Estrategia de reversión del mínimo

1

Follow

1802

Followers

Resumen

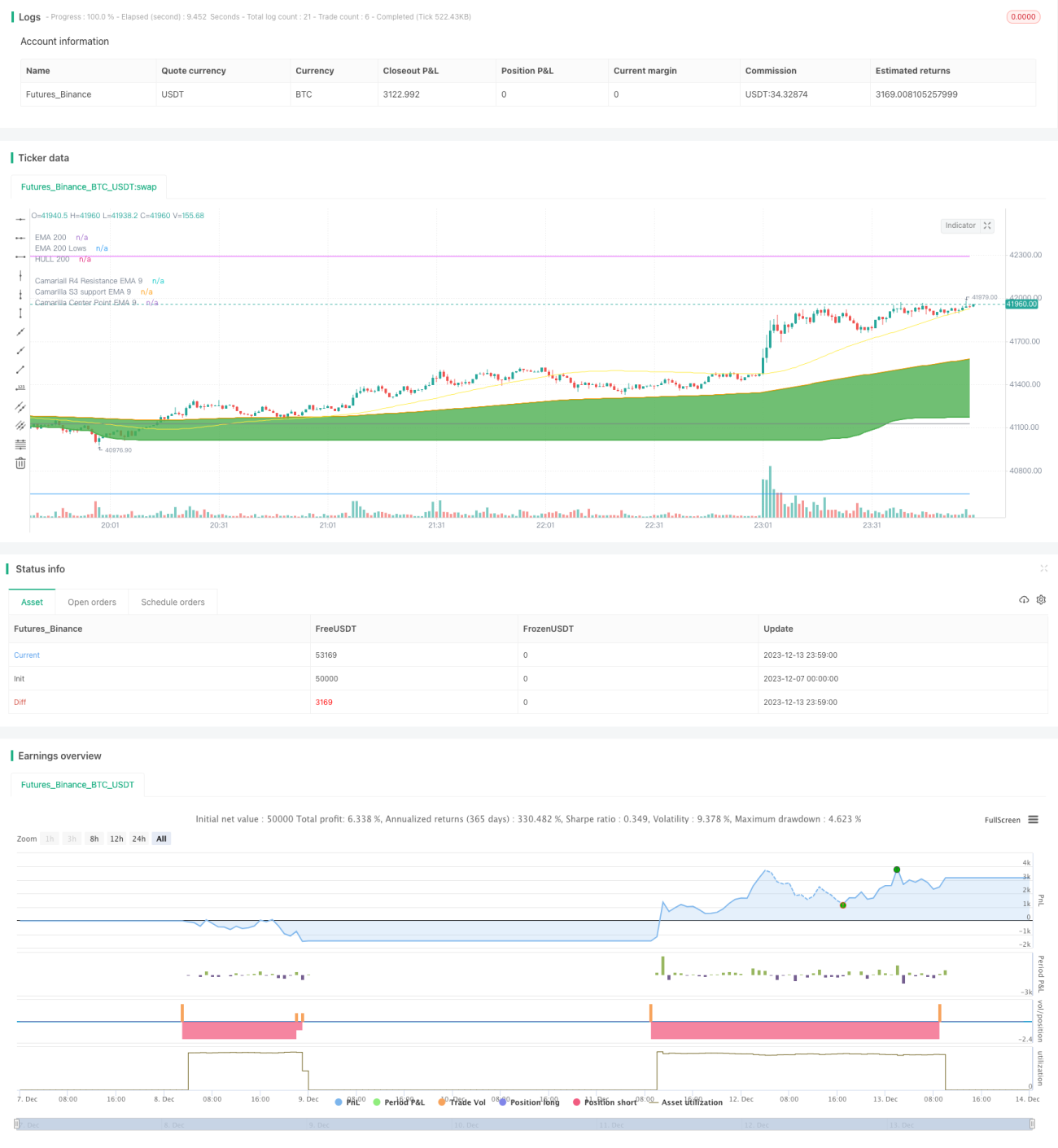

Esta estrategia se basa en operaciones de reversión en el punto más bajo del mercado. Utiliza el mínimo de la EMA de 200 días, combinado con los niveles de soporte y resistencia de Camarilla para identificar el punto más bajo del mercado, y realiza operaciones de compra cuando el precio rebota.

Principio de la estrategia

- Calcula el mínimo de la EMA de 200 días (EMA200Lows). Cuando el precio de cierre está por debajo de esta EMA, se considera que se encuentra cerca del punto más bajo del mercado.

- Calcula la EMA de 9 días del soporte 3 de Camarilla (S3), denominada ema_s3_9, como un nivel de soporte importante.

- Luego calcula la EMA de 9 días del pivote de Camarilla, denominada ema_center_9, como señal de reversión.

- Cuando ema_center_9 cruza por encima de ema200Lows, y las 3 velas anteriores están todas por debajo de ema200Lows, se realiza una operación de compra.

- El stop loss se basa en ATR, y se mueve siguiendo el mínimo del precio.

- Los objetivos de beneficio son ema_h4_9 (resistencia 4 de Camarilla) y ema_s3_9 (soporte 3 de Camarilla).

Análisis de ventajas

- Utiliza el mínimo de la EMA de 200 días para identificar la zona más baja del mercado, evitando que aparezcan mínimos más bajos durante el proceso.

- La combinación del soporte de Camarilla con el pivote permite identificar con mayor precisión los puntos de reversión.

- El stop loss basado en ATR hace que la gestión de pérdidas sea más razonable, y el seguimiento del mínimo ayuda a asegurar mayores ganancias.

Análisis de riesgos

- El riesgo de mantener posiciones a largo plazo es alto. Esta estrategia es más adecuada para operaciones de corto plazo.

- En condiciones de mercado de gran volatilidad, el stop loss puede ser amplio. Se puede ajustar según los parámetros del ATR.

- La identificación de reversiones mediante Camarilla no es 100% fiable, pudiendo producirse falsas señales.

Direcciones de optimización

- Se puede considerar combinar otros indicadores, como el RSI, para identificar señales de reversión.

- Se puede investigar el ajuste de parámetros para diferentes activos, buscando parámetros más óptimos.

- Se puede intentar utilizar métodos de aprendizaje automático para ajustar dinámicamente el stop loss basado en ATR.

Conclusión

Esta estrategia utiliza el mínimo de la EMA y los indicadores de Camarilla para identificar la zona más baja del mercado y los puntos de reversión. Obtiene ganancias mediante un stop loss basado en ATR. En general, la estrategia es completa y tiene cierto valor práctico. Mediante optimizaciones posteriores, se puede hacer que la estrategia sea más estable y fiable.

Source

Pine

/*backtest

start: 2023-12-07 00:00:00

end: 2023-12-14 00:00:00

period: 1m

basePeriod: 1m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © mohanee

//Using the lowest of low of ema200, you can find the bottomStrategy parameters

Related strategies

Comment

All comments (0)

No data

- 1