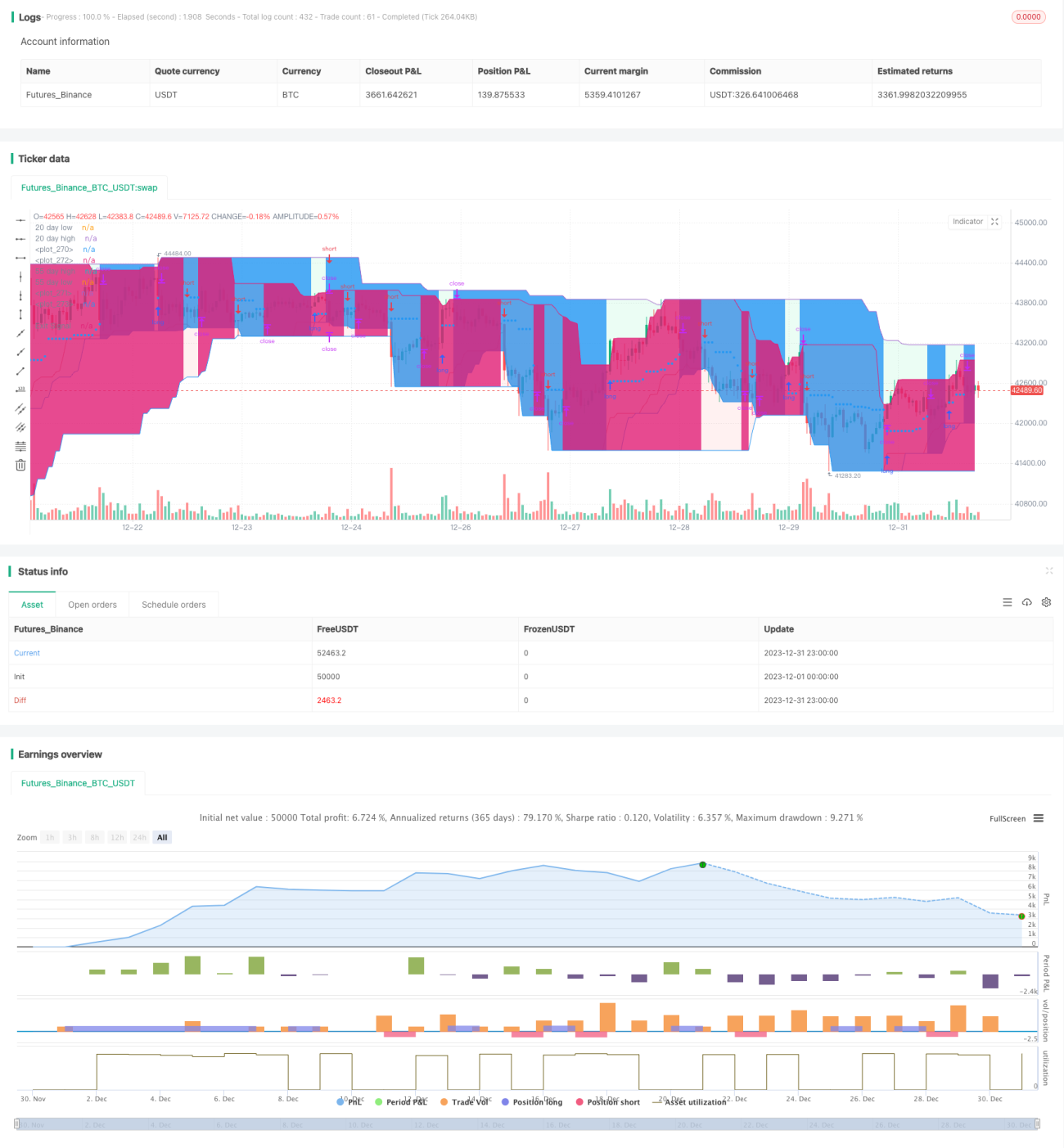

Modelo de reversión de ruptura basado en la estrategia del Comerciante Tortuga

Resumen

Esta estrategia se basa en la famosa "Estrategia del Operador de Tortugas", que ha sido validada durante muchos años. Envía señales de posiciones largas y cortas, permitiendo hasta 5 órdenes piramidales, lo que significa que la estrategia puede activar hasta 5 órdenes en la misma dirección. Cuenta con una buena gestión de riesgo y capital.

Es importante señalar que la estrategia combina dos sistemas que trabajan juntos (S1 y S2).

