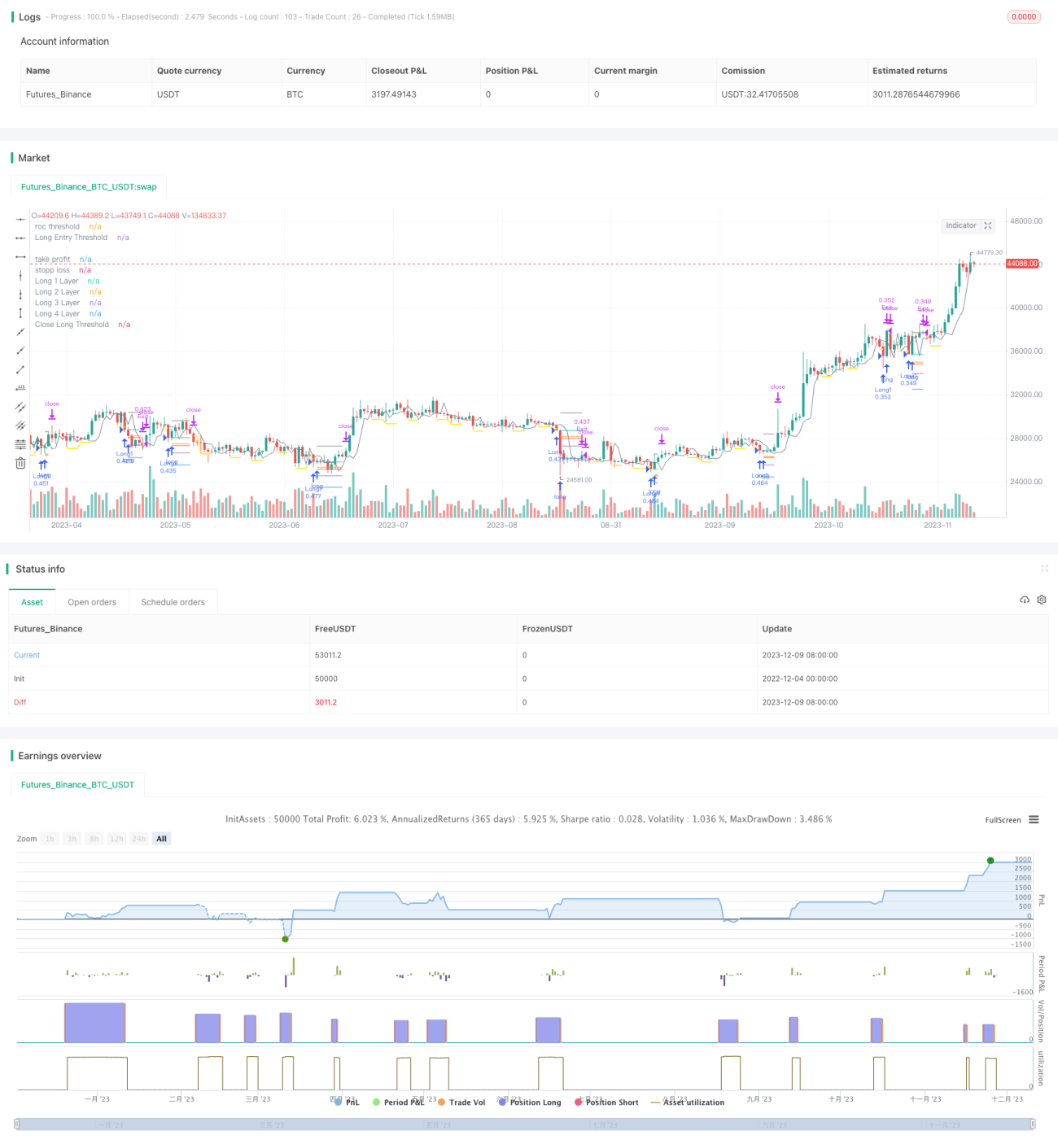

Esta estrategia combina indicadores técnicos de tasa de cambio de precio y medias móviles para lograr una localización precisa de puntos de compra y venta. Cuando el precio experimenta una caída significativa, se establece un umbral de compra, y al caer aún más, se abre una posición larga; cuando el precio sube, se establece un umbral de venta, y al continuar subiendo, se cierra la posición. Además, la estrategia emplea un método de acumulación de posiciones, comprando en múltiples ocasiones para reducir el costo.

