Estrategia de combinación de doble media móvil y punto pivote

Resumen

Esta estrategia combina la estrategia de reversión de patrón 123 con la estrategia de puntos pivote para obtener una mayor tasa de aciertos. La estrategia de reversión de patrón 123 identifica puntos de reversión de tendencia, mientras que la estrategia de puntos pivote determina los niveles clave de soporte y resistencia. La combinación de ambas permite capturar la tendencia y determinar precios específicos de entrada y salida.

Principio de la estrategia

Estrategia de reversión de patrón 123

Esta estrategia se basa en el estocástico para identificar puntos de reversión de tendencia. El principio específico es:

Cuando el precio de cierre es inferior al cierre anterior durante 2 días consecutivos y el estocástico lento de 9 días está por debajo de 50, se abre una posición larga; cuando el precio de cierre es superior al cierre anterior durante 2 días consecutivos y el estocástico rápido de 9 días está por encima de 50, se abre una posición corta.

Estrategia de puntos pivote

Esta estrategia calcula tres líneas de soporte y tres líneas de resistencia basándose en el máximo, el mínimo y el cierre del día anterior. El método de cálculo es:

Punto pivote = (Máximo + Mínimo + Cierre) / 3

Soporte 1 = 2 * Punto pivote - Máximo

Resistencia 1 = 2 * Punto pivote - Mínimo

Soporte 2 = Punto pivote - (Resistencia 1 - Soporte 1)

Resistencia 2 = Punto pivote + (Resistencia 1 - Soporte 1)

Soporte 3 = Mínimo - 2 * (Máximo - Punto pivote)

Resistencia 3 = Máximo + 2 * (Punto pivote - Mínimo)

Y se determina la entrada y salida basándose en los niveles de soporte y resistencia.

Ventajas de la estrategia

- Combina las ventajas de dos tipos diferentes de estrategias: puede identificar reversiones de tendencia y fijar niveles de precio específicos, logrando una mayor tasa de aciertos.

- La estrategia de patrón 123 puede identificar eficazmente puntos de reversión de tendencia a corto plazo.

- La estrategia de puntos pivote puede utilizar niveles clave de soporte y resistencia para filtrar falsas rupturas.

Riesgos y cobertura

- El indicador estocástico dual tiene cierto rezago, lo que podría perder reversiones a corto plazo.

- Los puntos pivote no son 100% efectivos; puede ocurrir que el precio rompa y continúe moviéndose.

- Se pueden ajustar adecuadamente los parámetros o combinar con otros indicadores para cubrir el riesgo.

Direcciones de optimización de la estrategia

- Se puede probar el impacto de diferentes parámetros en el rendimiento de la estrategia.

- Se puede intentar combinar con otros indicadores o patrones para mejorar el rendimiento de la estrategia.

- Se pueden incorporar algoritmos de aprendizaje automático para optimizar dinámicamente los parámetros.

Resumen

Esta estrategia combina hábilmente la identificación de tendencias con niveles de precio clave, lo que permite tanto detectar puntos de reversión de tendencia como filtrar señales mediante soportes y resistencias. Mediante la optimización de parámetros y la combinación de estrategias, se puede mejorar aún más su rendimiento. Esta estrategia merece ser estudiada y aplicada por los traders cuantitativos.

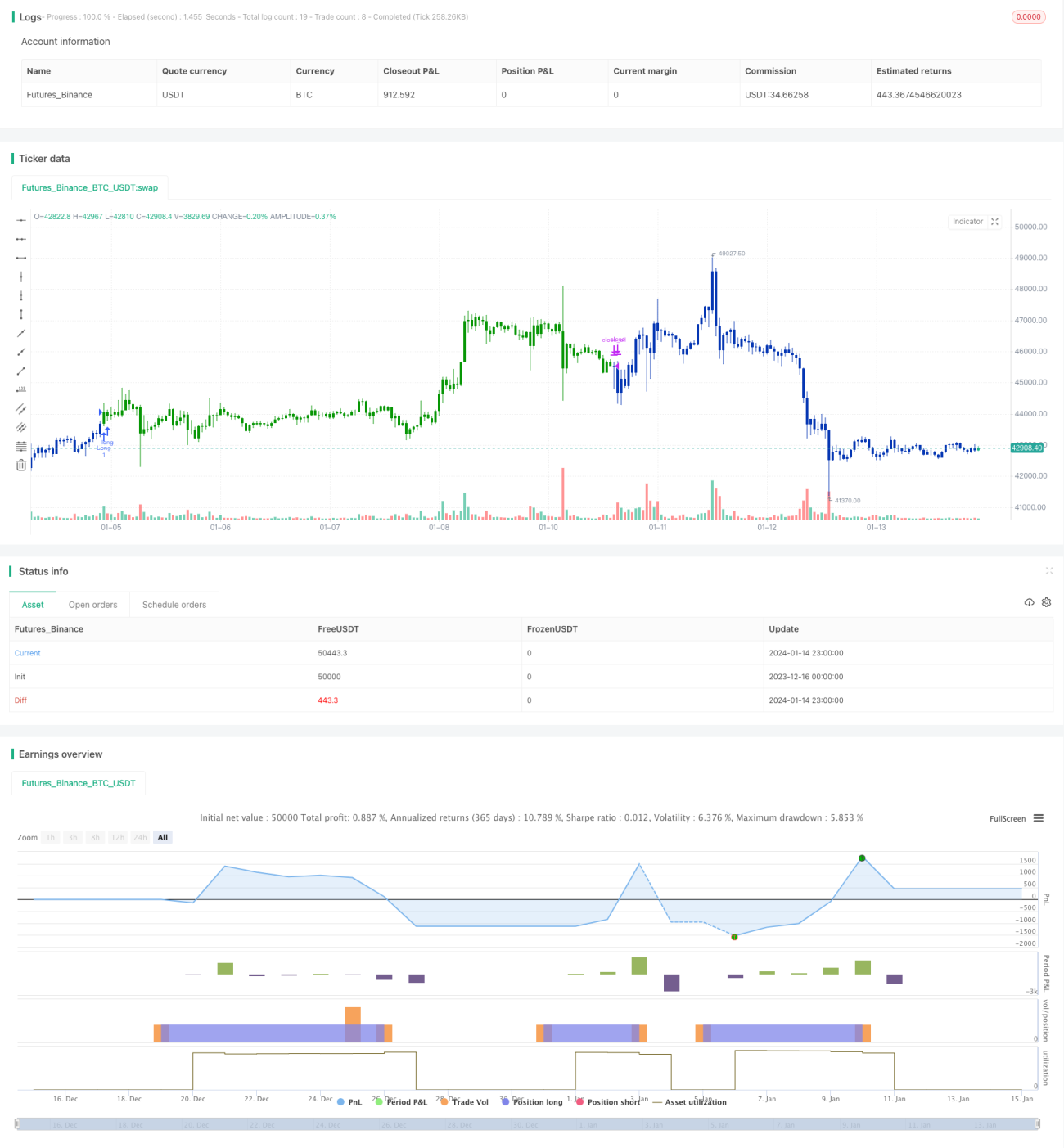

/*backtest

start: 2023-12-16 00:00:00

end: 2024-01-15 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

////////////////////////////////////////////////////////////

// Copyright by HPotter v1.0 21/04/2021

// This is combo strategies for get a cumulative signal. - 1