Estrategia de trading cuantitativo con MACD inverso de doble canal

Resumen

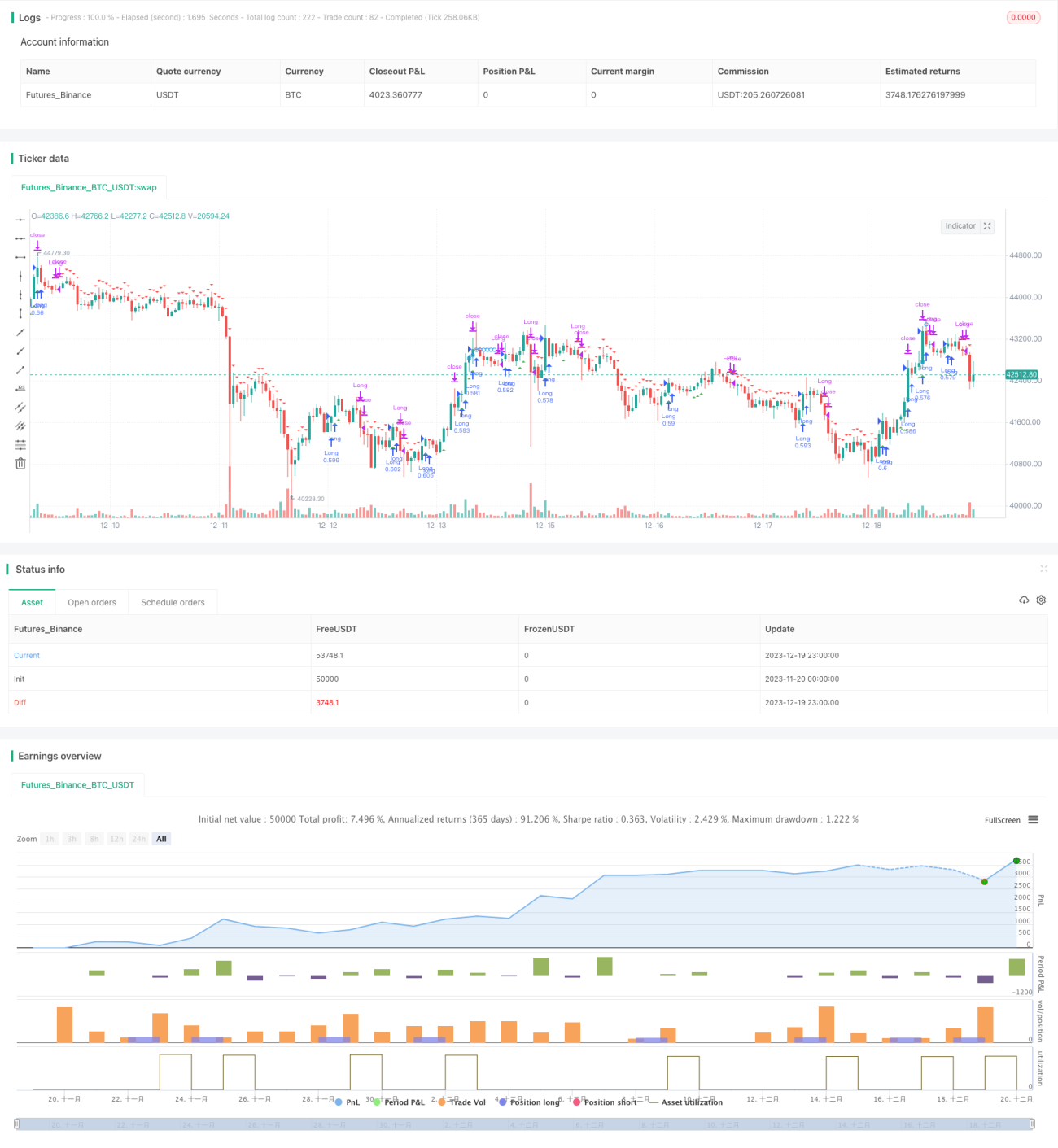

Esta estrategia es una estrategia cuantitativa de trading basada en el MACD inverso de doble banda. Toma como referencia los indicadores técnicos descritos por William Blau en su libro Momentum, Direction and Divergence y los amplía. La estrategia incluye capacidades de backtesting y se pueden añadir funciones adicionales como alertas, filtros y trailing stop.

