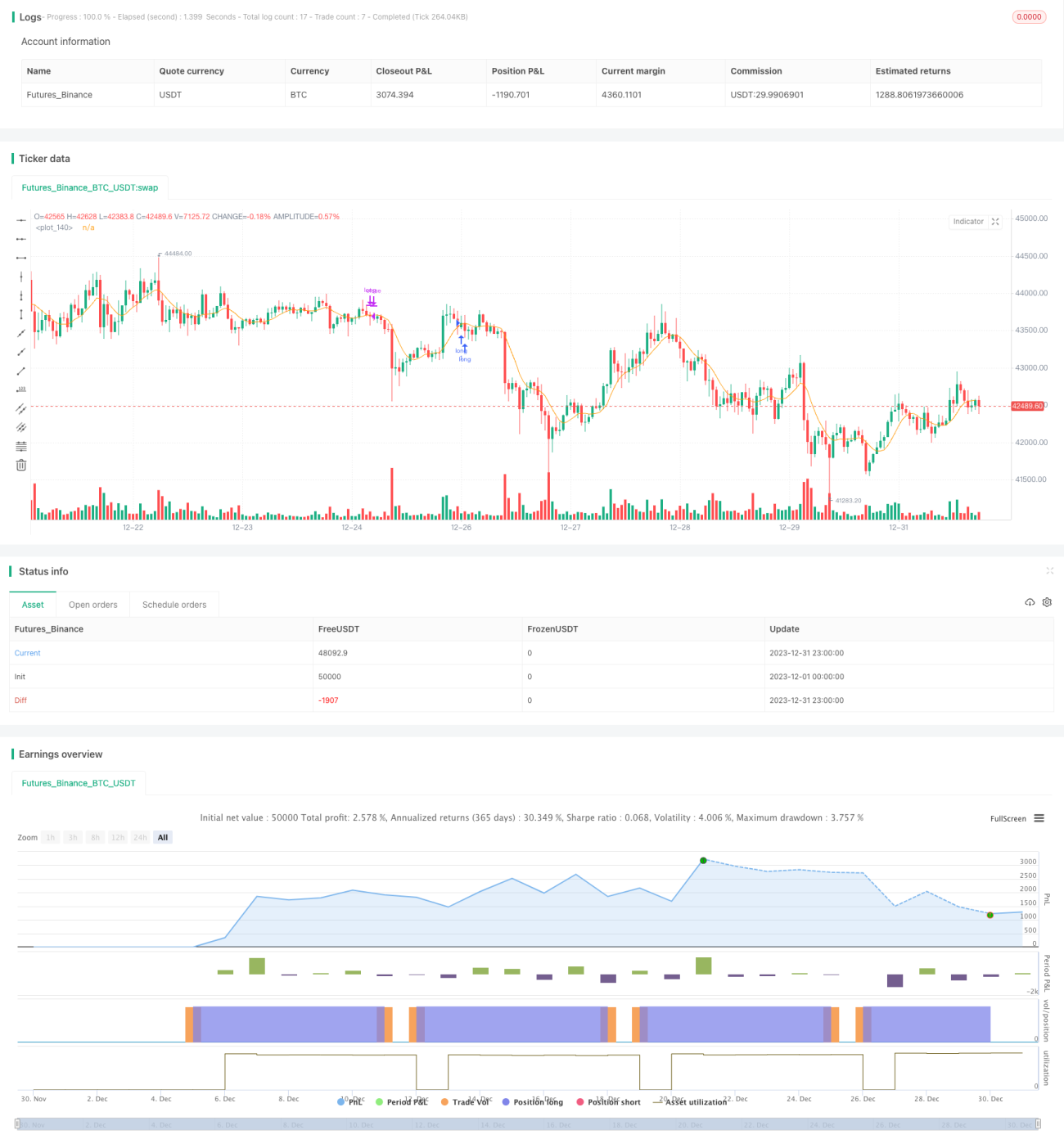

Estrategia de trading cuantitativo que combina medias móviles de múltiples marcos temporales con el horario de negociación

Resumen

Esta estrategia utiliza múltiples indicadores de medias móviles, combinados con la selección de tiempos de negociación para determinar los momentos de entrada y salida, logrando así un trading cuantitativo.

Principio de la Estrategia

La estrategia emplea 9 tipos de medias móviles, incluyendo SMA, EMA, WMA, entre otras. Según la selección del usuario, al abrir una posición larga, el precio de cierre cruza por encima de la media móvil seleccionada y el cierre de la vela anterior se encuentra por debajo de dicha media; al abrir una posición corta, el precio de cierre cruza por debajo de la media móvil seleccionada y el cierre de la vela anterior se encuentra por encima de dicha media. Todas las operaciones se ejecutan únicamente al inicio del lunes. Las condiciones de cierre son un take profit y stop loss fijos, o el cierre antes del cierre del domingo.

Análisis de Ventajas

Esta estrategia reúne la esencia de múltiples medias móviles, permitiendo al usuario seleccionar diferentes parámetros para adaptarse a diversas condiciones del mercado. Solo se ingresa cuando se confirma una tendencia, evitando así las 'operaciones ineficaces'. Además, la estrategia solo abre posiciones los lunes y cierra con take profit/stop loss o antes del domingo, limitando el número máximo de operaciones semanales y controlando eficazmente el riesgo de las transacciones.

Análisis de Riesgos

La estrategia depende principalmente de los indicadores de medias móviles para determinar la tendencia. Cuando la tendencia cambia, existe el riesgo de que algunas operaciones queden atrapadas. Además, al limitar la apertura solo los lunes, si surgen buenas oportunidades después de ese día, no se podrá entrar, lo que podría implicar perder parte de las ganancias.

Para controlar estos riesgos, se recomienda utilizar parámetros dinámicos de medias móviles; cuando el mercado entre en una fase de consolidación, acortar adecuadamente los parámetros. Asimismo, se puede ampliar el horario de apertura, permitiendo abrir nuevas posiciones los miércoles o jueves.

Direcciones de Optimización

Esta estrategia puede optimizarse en los siguientes aspectos:

-

Incorporar un algoritmo de take profit y stop loss dinámico para ajustar los puntos de take profit y stop loss de forma adaptativa.

-

Añadir un modelo de aprendizaje automático para determinar la tendencia anual, evitando entrar en mercados laterales.

-

Optimizar la lógica de apertura y cierre de posiciones, permitiendo más oportunidades de entrada.

Conclusión

Esta estrategia integra múltiples indicadores de medias móviles para identificar la dirección de la tendencia, y mediante el método de abrir posiciones los lunes y cerrarlas los domingos, controla eficazmente el número máximo de operaciones semanales. Al mismo tiempo, las estrictas reglas de take profit y stop loss limitan la pérdida máxima de cada operación. En conjunto, la estrategia está diseñada con optimización en dos dimensiones: juicio de tendencia y control de riesgos, constituyendo una estrategia de trading cuantitativo relativamente robusta.

- 1