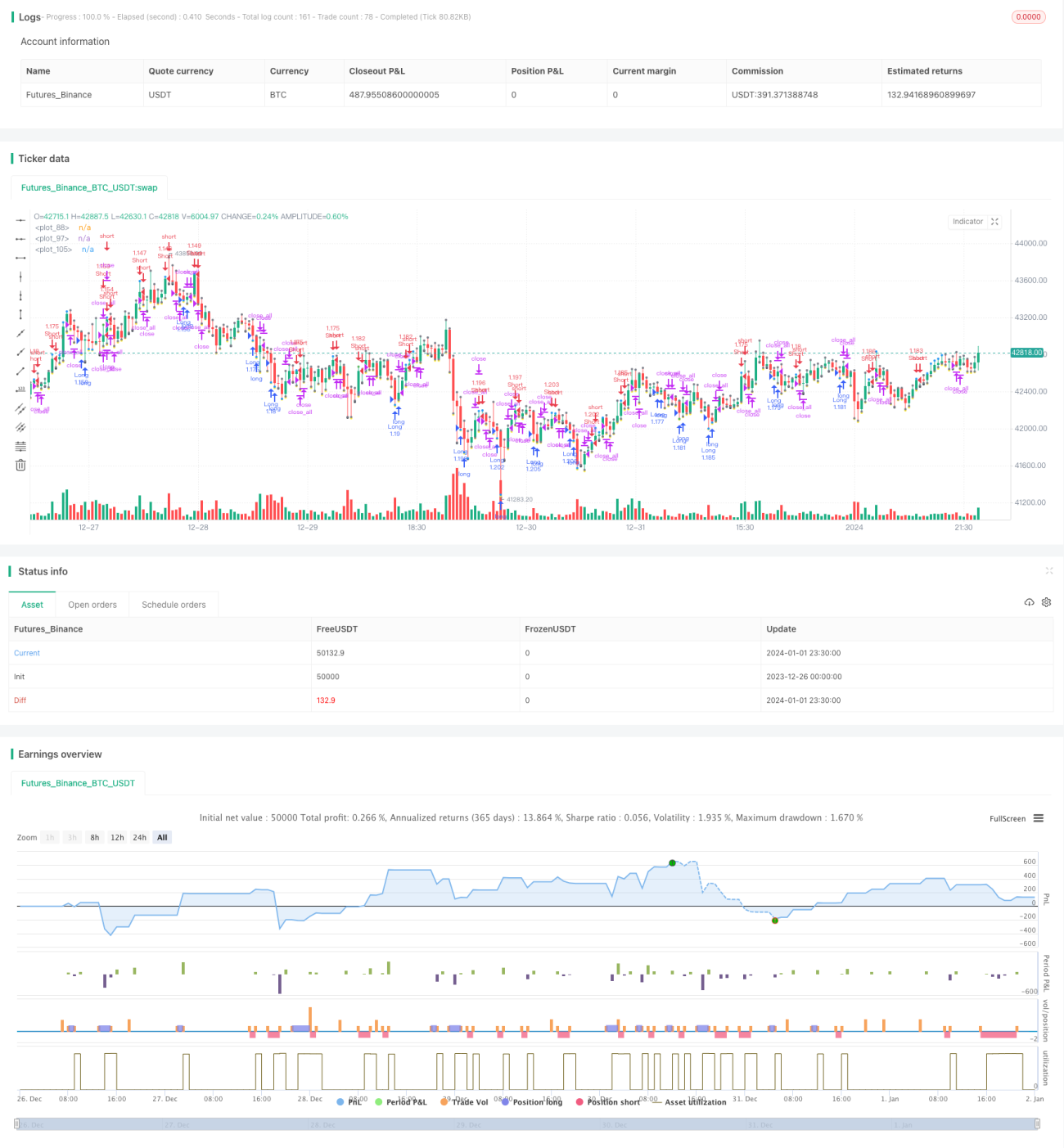

Estrategia de acumulación de rupturas basada en el filtrado de barras significativas

Resumen

Esta estrategia predice la tendencia mediante el análisis de las "velas significativas" de las velas K, y combina señales de ruptura para generar órdenes de trading. La estrategia filtra velas demasiado pequeñas y solo analiza las "velas significativas", lo que evita ser interferido por fluctuaciones pequeñas y frecuentes, haciendo que las señales sean más estables y fiables.

Principio de la estrategia

-

Se determina la longitud del cuerpo real (body) de la vela K actual. Si es 3 veces mayor que el promedio del cuerpo de las últimas 6 velas K, se considera una "vela significativa".

-

Si 3 "velas significativas" consecutivas son todas alcistas, se identifica una señal alcista; si son todas bajistas, se identifica una señal bajista.

-

Al mismo tiempo que se evalúa la señal, si el precio supera el máximo o mínimo anterior, se genera una señal de trading adicional.

-

Se utiliza una media móvil simple (SMA) como filtro, y solo se abre una posición cuando el precio atraviesa la SMA.

-

Una vez en posición, si el precio vuelve a cruzar el punto de entrada o la SMA, se cierra la posición.

Análisis de ventajas

-

El uso de "velas significativas" para determinar la tendencia permite filtrar interferencias innecesarias, haciendo que las señales sean más claras.

-

La combinación de señales de tendencia y señales de ruptura mejora la calidad de las señales y reduce las falsas señales.

-

El filtro de la SMA evita comprar en máximos y vender en mínimos. Comprar por debajo del cierre y vender por encima del cierre aumenta la fiabilidad de las señales.

-

El establecimiento de condiciones de stop-loss y take-profit permite cortar pérdidas y asegurar ganancias a tiempo, lo que favorece la preservación del capital.

Análisis de riesgos

-

Esta estrategia es relativamente agresiva al usar 3 velas para determinar señales, lo que podría malinterpretar una oscilación a corto plazo como un cambio de tendencia.

-

Los datos de prueba no son suficientes; los resultados pueden variar según diferentes activos y períodos de tiempo.

-

No se incluye control de posiciones overnight, lo que conlleva riesgo de posiciones abiertas durante la noche.

Direcciones de optimización

-

Los parámetros de las "velas significativas" se pueden optimizar aún más, como la cantidad de velas K consideradas o la definición de "significativo".

-

Se pueden probar diferentes parámetros de período para ver su impacto en los resultados y encontrar el período óptimo.

-

Se puede agregar un stop-loss basado en ATR para controlar el riesgo.

-

Se podría considerar la inclusión de lógica de control de posiciones overnight.

Conclusión

Esta estrategia utiliza el filtro de "velas significativas" y el juicio de tendencia, combinado con rupturas para formar señales de trading, filtrando efectivamente las fluctuaciones pequeñas e innecesarias, resultando en señales más claras y fiables. Sin embargo, debido al corto período de juicio, existe cierto riesgo de errores de predicción. Se puede mejorar mediante la optimización de parámetros y medidas de control de riesgos.

- 1