Principio de la Estrategia

El tamaño de la posición es muy importante para el Operador de Tortugas a fin de gestionar adecuadamente el riesgo. Este ajuste de posición se adapta a la volatilidad del mercado y a la cuenta (ganancias y pérdidas). Se basa en el ATR (Average True Range, rango verdadero promedio), también conocido como "N". Su longitud por defecto es 20.

El número de unidades a comprar es:

unit = (percentage_to_risk/100)*account/atr*syminfo.pointvalue

Según su tolerancia al riesgo, puede aumentar el porcentaje de la cuenta, pero el Operador de Tortugas usa por defecto el 1%. Si opera contratos, las unidades deben redondearse hacia abajo de forma predeterminada.

Existe una regla adicional para reducir el riesgo cuando el valor de la cuenta cae por debajo del capital inicial: en ese caso, en la fórmula de la unidad se debe reemplazar por:

account := (strategy.equity-strategy.openprofit)*(strategy.equity-strategy.openprofit)/strategy.initial_capital

Hay dos sistemas trabajando juntos:

Una ruptura es un nuevo máximo o nuevo mínimo. Si es un nuevo máximo, abrimos una posición larga; por el contrario, si es un nuevo mínimo, entramos en una posición corta.

Agregamos una regla adicional:

Esta regla adicional permite al operador participar en la tendencia principal si se omite la señal del sistema 1. Si se omite la señal de S1 y la siguiente vela también es una nueva ruptura de 20 días, S1 no emitirá señal. Debemos esperar la señal de S2 o esperar una vela que no produzca una nueva ruptura para reactivar S1.

Análisis de Ventajas

La estrategia de Tortugas nos permite agregar unidades adicionales a la posición cuando el precio se mueve a nuestro favor. He configurado la estrategia para permitir agregar hasta 5 órdenes en la misma dirección. Por lo tanto, si el precio cambia desde la compra, agregamos unidades.

Configuramos la primera orden (larga o corta) como la orden máxima. Las órdenes piramidales subsiguientes tendrán menos unidades que la primera orden.

Establecemos un stop loss máximo del 10% para la primera orden, lo que significa que no perderá más del 10% del valor de la primera orden. Sin embargo, dado que el stop loss aumenta/disminuye en 0.5 * ATR(20), sus órdenes piramidales podrían perder más, en cuyo caso no se garantiza que la pérdida sea inferior al 10%. El riesgo sigue estando bien gestionado, ya que el valor de estas órdenes es menor que el de la primera orden.

Análisis de Riesgos

El mayor riesgo de esta estrategia es mantener posiciones demasiado grandes. Debido a que las órdenes se colocan como órdenes de mercado, si se colocan múltiples órdenes de mercado de gran tamaño al mismo tiempo, se producirá un gran impacto en la cotización, lo que generará un deslizamiento significativo. Esto puede provocar pérdidas de capital considerables.

Otro riesgo es una configuración inadecuada de la gestión de capital. Por ejemplo, si el stop loss está mal configurado o el porcentaje es demasiado grande, puede generar grandes pérdidas. Es necesario configurarlo cuidadosamente según su propia tolerancia al riesgo.

Direcciones de Optimización

La estrategia se puede optimizar en los siguientes aspectos:

-

Se pueden probar diferentes parámetros para ver su impacto en la tasa de rendimiento y el índice de Sharpe, como el período ATR, el múltiplo ATR para el stop loss, etc. Encontrar la combinación óptima de parámetros.

-

Se pueden probar diferentes reglas de entrada y salida. Por ejemplo, usar patrones de velas como filtros adicionales.

-

Se pueden probar otros tipos de stop loss, como stop loss móvil o stop loss dinámico. Esto podría reducir la probabilidad de que se active el stop loss.

-

Se pueden probar diferentes cantidades de órdenes piramidales. Cuantas más órdenes, mayor apalancamiento y riesgo. Encontrar el punto de equilibrio óptimo.

-

Se puede intentar detener las operaciones durante períodos específicos (por ejemplo, antes de la publicación de datos de nóminas no agrícolas de EE. UU.) para evitar el impacto de eventos importantes.

Conclusión

En general, esta estrategia ofrece un buen equilibrio entre riesgo y rendimiento, adecuada para el trading de tendencia a mediano y largo plazo. Tiene ventajas como un trading sistemático y un riesgo controlable. Mediante la optimización, se puede mejorar aún más la estabilidad y la tasa de rendimiento de la estrategia.

- 1