Principio de la Estrategia

Lógica de Compra

- Calcular la tasa de cambio de precio (ROC) y definir la línea de umbral de compra.

- Cuando el precio rompe por debajo de la línea de umbral de compra, se registra ese punto y se activa la línea de limitación de compra.

- La línea de limitación de compra tiene una duración definida según los parámetros de entrada, y se cierra después de que expire.

- Cuando el precio continúa cayendo y rompe por debajo de la línea de limitación de compra, se abre la primera posición larga.

Lógica de Venta

- Calcular la tasa de cambio de precio (ROC) y definir la línea de umbral de venta.

- Cuando el precio supera la línea de umbral de venta, se registra ese punto y se activa la línea de limitación de venta.

- La línea de limitación de venta tiene una duración definida según los parámetros de entrada, y se cierra después de que expire.

- Cuando el precio continúa subiendo y supera la línea de limitación de venta, se cierran todas las posiciones largas.

Control de Riesgos

La estrategia incorpora funciones de stop loss y take profit, con parámetros personalizables para controlar en tiempo real el riesgo de las posiciones abiertas.

Método de Acumulación de Posiciones

Cada vez que se abre una posición de trading, se establece un precio de compra posterior en una proporción determinada según los parámetros de entrada, logrando así un efecto de acumulación de posiciones mediante compras escalonadas.

Análisis de Ventajas

- Utiliza el indicador de tasa de cambio de precio (ROC) para localizar puntos de compra y venta; el ROC es muy sensible a los cambios de precio, logrando una localización precisa.

- Emplea la línea de limitación para confirmar aún más el momento de la operación, evitando falsas rupturas.

- El método de acumulación de posiciones permite seguir el valor de mercado mientras se mantiene el riesgo controlado.

- Las funciones integradas de stop loss y take profit controlan estrictamente el riesgo por posición individual.

Riesgos y Soluciones

- Cuando el mercado experimenta una volatilidad extrema, la estrategia podría abrir demasiadas posiciones. La solución es configurar adecuadamente los parámetros de acumulación de posiciones y controlar el número total de posiciones.

- Cuando la tendencia del precio es incierta y oscilante, los niveles de stop loss o take profit pueden activarse con frecuencia. Se puede ampliar ligeramente el margen de stop loss y take profit, o desactivar esta función.

Sugerencias de Optimización

- Combinar con otros indicadores para filtrar los momentos de entrada. Por ejemplo, junto con medias móviles, solo tomar la señal del ROC cuando el precio esté por debajo de la media móvil.

- Optimizar la lógica de acumulación de posiciones, activándola solo bajo ciertas condiciones. Por ejemplo, continuar acumulando solo cuando el precio vuelva a caer por debajo de un cierto porcentaje.

- La configuración de parámetros puede variar significativamente entre diferentes activos; se requieren suficientes pruebas retrospectivas y simulaciones en vivo para obtener la mejor combinación de parámetros.

- Se puede implementar un stop loss y take profit adaptativos, estableciendo diferentes niveles de stop loss según el grado de volatilidad del mercado.

Conclusión

Esta estrategia utiliza de manera integral el indicador ROC para localizar con precisión los puntos de compra y venta, la línea de limitación para filtrar señales, el stop loss y take profit incorporados para prevenir riesgos, y la acumulación de posiciones para ampliar las ganancias. Con una configuración de parámetros razonable, puede obtener rendimientos excesivos mientras mantiene el riesgo controlado. En el futuro, se puede optimizar aún más el filtrado de señales y los mecanismos de control de riesgos para que la estrategia se adapte a más entornos de mercado.

- 1