Estrategia de cruce de medias móviles ponderadas por momentum

Resumen

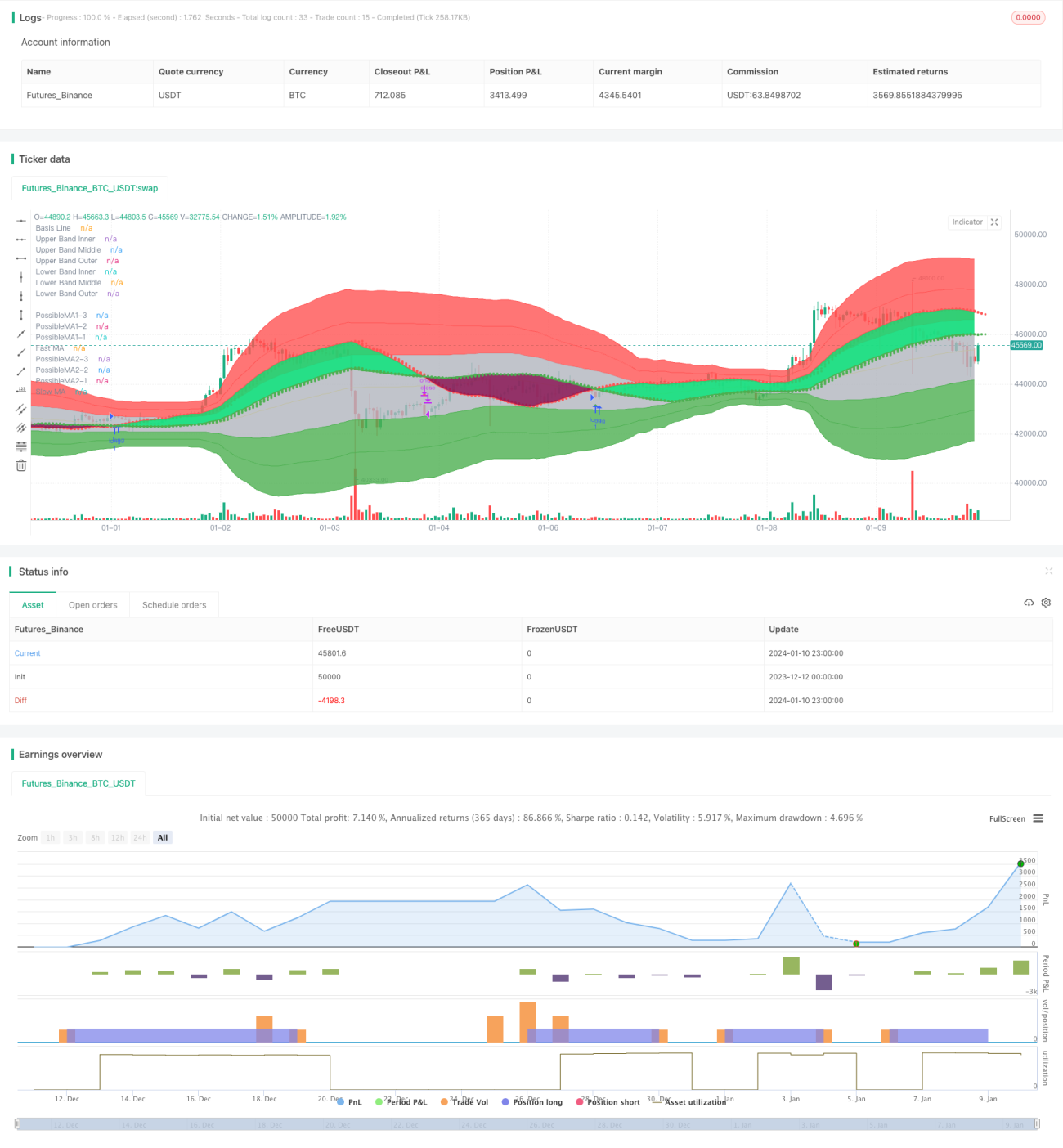

Esta estrategia genera señales de compra y venta cuando se cruzan dos medias móviles exponenciales con peso de momento (MAEMA) de diferentes períodos. La línea de período corto se utiliza para juzgar la tendencia del mercado y las señales de reversión a corto plazo, mientras que la línea de período largo determina la dirección de la tendencia principal.

Principio

- Calcular la MAEMA de la línea rápida (80 períodos) y la línea lenta (144 períodos).

- La línea rápida refleja la tendencia a corto plazo y los puntos de reversión. La línea lenta refleja la dirección principal de la tendencia.

- Cuando la línea rápida cruza por encima de la línea lenta, se genera una señal de compra. Cuando la línea rápida cruza por debajo de la línea lenta, se genera una señal de venta.

- La estrategia también dibuja 3 puntos de predicción, que representan los valores posibles del próximo período, para determinar la tendencia de cruce futura.

- La estrategia aprovecha al máximo la naturaleza de momento y la función de predicción del indicador MAEMA.

Análisis de ventajas

- La MAEMA incorpora un factor de momento por sí misma, lo que permite capturar los cambios de tendencia más rápidamente.

- Estrategia de doble media móvil para juzgar la dirección de la tendencia en diferentes marcos temporales.

- La combinación del cruce de las líneas rápida y lenta con los puntos de predicción de la MAEMA hace que las señales de compra y venta sean más fiables.

- El gráfico automático es completo y refleja intuitivamente la volatilidad del mercado.

Análisis de riesgos

- Cuando el mercado presenta una volatilidad anormal, la sensibilidad del indicador MAEMA puede ser demasiado alta, generando señales falsas. Se puede ajustar adecuadamente el punto de stop loss.

- El sistema de medias móviles tiende a generar señales falsas en mercados laterales. Se pueden agregar otros filtros.

- La configuración de los períodos de la línea rápida y la línea lenta necesita determinar los mejores parámetros según los diferentes instrumentos.

Direcciones de optimización

- Optimizar los parámetros de período de la MAEMA rápida y lenta para encontrar la mejor combinación de parámetros.

- Agregar condiciones de filtro para evitar abrir posiciones en mercados oscilantes. Por ejemplo, introducir DMI, MACD, etc., para juzgar la tendencia.

- Ajustar continuamente el coeficiente ATR y el stop loss móvil en función de los resultados del backtest para reducir los falsos positivos y controlar el riesgo.

Resumen

Esta estrategia utiliza el cruce de dos medias móviles con peso de momento para juzgar los cambios de tendencia del mercado, con un principio básico claro y simple. Combinando el momento y la función de predicción de la MAEMA, es efectiva para identificar señales de reversión. Es necesario prestar atención a la optimización de parámetros y fortalecer las condiciones de filtro para mejorar la estabilidad.

- 1