Principio de la estrategia

El indicador central de la estrategia es el MACD. Calcula la media móvil rápida EMA(r) y la media móvil lenta EMA(slowMALen), luego calcula su diferencia xmacd. Además, calcula la EMA(signalLength) de xmacd para obtener xMA_MACD. Cuando xmacd cruza por encima de xMA_MACD, se abre una posición larga; cuando cruza por debajo, se abre una posición corta. La clave de la estrategia radica en las señales de trading inversas: la relación entre xmacd y xMA_MACD es opuesta a la del MACD convencional, de ahí el nombre "MACD inverso".

Además, la estrategia incorpora un filtro de tendencia. Al activarse una señal larga, si se ha configurado un filtro de tendencia alcista, se comprueba si el precio está subiendo; de manera similar, las señales cortas verifican una tendencia bajista. Los indicadores RSI y MFI también pueden usarse para filtrar señales. Se configura un mecanismo de stop loss para evitar pérdidas que superen un umbral determinado.

Análisis de ventajas

La mayor ventaja de esta estrategia es su potente función de backtesting. Permite seleccionar diferentes instrumentos de trading, establecer el rango temporal del backtest y optimizar la estrategia con datos específicos de cada activo. En comparación con una estrategia MACD simple, añade juicios sobre tendencias y condiciones de sobrecompra/sobreventa, lo que puede filtrar señales redundantes. El MACD inverso de doble banda difiere del MACD tradicional, lo que permite capturar oportunidades que el MACD clásico podría pasar por alto.

Análisis de riesgos

El riesgo principal de esta estrategia proviene del enfoque de trading inverso. Aunque las señales inversas pueden aprovechar ciertas oportunidades, también implican renunciar a algunos puntos de entrada y salida del MACD tradicional, lo que requiere una evaluación cuidadosa. Además, el MACD en sí mismo tiende a generar señales falsas en mercados laterales. Si se enfrenta a un mercado oscilante, la estrategia podría generar demasiadas operaciones, aumentando los costos de transacción y el deslizamiento.

Para reducir el riesgo, se pueden ajustar los parámetros, optimizar las longitudes de las medias móviles, combinar filtros de tendencia e indicadores para evitar señales en mercados laterales, y aumentar adecuadamente la distancia del stop loss para controlar las pérdidas de operaciones individuales.

Direcciones de optimización

La estrategia se puede optimizar en los siguientes aspectos:

- Ajustar los parámetros de las bandas rápidas y lentas, optimizar las longitudes de las medias móviles, probar con datos de activos específicos para encontrar la mejor combinación de parámetros.

- Añadir o ajustar filtros de tendencia, y evaluar en función de los resultados del backtest si mejoran la rentabilidad de la estrategia.

- Probar diferentes mecanismos de stop loss, determinando si es mejor un stop fijo o un trailing stop.

- Intentar combinar otros indicadores, como KD, Bandas de Bollinger, etc., para establecer más condiciones de filtro y garantizar la calidad de las señales.

Conclusión

La estrategia cuantitativa de MACD inverso de doble banda toma prestada la idea del indicador MACD clásico y la expande y mejora. La estrategia cuenta con ventajas como una configuración flexible de parámetros, una rica selección de mecanismos de filtro y una potente función de backtesting. Esto permite una optimización personalizada para diferentes instrumentos de trading, lo que la convierte en una estrategia cuantitativa prometedora y digna de exploración.

/*backtest

start: 2023-11-20 00:00:00

end: 2023-12-20 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version = 3

////////////////////////////////////////////////////////////

// Copyright by HPotter v1.0 09/12/2016

// This is one of the techniques described by William Blau in his book- 1